In eight trading days, the first quarter of 2015 will come to a close. After a respectable fourth quarter rally last year, the market has struggled over the past three months. At yesterday’s close DJIA was up 1.4% year-to-date, S&P 500 was up a modest 2.0% and NASDAQ had a 5.2% gain. Whether or not the current 6-year old bull market is forming a top is still open for debate. However, what is not open for discussion is the fact that the “Best Six Months” of the year could come to an end as early as April 1.

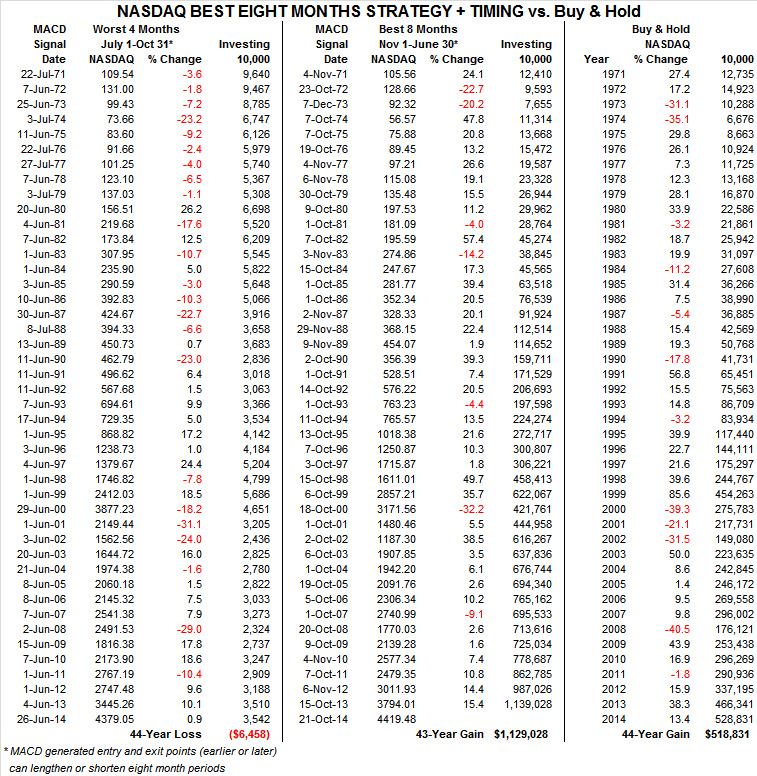

The long-term track record of our Seasonal Switching Strategy, which is based upon the “Best Six Months”, has a solid track record of outperformance with potentially less risk compared to a buy and hold approach. Since 1950, DJIA’s average annual gain has been 8.4%. Over the same time period, DJIA has lost an average 1.1% during the “Worst Six Months,” May through October, and gained an average 9.3% during the “Best Six Months,” November through April.

Detractors are quick to point out that there have been positive “bad” months and negative “good” months. This is absolutely true as there is no trading or investment strategy that works 100% of the time (even the best will report a trading loss every once and a while). Even in pre-election years, the best performing year of the four-year cycle, there have been some rather nasty selloffs. Most recently in 2011 when DJIA fell 9.4%, S&P 500 dropped 11.4% and NASDAQ declined 10.4% during the worst months.

Our Seasonal Switching Strategy may not suit every investor or trader, but before dismissing it consider this. Would you book a Gulf Coast or Caribbean vacation during hurricane season? Sure, you might find a great bargain and have a great trip, but it could just as easily turn out to be a real disaster.

Applying Our Seasonal Switching Strategy

Use of the words buy and sell has created some confusion when used in conjunction with our Seasonal Switching Strategy. They are often interpreted literally, but this is not necessarily the situation. Exactly what action an individual investor or trader takes when we issue our official fall buy or spring sell signal depends upon that individual’s goals and, most importantly, risk tolerance.

A conservative way to execute our switching strategy, the in-or-out approach as we like to refer to it entails simply switching capital between stocks and cash or bonds. During the “Best Months” an investor or trader is fully invested in stocks. Index tracking ETFs and mutual funds are an easy and inexpensive way to gain stock exposure. During the “Worst Months” capital would be taken out of stocks and could be left in cash or used to purchase a bond ETF or bond mutual fund.

This approach works very well for retirement accounts where the goal is to build wealth over time. It comes with the added advantage of potentially less risk of a “buy and hold”. Of further benefit, you may find summertime vacations and activities more enjoyable because you will not be concerned with stock market gyrations while your nest egg is parked in the relative safety of cash or bonds.

The approach that we use in the Almanac Investor Stock and ETF Portfolios involves making adjustments to your portfolio in a more calculated manner. During the “Best Months” additional risk can be taken as solid market gains are most likely, but during the “Worst Months” risk needs to be reduced, but not necessarily entirely eliminated. There have been several strong “Worst Months” periods such as 2003 and 2009. Taking this approach is similar to the in-or-out approach however; instead of exiting all long stock positions a defensive posture is taken.

Weak or under-performing positions can be closed out, stop losses can be tightened, new buying can be limited, and a hedging plan can be implemented. Purchasing out-of-the-money index puts, adding bond market exposure, and/or taking a position in a bear market fund would mitigate portfolio losses in the event a summer pullback manifests into something more severe such as a full blown bear market.

Worst Months Defense

We are not issuing the signal, we are only prepping for when it arrives.

Currently, the Almanac Investor Stock Portfolio and ETF Portfolio are positioned for the “Best Months” with no exposure to bonds, distant or nonexistent stop losses and a long-only bias. But, beginning April 1, 2015 we will begin looking for our seasonal MACD sell signal accompanied by signs of seasonal weakness. Our recent Official Seasonal MACD Sell Signal Alerts proved rather timely as the market topped shortly thereafter. Even last year, DJIA gained just 2.3% between our April Seasonal Sell and our October Seasonal Buy.

When both the DJIA and S&P 500 MACD Sell indicators trigger a sell signal, we will issue an Almanac Investor Alert. We will either outright sell specific positions or implement tight trailing stop losses. Bearish/defensive positions in: iShares Barclays 7-10 Year Treasury (IEF), iShares Barclays 20+ Year Treasury (TLT), Ranger Equity Bear (HDGE) and other protective strategies will also be considered. All stock and ETF holdings will be evaluated at that time. ETFs providing exposure to sector seasonalities ending in April and May along with under-performing stocks in the Almanac Investor Stock Portfolio may be sold at that time as well.

For traders and investors employing the “Best 6 + 4-Year Cycle” as detailed on page 62 of the Stock Trader’s Almanac 2015, this year’s upcoming Seasonal MACD Sell signal could be overlooked. Again, individual risk appetite will determine which of the above paths are preferred.