Today’s rally caps the biggest three-day surge since October 6-8, 1931. That may sound encouraging, but remember 1931 was the worst year for DJIA on record, down 52.7%. DJIA is up 21.3% since Monday’s low. This surge comes on the heels of the fastest and most furious decline in stock market history. DJIA dropped 37.1% from its 2/12/2020 all-time high in 40 calendar days. It fell 35.9% in 31 days from the top of the

waterfall decline on 2/21/2020 and 31.4% in 19 days from the 6.6% three-day rally March 2-4, 2020.

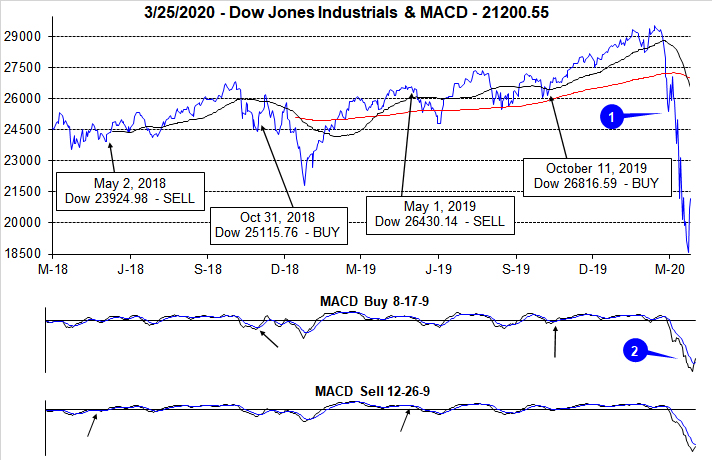

While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

Federal Reserve and Federal Government action has been more encouraging. The Fed has made it clear that it will supply unlimited liquidity to the financial system. Congress is fast tracking this $2 trillion emergency stimulus package, which the President has vowed to sign – and more is likely. There are also some encouraging therapeutic solutions, but nothing of substance yet. And the lockdown of much of the country has yet to stem the spread of COVID-19 in the U.S.

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the

March Outlook we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the

January Barometer as measured by the S&P 500 were down and the Dow closed below its previous December closing low in the first quarter. Below that is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.

![[Dec Low Down Jan Seasonal Chart]](/UploadedImage/AIN_0420_20200326_2020_v_Down_JB_Dec_Low.jpg)

The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage, “If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.”— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)

The table below of Down Best Six Month for DJIA since 1950 also suggests caution and patience is in order. Subsequent Worst Six Months (May-October) have averaged losses with only two decent years 1982 and 2009. The market bottom in August 1982 marked the end of the 1966-1982 secular bear market and came of the early 1980s double dip recession. Following the first back-to-back down Best Six Months since 1973-1974, the market hit a secular bear market low in March 2009. Market action in the rest of these years was rather grim.

![[Down Best Six Months Table]](/UploadedImage/AIN_0420_20200326_Down_BSM.jpg)

Stop losses in our Stock and Sector ETF Portfolios got us out of all but a few positions before the bottom fell out of the market, mitigating our losses significantly. This is a generational crisis that will forever change our lives. But the market has been through these trials and tribulations before – so have the Stock Trader’s Almanac and our brand of seasonal and cyclical trading and investing strategies. Soon enough market conditions will be such that will have new investment and trading ideas for you. Continue to stick to the system, heed stop losses and remain rational.

Pulse of the Market

DJIA’s 37.1% decline (1) from its closing high on February 12 through its closing low thus far on March 23 took just twenty-seven trading sessions. Market crashes in 1929 and 1987 are the closest comparable declines although there are observable similarities to numerous other waterfall declines. The once reliable death cross indicator, when the 50-day moving average falls below the 200-day moving average, would not have provided much relief in the current sell off as the indicator triggered on March 23, at the current low.

DJIA’s abrupt reversal and violent decline has both the faster and slower moving MACD indicators deep in negative territory well below the zero line (2). If the chart of MACD looks different, it is. We had to change the scaling of the MACD charts to account for the sharp decline. Currently, the faster moving MACD turned positive on Wednesday’s close and the slower moving MACD indicator could turn positive today. A reprieve from all the selling of late is welcome however it is still too early to assert that the final lows of this bear market have been reached.

Fridays continue to be challenging with DJIA recording just two positive Fridays out of twelve so far this year (3). For the last six weeks, selling on Friday was better than holding over the weekend five times. Monday now holds the record for worst and third worst daily DJIA losses by points. With five Down Friday/Down Mondays (DF/DMs) in less than three months, 2020 is on a pace to have the most of any year going back to 1995 (page 76 of Stock Trader’s Almanac 2020).

Last week, DJIA, S&P 500 (4) and NASDAQ (5) all recorded their biggest weekly percentage declines since October 2008. Four weeks prior, the last week of February also suffered double-digit declines. Currently, the market is on course to recover some of last week’s losses, but any gains this week may not last as uncertainty remains high.

Market breadth measured by NYSE Weekly Advancers and NYSE Weekly Decliners (6) has reached extremes of historic proportions twice in the last three weeks. At the end of February, Weekly Decliners outnumbered Weekly Advancers by nearly 27-to-1 and last week the ratio was over 35-to-1. The only week to log a more lop-sided number was October 10, 2008 when the ratio spiked to just over 41-to-1. Back in 2008, the market did rebound in the following week, but the bear market bottom was not reached until March 2009.

Weekly New Highs have evaporated while Weekly New Lows have exploded to the highest number (7) since October 10, 2008. Last week’s levels will likely not be reached or exceed again in this bear market and can really only improve from there.

Yet another reading that reached a level last seen in the depths of the financial crisis of 2007-2009, was the Weekly CBOE Put/Call ratio (8) last week at 1.03. In November 2008 it reached 1.04. Back then, the market did bounce and move higher into early January of 2009, but that bounce failed to hold.

Click for larger graphic…