AI and the chip stocks are surely conspiring to drive NASDAQ higher during this last leg of NASDAQ’s Best 8 months November-June. AI also stands for Almanac Investor. It is a testament to our seasonal stock screening process that we uncovered Super Micro Computer, Inc. (SMCI) in last November’s stock basket, which is riding the AI wave.

As of today’s close, SMCI is up 152.5% from our buy price and it’s up 121.8% in the last 30 days. In a recent release president and CEO Charles Liang said, “Supermicro continues to lead the industry supporting the demanding needs of AI workloads and modern data centers worldwide.” Their liquid-cooled AI-optimized racks use both Intel and AMD CPUs with NVIDIA GPUs.

Our portfolios are enjoying this AI/Chip-driven rally, but the backdrop over the market remains cautious and still sets up for further sideways action and a likely pullback or correction over the weak summer months, especially after mid-July into the worst two months of the year August and September.

We have created a new NASDAQ’s seasonal pattern chart here that compares the one-year pattern of all NASDAQ years from 1971-2022 with pre-election years along with our STA Aggregate Cycle which is a combination of all years, pre-election years and years ending in three. So far in 2023 NASDAQ is closely tracking the pre-election pattern up 21.3% year-to-date.

All three pattern lines show a distinct mid-July peak and then sideways action through late October before the usual pre-election Q4 strength that often brings annual highs and perhaps even new all-time highs. This is lining up well for our NASDAQ Best 8 Months MACD Seasonal Sell Signal that can occur anytime on or after June 1. Subscribers will of course be emailed when it triggers. This NASDAQ rally is also providing us ample time to reposition our portfolio for the Worst 4 months of the year July-October.

We suspect that by September the folks in Congress will have made a deal with folks in the White House on the debt ceiling and the budget– at least for the time being. They will likely have managed to simultaneously put feathers in the respective caps that they can tout in their next election campaigns that will ramp up in Q4 of this year where the 4-year cycle and the seasonal cycle converge to rally mode.

In the process, however, their machinations will likely keep the market contained in a relatively narrow range. We have added a couple of notes to our 2011 vs. 2023 debt ceiling showdown comparison highlighting both parties’ 2023 negotiation maneuvers are right out of the 2011 playbook. We don’t expect the same degree of market fallout this year since we all saw this movie in 2011.

Unless there really is an impasse and there is no deal. If that were to transpire, our worst-case scenario might come into play. But for now, expect a deal to occur just in time and the market to mark time until September/October before moving significantly higher.

In the meantime, investors and traders are still handicapping the Fed’s next moves which is back to about even money on a hike or pause at the June FOMC meeting. There is also still plenty of recession fear mongering. We don’t see it. The reliable Atlanta Fed’s GDPNow model’s latest estimate for Q2 GDP is 2.9%. Many economists and Fed speakers continue to warn about inflation being persistent. All the inflation metrics we see are trending lower. And we contend we had our recession with the two negative quarters of GDP in 2022 Q1-2.

Another concern for the near term is market internals. As noted in the Pulse below, market breadth has been uninspiring as new highs are not expanding while new lows continue to pop up and remain elevated. In the chart below of the S&P 500 we have overlaid the NYSE Advance/Decline Line. Over the past month as the market has drifted sideways the A/D Line has made lower highs and is trending down. This suggests that stocks in general are running out of steam.

The 3800-4200 range is also highlighted with near term support around 4050 still holding. NASDAQ and big tech may be rallying, but the rest of the market seems tired. As NASDAQ’s Best 8 months comes to a close in June and the current AI/chip craze fades we expect seasonality along with the debt ceiling and economic headwinds to prevail and keep a lid on stocks through summer doldrums.

Pulse of the Market

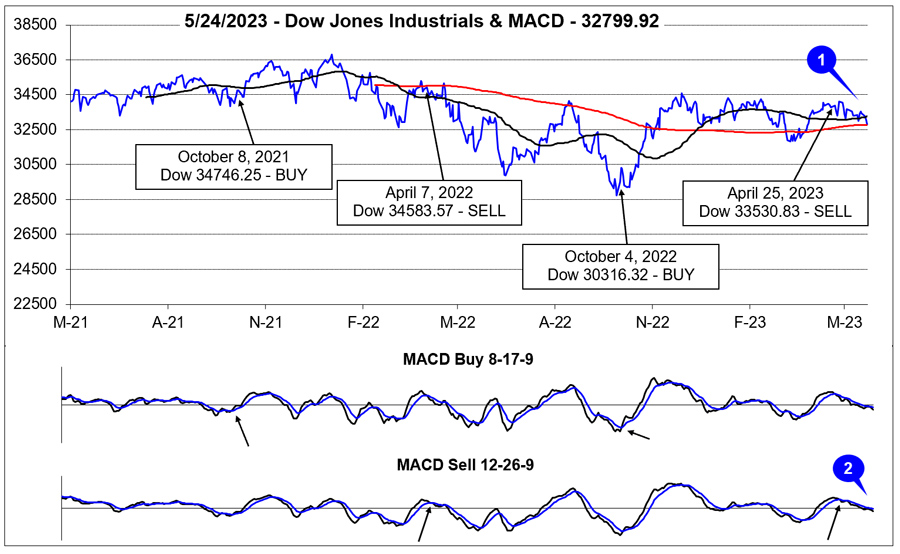

In the four weeks and a day since issuing our Seasonal MACD Sell for DJIA and S&P 500, DJIA declined 2.3% while S&P 500 gained 2.0% as of May 25 close. Over the same period NASDAQ advanced 7.6% as its “Best Months” last through June. Absent heavy technology exposure, DJIA has struggled in 2023 and is down a little more than 1% year-to-date. DJIA has slipped below its 50- and 200-day moving average as of its close today (1). Both the Buy and Sell MACD indicators applied to DJIA remain negative and have been trending lower since crossing over in late-April confirming the loss of positive momentum (2).

It has been more than two months since DJIA recorded its last Down Friday/Down Monday (DF/DM). The last DJIA DF/DM occurred near the end of a multi-week downtrend. The current DJIA DF/DM (3) came with the major indexes near the top of their respective trading ranges. Thus far, NASDAQ strength has averted further weakness that has historically been observed following a DJIA DF/DM. Should NASDAQ falter, a broader and deeper retreat could unfold quickly.

NASDAQ’s dominance (5) in May is clearly on display in the Pulse table with three straight weekly gains compared to just a single weekly advance for DJIA and S&P 500 (4). With NASDAQ breaking out above last August’s highs, strength could persist into June, the last month of NASDAQ’s Best Eight Months.

Market breadth (6) is an area of concern. Weekly Advancers have been meager over the last seven weeks with just a single week exceeding 2000. Weekly Decliners have been stubbornly elevated. This would suggest momentum is fading and the current rally by NASDAQ could soon suffer a similar fate if Weekly Advancers do not begin to increase.

Weekly New Highs and New Lows are also muddled (7). New Highs have been stuck between 100 and 200 for eight straight weeks while New Lows spiked at the start of May and have retreated modestly. Historically, a healthy rally will see the number of New Highs trend steadily higher and New Lows trend lower. The current trend of both suggests the market is likely to continue to trade in a narrow range.

The Fed’s last rate increase and recent hawkish comments have pushed the weekly 90-day Treasury yield (8) to its highest level since January 2001. One major difference between then and now is the yield on the 30-year Treasury. In 2001, the 30-year Treasury yield was over 5.5% versus the 3.89% it is now. Headline CPI then was around 3.7% and, in an uptrend, compared to 5.0% and trending lower now.