|

2020 Forecast: Santa Brings New Highs, Market Sanguine on Impeachment & Sitting President Running

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 19, 2019

|

|

|

|

The House of Representatives impeached President Trump last night. The stock market woke up today, yawned and rallied smartly to new all-time highs across the board. Senate republican leadership has made it clear they are not on a trajectory to remove the president from office. The market remains sanguine as the likelihood of the president’s removal from office appears low. So we have sitting president running for reelection with mountains of cash, and an apparently reunified Republican Party rallying around the president.

Late today the House passed Trump’s USMCA trade agreement between the USA, Mexico and Canada. Across the pond Boris Johnson recently won the latest general election handily, so the UK finally appears headed toward the long awaited smooth and soft Brexit by January 31. Trade is improving with the Phase 1 trade deal with China nearing completion as both China the US have been announcing concessions and details.

The Fed is on hold, but ready to act and already has QE lite underway as it keeps the treasury repo markets flush with liquidity. Weak earnings and high valuations represent the best reason for a mild pullback, mid-January perhaps or just ahead of next earnings season. Risks remain, mostly on the trade and earnings/valuation fronts, but uncertainty appears to be trending lower. Growth is soft, but not zero or negative. Trade deals are moving forward and we have an easy Fed ready to act. Declining uncertainty supports a bullish outlook for 2020.

Four Horseman of the Economy

DJIA along with S&P 500 and NASDAQ have been leading the pack all year long. We have just logged new highs in prototypical Pre-Election Year fashion. Save any major setbacks on the trade, earnings, election or geopolitical fronts gains are likely to trend higher, except for a mild correction.

Consumer confidence remains positive though it has been flattening out over the past five years. Continuing progress on trade deals and Brexit, plus an easy Fed and more stable and functional federal government should help to improve consumer confidence in 2020.

The Unemployment Rate continues to remain super low at 3.5%. Economic activity may have decelerated some, but it remains solid and prices remain stable. Even more jobs are on the near-term horizon as Census 2020 hiring and 2020 election campaign hiring ramps up. We have seen the mailings for how to apply for a census job.

Our inflation horseman as measured by our 6-month exponential moving average calculations on the CPI and PPI have been in retreat, especially the PPI which has gone negative – likely the underlying reason the Fed lowered rates three times this year. CPI is now below the Fed’s target inflation rate of 2% at 1.88%.If negative PPI trickles into CPI we would not be surprised if Fed cut rates again. The Fed is terrified of sub 2% inflation. But with all the government hiring and deficit spending we don’t see a recession likely in 2020.

2019 Forecast Recap

The three-case forecast we presented last year was:

- Worst Case – Prolonged bear market caused by hawkish Fed, dysfunctional Federal Government, slow growth and weak corporate fundamentals brings us all the way back to November 2016 pre-Trump election levels or lower. Repeat of pre-election year 2015 with the bear lasting throughout 2019 into 2020.

- Base Case – Something gives. Mild bear market bottoms soon or in early 2019 as Fed tones down rhetoric and holds off raising rates, Trump and the Dems work out a few deals and we have modest pre-election year gains in the 5-10% range.

- Best Case – Everything resolves quickly. Fed becomes accommodative. Trade deals are worked out expeditiously. Trump tacks towards the center and works with congress and does not get “Muellered.” Typical pre-election year gains of 10-15% for Dow and S&P 500 and 20-30% for NASDAQ

We scrapped our worst case scenario rather quickly in 2019 as our January Indicator Trifecta came in positive 3-for-3. The Santa Claus Rally reemerged on the day after Christmas, logging a 1.3% gain for the S&P 500 during the 7-trading day stretch that includes the last five days of the year and the first two of the New Year, right in line with the historical average. Then our “First Five Days Early Warning System” came in strong with a 2.7% gain for the S&P and finally our full-month January Barometer registered a whopping 7.9%. This flashed a big green light for us as the market posted gains in 27 of the previous 30 years that all three components of our January Indicator Trifecta were up.

As the year progressed, closely tracking the bullish pattern of Pre-Election Years and often trending well above the historic seasonal pattern for Pre-Election Years (as we documented all year long), our base case scenario fell by the wayside. Then the Mueller Report found nothing conclusive on collusion, the Fed became accommodative and the Trade deal negotiations progressed with China. Decent fundamentals, supportive technicals and few attractive investments other than US equities kept us bullish all year in line with our best case scenario (except for our seasonal defense over the “Worst Six Months, which proved to be prudent and beneficial). Currently, at todays close the market is above our best case scenario with DJIA up 21.6% year-to-date, S&P 500 up 27.9% and NASDAQ up 33.9%.

Pulse of the Market

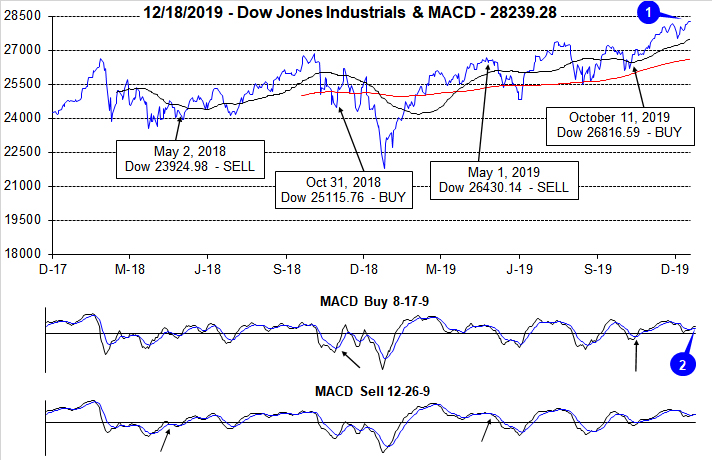

Typical first-half December weakness arrived a bit earlier than usual this year. DJIA suffered back-to-back, greater than 200-point declines on the first and second trading days of December (1). This “dip” proved to be brief as DJIA quickly recovered and is once again trading above 28,000 and at new all-time highs. As a result of DJIA’s quick reversal and new positive momentum, both the faster (2) and slower MACD indicators applied to DJIA are once again positive.

After four straight weeks of gains, DJIA has declined modestly in two of the last four weeks ending December 13. In the middle of this mixed streak of performance DJIA logged its seventh Down Friday/Down Monday (DF/DM) of the year (3). Since 1995, DJIA has recorded an average of 10 DF/DMs per year. This year’s below average number of DF/DMs is yet another confirming sign of underlying market strength. However, given the historical record of DF/DMs, it would be prudent not to forget that most past occurrences were followed by some weakness during the next 90 calendar days. Early December weakness may have been sufficient as the most recent DF/DM was most likely the result of trade and progress has since been made in the form of a Phase 1 deal with China.

S&P 500 has advanced in nine of the last 10 weeks (4) and NASDAQ has risen in nine of its last eleven (5). The worst weekly decline by S&P 500 or NASDAQ was a meager 0.3% during the week before Thanksgiving. Solid performance across all three indexes would seem to suggest more new all-time highs are likely in the near-term.

Market breadth measured by NYSE Weekly Advancers and NYSE Weekly Decliners (6) has begun to improve over the past two weeks with Weekly Advancers outnumbering Weekly Decliners by larger amounts when compared to mid-November. Rotation from defensive sectors to growth is likely slowing and participation in the rally could be broadening.

Weekly New Highs and Lows (7) remained somewhat mixed considering the new all-times highs reached by the major indexes. Overall New Highs remain subdued, but they are trending higher while New Lows continue to bounce around leaving room for further improvement. Should small-caps pick up and join in the rally, weekly metrics will likely respond with improvement.

The 90-day Treasury rate and the 30-year Treasury rate (8) appear to be stabilizing around current levels. The Fed has signaled it is most likely done with rate cuts unless there is a material change to their outlook or the data. Historically, U.S. rates are low and other developed nation’s rates are even lower. Low rates have historically been a positive for stocks.

Click for larger graphic…

2020 Forecast

- Worst Case – Correction, but no bear in 2020. Flat to single digit loss for full year due to on-going unresolved trade deals, no improvement in earnings and growth weakens further. Trump is removed from office by the Senate, resigns or does not run and political uncertainty spikes.

- Base Case – Average election year gains. Incumbent victory, trade and growth remain muddled, modest improvement in corporate earnings and Fed stays neutral to accommodative. 5-10% gains for DJIA, S&P 500 and NASDAQ.

- Best Case – Above average gains. Incumbent victory, trade resolved, growth improves, earnings improve and Fed stays neutral and accommodative. 7-12% for DJIA, 12-17% for S&P 500 and 17-25% for NASDAQ.

We will be keeping you fully abreast of all readings from our three January Trifecta Indicators: Santa Claus Rally, First Five Days and the full-month January Barometer and will make adjustments on the close of January 2020.

Happy Holidays & Happy New Year, we wish you all a healthy and prosperous 2020!