|

Market at a Glance - 12/22/2022

|

|

By:

Christopher Mistal

|

December 22, 2022

|

|

|

|

12/22/2022: Dow 33027.49 | S&P 3822.39 | NASDAQ 10476.12 | Russell 2K 1754.09 | NYSE 15081.53 | Value Line Arith 8468.68

Seasonal: Bullish. January is the #1 S&P 500 and NASDAQ month in pre-election years, second best for DJIA. Average pre-election year gains since 1950 range from 3.9% from DJIA and 6.8% by NASDAQ (since 1971). “As January goes, so goes the year.” Our Santa Claus Rally ends on January 4, the First Five Days finish on the nineth and our January Barometer gives its read at month’s end. When all three are positive, our January Indicator Trifecta is nearly perfect with 28 S&P 500 full-year gains in 31 years.

Fundamental: Improving. Final Q3 GDP was revised higher to 3.2%. Q4 GDP estimate from Atlanta Fed’s GDPNow is 2.7%, slightly slower growth but still respectable. Headline CPI has declined from its June peak of 9.0% to 7.1% in November. Unemployment is at 3.7% while weekly initial claims data remains firm. Corporate earnings are still forecast to slow, but not retreat in 2023. Housing is a mess, but the easing of Treasury yields from their earlier highs is translating into lower mortgage rates. Supply chains are also improving with China’s easing of Covid-19 policy.

Technical: Consolidating. Still awaiting confirmation of the new bull market. DJIA did briefly exceed its August closing high and its 50-day moving average has climbed back above its 200-day moving average creating a historically bullish golden cross. However, NASDAQ’s struggles persist, and tech weakness lingers over the entire market. Relative strength, stochastic and MACD indicators applied to DJIA, S&P 500 and NASDAQ are currently at or near oversold levels. Should NASDAQ’s October low hold, another leg higher could be the market’s next move.

Monetary: 4.25 – 4.50%. We could debate endlessly whether the Fed has gone far enough with rates or not, but why bother when they have already explained their plan. At the conclusion of this December’s FOMC meeting, the updated Fed dot plot basically told us that the Fed is going to tighten until they get to 5.00 – 5.25%. This suggests another 0.50% increase on February 1, 2023, and a final 0.25% hike on March 22.

Sentiment: Neutral. According to

Investor’s Intelligence Advisors Sentiment survey Bullish advisors stand at 37.5%. Correction advisors are at 29.2% while Bearish advisors numbered 33.3% as of their December 21 release. Over the last month sentiment is relatively unchanged with only a small increase in the percentage of bearish and correction advisors which is consistent with recent market weakness.

|

2023 Forecast: Choppy Start, Fed Pause Q1, Pre-Election Bull Emerges

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 22, 2022

|

|

|

|

[Publication Note: Today’s Alert will be our last regularly scheduled Alert of 2022. Our next email will be on January 4, 2023. However, if market conditions warrant an interim update, one will be sent. Happy Holidays and Happy New Year!]

Last year at this time we were much more concerned and cautious than most of The Street as we anticipated heightened volatility during the midterm election when we made our

2022 Forecast for an Early Year High, a Worst Six Months Correction and a Q4 Rally.

After our

January Indicator Trifecta came in negative, we shifted more bearish. Even though our Santa Claus Rally delivered positive gains, the First Five Days Early Warning System and our full-month January Barometer were down. This deepened our cautious and bearish posture as we projected lower lows in the Worst Six Months May-October, while maintaining our expectation for a Q4 rally.

Then Russia invaded Ukraine, supply chain bottlenecks continued to mount, inflation heated up and the Fed began an aggressive tightening campaign. Most of the stock and ETF positions in our portfolios were stopped out by the time we issued our timely Best Six Months MACD Sell Signal on April 7. By June our

worst case scenario was in play.

We maintained a large cash position for much of the year and remained on the sidelines through Q3. In mid-August when most traders and pundits were jumping on the bull market bandwagon, we cautioned against the summer-rally hype and warned of another leg down as our

Stock Trader’s Almanac Aggregate Cycle pointed to a

mid-summer top and a retest of the June lows.

Midterm September and October delivered the volatility and selloff they often do, pushing the major averages to new bear market lows – except for the Russell 2000, which constructively held its June lows. Then on October 4th our Best Six Months MACD Seasonal Buy Signal was triggered and the Q4 Rally we had anticipated was underway.

NASDAQ is currently lagging and testing its lows, but as of today’s close the Dow is still up 15.0% for Q4. So now what? Well, unlike last year The Street is full of bears and that has our contrary antenna purring again. We logged a prototypical midterm year bear market here in 2022 and most everyone is calling for the bottom to fallout.

Current conditions remind us quite a bit of 1974 where we had a scattered bottom scenario. S&P and NASDAQ bottomed October 3 and the Dow hit its low on December 6. 2022 is a midterm year like 1974 and there is a steady flow of negative news and dire outlooks.

The chart here of the S&P 500 Seasonal Pattern for Pre-Election Years and our STA Aggregate Cycle first appeared on page 11 of the Stock Trader’s Almanac 2023. It depicts four rather bullish scenarios. All Pre-Election years since 1949 have an average gain of 16.8%. Pre-Election Years after a midterm bear market like 2022 average 20.3% and 1st Term President’s Pre-Election years average 20.1%. Our new Aggregate Cycle of the One-Year Seasonal Pattern, the 4-Year Presidential Election Cycle and the Decennial Cycle averages 12.3%. Despite current worrisome conditions, we believe a midterm bear market bottom is in and a new bull market is emerging. Remember Warrant Buffets wise words: “Be greedy when others are fearful.”

Sweet Spot of the 4-Year Cycle

As we have discussed for much of the year, we are currently sitting in the early stages of the Bullish Sweet Spot of the 4-Year Presidential Election Cycle, which runs from Q4 of the midterm year though Q2 of the pre-election. Over the 3-quarter span Dow averaged 19.3%, S&P 20.0% and NASDAQ 29.3%.

The current 4-year cycle has been more volatile than the average cycle, logging greater than average gains in post-election year 2021 and steeper declines, and a full-blown bear market, in 2022. Perhaps that will equate to outsized “Sweet Spot” gains this time around.

In any event, we are having a hard time swallowing all the doomsday scenarios we are hearing out there. With inflation decelerating, Q3 GDP revised higher to 3.2% from 2.9%, a steady employment picture and the Fed clearly telegraphing it will be done tightening in Q1, we are more inclined to look for a soft landing versus a full-blown catastrophic economic collapse with some positive surprises on the horizon.

Four Horsemen of the Economy

Let’s turn to our Four Horsemen of the Economy for some further perspective. Our lead horseman is the mighty Dow. While the bear market held sway over the market this year the historic blue-chip average was most resilient, losing less than its tech-laden brethren. And now DJIA is leading us higher, up 15.0% from its low. We contend S&P, NASDAQ, Russell 2000, and the broad market will follow suit.

Consumer Confidence collapsed this year as the bear gathered momentum. But it now appears to have bottomed. With inflation receding, GDP rising and retail sales doing just fine, it looks like the worst of consumers’ fears are behind us. Many of these ConCon lows have been associated with recessions in the past as you can see in the chart. We would not be surprised if the negative two quarters of GDP growth we had in Q1 and Q2 of 2022 end up appearing as a mild recession bar on this chart.

Inflation is falling and it may fall faster than most expect. Our 6-month exponential moving averages of the PPI and CPI show a steep drop in PPI. CPI will likely come down at a much slower pace, but it does appear to be rolling over.

Alas our most durable labor market. The unemployment rate will likely tick slightly higher moving forward off its historic low levels. But the labor market is likely forever changed from the pandemic with folks finding an endless array of ways to find gainful employment.

The Santa Claus Rally (created by Yale Hirsch in 1972) is scheduled to start tomorrow. This is our first indicator for the New Year. If the market does not rally over the 7-day period from the last 5 days of the year to the first 2 of the new year it will be cause for concern. To wit Yale’s famous line: “If Santa Claus Should Fail to Call, Bears May Come to Broad and Wall.” (Stock Trader’s Almanac 2023 p 118). But this is only part of our “January Indicator Trifecta.”

The results of the Santa Claus Rally along with the other two components of our “January Indicator Trifecta,” the first five days of January and the full month January Barometer (also created by Yale Hirsch in 1972) will help solidify our outlook for next year.

When all three are up the S&P 500 has been up 90.3% of the time, 28 of 31 years, with an average gain of 17.5%. When any of them are down the year’s results are reduced and when all three are down the S&P was down 3 of 8 years with an average loss of -3.6% with bear markets in 1969 (-11.4%), 2000 (-10.1%) and 2008 (-38.5%), flat years in 1956 (2.6%), 1978 (1.1%) and 2005 (3.0%). Down Trifecta’s were followed by gains in 1982 (14.8%) and 2016 (9.5%).

It has become increasingly apparent to us that the midterm year bear market is over, and we may have already experienced a mild recession. From our vantage point you can cut the bearishness on The Street with a knife. When the market was riding high last year all the big forecasts were for more gains. Now that we have our first double digit annual losses for the S&P since 2008, the big forecasts are for more downside.

Our cycles, indicators and readings of the market are leaning much more bullish. The Fed is almost done. Inflation is falling. China has relaxed its zero Covid-19 policy. With GDP revised higher we see the potential for the elusive soft landing and the usually bullish action associated with pre-election years – especially after the prototypical midterm year bear market we just had.

We will probably experience some early year choppiness. While it sure looks ugly out there, markets love to climb the proverbial “wall of worry.” We contend the worst is behind and a nascent bull is emerging.

Pulse of the Market

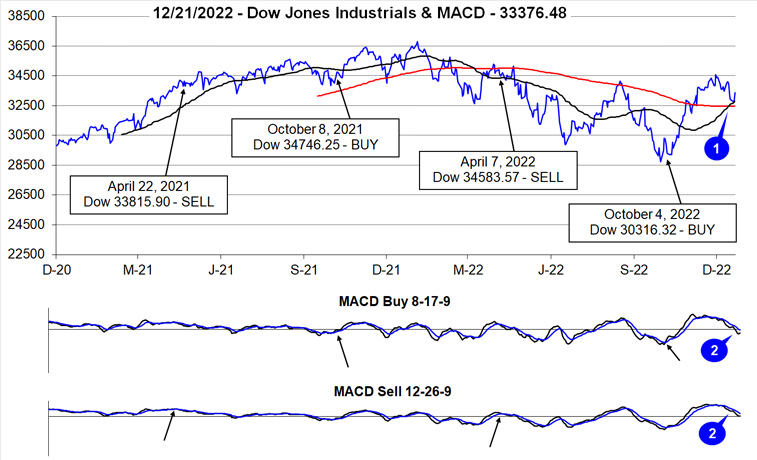

Typical first half of December weakness has persisted beyond mid-month this year. We continue to look for our Santa Claus Rally (SCR) which officially starts when the market opens for trading on December 23. Recent weakness could be setting up the SCR nicely this year. Despite recent weakness, DJIA’s Q4 rally has been solid this year with DJIA up 15.0% as of today’s close. DJIA’s Q4 advance has pulled its 50-day moving average back above its 200-day moving average creating a historically bullish golden cross (1). However, momentum has turned negative with bearish signals from both the slower and faster moving MACD indicators applied to DJIA (2).

At the start of this week DJIA logged its fifteenth Down Friday/Down Monday (DF/DM) of 2022 (3). Historically DF/DM occurrences have been associated with market inflection points that frequently were followed by additional weakness. On some occasions such as the DF/DM in early October, the market had already experienced a sizable decline and the DF/DM was followed by a reversal in market direction and solid gains. Today’s trading action is satisfying the near-term bearishness while it remains to be seen if this week’s DF/DM will trigger another rally.

DJIA (3), S&P 500 (4) and NASDAQ (5) are currently on track to record their third straight weekly loss. Tech-heavy NASDAQ has been the weakest throughout the year and during the recent weekly losing streak. Compared to other weekly losing streaks earlier this year, the current streak has been relatively less severe thus far suggesting that overall selling pressure could be getting exhausted.

NYSE Weekly Advancers and Weekly Decliners (6) have remained consistent with the market’s overall moves. Weekly Decliners easily outnumbered Weekly Advancers during down weeks while the opposite was true in advancing weeks. The spike in Weekly Decliners during the first full week of trading in December was likely due to tax-loss selling as this year has produced numerous candidates.

Weekly New Highs (7) did briefly bounce back after declining throughout all of November, but it was a short-lived bounce. Weekly New Lows have bearishly crept higher but have remained subdued when compared to their peaks earlier in the year. This appears consistent with a market looking for its footing and clearer signals as to where to go in the near-term.

Weekly CBOE Put/Call ratios (8) have been steadily trending higher reaching 0.93 last week. Historically elevated levels approaching 1.00 have been observed near significant market bottoms. However, the rising popularity of zero days to expiration (0DTE) options is impacting this once reasonably reliable indicator. High levels of bearish sentiment make for easy put option sales.

The 30-year Treasury bond yield is still below the 90-day Treasury yield (9) as the bond market appears to be increasingly pricing in the probability that the Fed will overtighten and possibly trigger a recession. Historically a recession was broadly defined as two quarters of decline in GDP. That definition was meet in the first half of this year.

2023 Forecast

Base Case: 65% Probability – Current trends remain intact. Inflation continues to moderate at current pace and Fed pauses rate hikes in Q1. No recession, but a marked slowdown in growth and a modest increase in unemployment. Supply chains slowly continue to improve with gains from loosening China Covid-19 policy being held in check by higher infection rates. Slightly below average pre-election year gains of 10-15%.

Best Case: 25% Probability – Loosening China Covid-19 protocols accelerate supply chain recovery. Ukraine and Russia conflict ends. Inflation rapidly retreats allowing Fed to ease to a neutral policy stance. Recession is avoided, growth picks up, and unemployment remains low. Above average pre-election-year gains of 15-20%.

Worst Case: 10% Probability – Inflation persists, and Fed forced to tighten beyond current expectations which triggers a full-blown recession that is accompanied by historically declines in economic growth and a spike in unemployment. Current rally ends up being a bear market bounce. Final bear market bottom arrives in first half of 2023 with late Q3-Q4 rally that returns major indexes to 0-5% at yearend.

We expect pre-election 2023 to deliver the usual gains with the return of a new bull market. And our May 2010 Super Boom Forecast when the Dow was around 10,000 for the Dow to reach 38,820 by the year 2025 is still on track. (Page 104, Stock Trader’s Almanac 2023.)

Happy Holidays & Happy New Year, we wish you all a healthy and prosperous 2023!

|

2022 Free Lunch Stocks Served: 38 New Lows For Consideration

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 17, 2022

|

|

|

|

Our “Free Lunch” strategy is purely a short-term strategy reserved for the nimblest traders. Traders and investors tend to get rid of their losers near yearend for tax loss purposes, often driving these stocks down to bargain levels. Our research has shown that NYSE stocks trading at a new 52-week low on or about December 15 will usually outperform the market by February 15 in the following year. We have found that the most opportune time to compile our list is on the Friday of December quarterly options and index futures expiration – AKA Triple Witching Day.

This strategy takes advantage of several year-end patterns and indicators. First, the stocks selected are usually technically, deeply oversold and poised for a bounce, dead cat or otherwise. Second, all of the stocks are of the small- and mid-cap variety that will benefit from the January Effect which is the tendency for small-caps to outperform large-caps from mid-December through February. Lastly, the strategy spans the usually bullish Santa Claus Rally and the First Five Days of January.

To be included in this list, the stock must have traded at a new 52-week low on Friday, December 16, 2022. To remain on this year’s list, the stock had to still be trading at $1.00 or higher as several online trading platforms place additional restrictions on a trade when shares are below $1.00. Furthermore, the stock must have traded at least 100,000 shares on average over the past 20 days and have a market cap of at least $100 million, but not greater than $10 billion. Then, any stock that was not down 70% or more from its 52-week high to the 52-week low reached on Friday was also eliminated. Additionally, since the number of stocks making new 52-week lows on December 16, 2022, was large we screened for stocks that had trading volume on Friday that was 2x the average daily volume over the past 20 days on NYSE, AMEX and NASDAQ. No China domiciled companies are included on the list. Finally, preferred stocks, funds, splits, special high dividends, and new issues (less than 1-year trading) were eliminated. No stocks from the American Stock Exchange made the cut.

Our suggested guidelines for trading these Free Lunch stocks are to initiate a position at a price no greater or less than 3% of Friday’s closing price and to implement an 8% trailing stop on a closing basis from your execution prices. If the stock closes below 8% of the execution price or a subsequent high watermark, then the stock would be closed out of the portfolio. If any of these stocks trade in a window between -3% to +3% of Friday’s closing price on Monday, December 19, it will be tracked in the Almanac Investor Stock Portfolios using the trade’s execution price with an 8% trailing stop on closing basis.

If you buy these stocks, please note the following:

1. Consider selling them as soon as you have a significant gain and utilize stop losses.

2. The stocks all behave differently and there is no automatic trigger point to sell at.

3. Standard trading rules from the Almanac Investor Stock & ETF Portfolios do not apply for these stocks.

4. We think you should be out of all of these stocks between the middle of January and the middle of February.

5. Also, be careful not to chase these stocks if they have already run away.

DISCLOSURE NOTE: Officers of the Hirsch Organization do not currently own any of the shares mentioned. However, we may participate in the Free Lunch Strategy.

|

January Almanac & Vital Stats: Best Month of Pre-Election Year

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 15, 2022

|

|

|

|

January has quite a reputation on Wall Street as an influx of cash from yearend bonuses and annual allocations has historically propelled stocks higher. January ranks #1 for NASDAQ (since 1971), but sixth on the S&P 500 and DJIA since 1950. January is the last month of the best three-consecutive-month span and holds a full docket of indicators and seasonalities.

DJIA and S&P rankings did slip from 2000 to 2022 as both indices suffered losses in thirteen of those twenty-three Januarys with three in a row in: 2008 to 2010, 2014 to 2016 and then again from 2020 to 2022. January 2009 has the dubious honor of being the worst January on record for DJIA (-8.8%) and S&P 500 (-8.6%) since 1901 and 1930 respectively. Covid-19 spoiled January in 2020 & 2021 as DJIA, S&P 500, Russell 1000 and Russell 2000 all suffered declines in 2020. In 2021, DJIA, S&P 500 and Russell 1000 declined. This year surging inflation, reaching multi-decade highs, stoked fears of substantially higher interest rates in January.

Recent January weakness can be seen in the following chart. January has on average started out positive with DJIA, S&P 500, NASDAQ, Russell 1000 and 2000 all logging gains in the first half of the month, but weakness then creeps in. From around the seventh trading day to the end of the month declines have prevailed over the last 21-years.

However, in pre-election years, Januarys have been outright stellar ranking #1 for S&P 500, NASDAQ, Russell 1000, and Russell 2000 and #2 for DJIA. Average gains range from 3.4% by Russell 1000 to a whopping 6.8% for NASDAQ. DJIA and S&P 500 have only declined twice in pre-election Januarys, 2015 and 2003.

On pages 112 and 114 of the Stock Trader’s Almanac 2023 we illustrate that the January Effect, where small caps begin to outperform large caps, actually tends to start in mid-December. Historically, the majority of small-cap outperformance is normally done by mid-February, but strength can last until mid-May when major indices typically reach a seasonal high.

The first indicator to register a reading in January is our Santa Claus Rally. The seven-trading day period will begin on the open on December 23 and ends with the close of trading on January 4. Normally, the S&P 500 posts an average gain of 1.3%. The failure of stocks to rally during this time has tended to precede bear markets or times when stocks could be purchased at lower prices later in the New Year.

On January 9, our First Five Days “Early Warning” System will be in. In pre-election years this indicator has a respectable record. In the last 18 pre-election years 13 full years followed the direction of the First Five Days. The full-month January Barometer has an even better record in pre-election years with 15 of the last 18 full years following January’s direction.

Our flagship indicator, the January Barometer created by Yale Hirsch in 1972, simply states that as the S&P goes in January so goes the year. It came into effect in 1934 after the Twentieth Amendment moved the date that new Congresses convene to the first week of January and Presidential inaugurations to January 20.

The long-term record has been solid, an 83.3% accuracy rate, with 12 major errors since 1950. Major errors occurred in the secular bear market years of 1966, 1968, 1982, 2001, 2003, 2009, 2010 and 2014 and again in 2016 as a mini bear came to an end. The tenth major was in 2018 as a hawkish Fed continued to hike rates even as economic growth slowed and longer-term interest rates fell. Historical levels of support from the Fed and Federal governments in 2020 quickly undid the market damage caused by the Covid induced economic shutdown. 2021 was the 12th major error for the January Barometer. The market’s position on the last trading day of January will give us a better read on the year to come. When all three of these indicators agree it has been prudent to heed their call.

|

January 2023 Strategy Calendar

|

|

By:

Christopher Mistal

|

December 15, 2022

|

|

|

|

|

Stock Portfolio Update: Mid-December is Key

|

|

By:

Christopher Mistal

|

December 08, 2022

|

|

|

|

Next week is going to be a busy week for the market. Not only is the Fed meeting for the last time this year, but it is also quarterly options expiration week. Before the Fed meets PPI will be released tomorrow followed by CPI on December 13. Expectations for both inflation reports are for a continuation of the moderating trend that began in Q3. It seems most plausible that there will be no significant surprise in either inflation report and the Fed will proceed with its well telegraphed 0.5% increase in the Fed’s fund rate to a new range of 4.25-4.50%.

At that point, all eyes and ears are going to focus on the press conference and the updated rate dot plot. Any sign of higher and/or longer for interest rates is not going to be well received by the market. However, we believe the Fed is likely to continue to shift towards a more dovish stance with monetary policy which could be sufficient to reignite the rally into yearend and beyond.

Seasonally speaking,

mid-December has also been a major inflection point for the market. Over the last 21-years, the market typically begins its march higher on or around the tenth trading day of December. This year the tenth trading day is December 14, the same day as the Fed announcement. It is also around this point in December that tax-loss selling pressure begins to abate. We remain bullish and look for additional confirmation for this stance from the market next week.

Stock Portfolio Updates

Over the last five weeks since last update through yesterday’s close, S&P 500 advanced 4.7% while Russell 2000 climbed 2.6%. Over the same period the entire stock portfolio was 0.7% lower, excluding dividends and any fees. Overall portfolio performance was weighted down by declines in numerous energy related positions as energy prices declined. After adding the 16 new positions presented in early November, the cash balance in the portfolio is still around 40% of total holdings. We are not targeting a specific amount of cash, but we do want to retain some to participate in this year’s upcoming “Free Lunch” basket that we will be emailed to members before the market opens for trading on December 19.

Energy’s continued weakness appears to be driven by China’s ongoing Covid-19 lockdowns and renewed domestic recession concerns. China does appear to be easing up on some of its most restrictive measures following recent protests. And despite the seemingly relentless calls for a recession sometime next year, economic data has remained relatively firm. There have been numerous layoff announcements, but overall employment numbers have held up so far. Economic growth forecasts also appear to be improving with the Atlanta Fed’s GDPNow model projecting Q4 growth of 3.4%. Absent a significant increase in domestic energy production, the current decline in energy prices is not likely to continue for much longer.

Comstock Resources (CRK) was stopped out on December 5, when it closed below $15.75. CRK was closed out of the portfolio the following day at its average daily price of $14.81 for a 18.1% loss. Declining natural gas price and the conversion of preferred shares to common shares are the most likely causes for the decline. CRK was down again today even as natural gas bounced higher. Diamondback Resources (FANG) closed below its stop loss today. It will be closed out of the portfolio in the next update. All energy positions are on Hold.

Outside of energy, many existing and new positions have performed rather well given the choppy trading so far this month. MGP Ingredients (MGPI) recently traded at a new all-time high above $125 on December 1. Accounting for the sale of half the original position in MGPI when it first doubled, the overall gain was 141.7% as of the close on December 7. MGPI is on Hold.

Northwest Pipe (NWPX) is another notable standout, trading at a new 52-week high earlier this month. As its name suggests, NWPX makes steel pipe and precast piping solutions used in a variety of applications. Its primary application is water related infrastructure products which is another area of U.S. infrastructure that needs upgrading and improvement. Hopefully some of the federal infrastructure funds do get allocated water system projects. NWPX is on Hold.

In the Mid-cap portfolio, five of the six newly added positions had modest gains at the December 7, close. Digi International (DGII) was the only position with a mild loss of 0.5%. All six positions presented on November 10, can still be considered on dips below their respective buy limits or at current levels.

Large-cap positions, on average, held up best over the last five weeks. Amdocs (DOX) traded within a few cents of its 52-week high earlier this month and is up 39%. Recently added Steel Dynamics (STLD) also had a solid five weeks gaining 10% since addition to the portfolio. All new trade ideas presented on November 10, excluding energy related companies, can be considered on dips below their respective buy limits or near current levels.

Please see table below for updated advice, suggested buy limits and stop losses.

Disclosure note: Officers of Hirsch Holdings Inc hold positions in CEIX, CRK, EPSN, MUR, PR, QRHC & WTI in personal accounts.

|

ETF Trades: Not So Bad December & Energy Sector on Radar

|

|

By:

Christopher Mistal & Jeffrey A. Hirsch

|

December 01, 2022

|

|

|

|

There was a stat floating around the internet and business news channels this week that stated when the S&P 500 was down 15% or more year-to-date (YTD) on November 30, December was down >2% on average. We ran the numbers yesterday before the big rally on Fed Chair Powell’s “makes sense to moderate the pace of our rate increases” comments yesterday at the Brookings Institute.

What we found was that most of the carnage after November YTD losses > 15% occurred in the Great Depression years and since WWII December has performed much better after a down >15% YTD November. During the Depression after November YTD >15% losses December was down 3 of 4 with an average loss of -5.4%. In the six years since 1939 with November YTD >15% losses December was up 3, down 3 with an average loss of -0.3%.

But with the big 3.1% gain in the S&P 500 on November 30, the YTD loss receded above the -15% mark to -14.4% on the heels of a 5.4% gain for the month, which is also a 14.1% rally off the October 12 low. And this marks the first back-to-back monthly gains of over 5% each month since August 2020, the ones before that were in March-May 2009. It’s the 14th such occurrence since 1950. The previous 13 all occurred in bull markets.

Now, when the S&P 500 is down YTD November less than 15%, December’s performance is not so bad at all, just a tad below the average 1.6% to 1.1%, up 17 of 23 or 74% of the time. We still expect some chop as the bull market finds its footing, but we remain bullish and anticipate the yearend rally to continue to climb the proverbial “wall of worry” and for the Santa Claus Rally to come to town later this month.

New December Sector Seasonality

Oil companies typically come into favor in mid-December and remain so until late April or early May in the following year (highlighted with yellow box in following chart). This trade has averaged 11.2%, 8.0%, and 6.6% over the last 25-, 10-, and 5-year periods respectively. Sizable declines in 2017 and 2020 have depressed average performance in the most recent periods when compared to the 25-year period. Seasonal strength in crude oil companies has also been ending sooner, typically in late April or early May instead of late June or July over the past ten years. As a reminder, this seasonality is not based upon the commodity itself (crude oil or natural gas); rather it is based upon NYSE ARCA Oil & Gas index (XOI). This price-weighted index is composed of major companies that explore and produce oil and gas.

![[NYSE Arca Oil Index (XOI) Weekly Bars and Seasonal Pattern since 11/9/1984]](/UploadedImage/AIN_0123_20221201_XOI.jpg)

Both crude oil and natural gas prices have retreated from their respective Russian invasion of Ukraine driven peaks earlier this year as Covid-19 lockdowns in China and on-again/off-again recession fears have weighed on demand expectations. However, actual demand energy has remained relatively firm. Absent meaningful improvement to the supply side prices for energy are likely to remain firm and creep higher. Any disruptions to current supplies could easily send prices spiking higher.

SPDR Energy (XLE) is the top pick to trade this seasonality. A new position in XLE could be considered near current levels up to the buy limit of $91.25. Employ an initial stop loss of $79.62. Consider taking profits at the auto sell of $121.76. Exxon Mobil is the top holding in XLE at 22.84%. The remaining top five holdings of XLE are Chevron, Schlumberger, EOG Resources and ConocoPhillips. For tracking purposes, XLE will be added to the portfolio using its average daily price on December 2.

Sector Rotation ETF Portfolio Updates

After a mixed start in October, the Sector Rotation portfolio picked up momentum in November. Average performance across all positions held has risen to 11.5% as of the close on November 30. In the prior update, the average performance was 2.5%. As a result of the gains, stop losses for all previous holdings have been adjusted higher. Please see table below for new suggested stop losses for each position.

There is just one position in the red in the portfolio, SDPR S&P Biotech (XBI). This is a long-term holding, and we will add to or trim when opportunities present. XBI did participate in the rally which is encouraging. We hold the belief that at some point in the (near) future cures for diseases will become more prevalent than treatments. The companies held by XBI are some of the best candidates to fulfill this belief. XBI can still be considered on dips below its buy limit.

Semiconductors have had a challenging year. Our short position worked out quite well, but the subsequent long trade did not as it was stopped out for a modest loss. Last month’s second attempt at a long in iShares Semiconductor (SOXX) also did not pan out as it never traded below our buy limit. With historical seasonal strength in semiconductors coming to an end later this month and SOXX having already made a sizable move, we are cancelling this long trade at this time.

Somewhat surprising, the second weakest position in the portfolio is iShares Consumer Discretionary (XLY) with a 3.1% gain. Yes, the consumer is facing numerous headwinds ranging from elevated energy prices and inflation to sizable increases in interest rates, but the numbers from Black Friday/Cyber Monday suggest the consumer still has the means. XLY has also been held in check by sizable positions in its top two holdings, Amazon, and Tesla. XLY can still be considered on dips.

All other positions in the portfolio are on hold. Please see the following table for current advice and updated stop losses.

Tactical Seasonal Switching Strategy ETF Portfolio Updates

Results from SPDR DJIA (DIA), SPDR S&P 500 (SPY), Invesco QQQ (QQQ), and iShares Russell 2000 (IWM) have improved nicely since last update. The portfolio’s average gain was 9.1% as of November 30 close compared to 1% prior month. DIA is the top performing position, up 14.7% since our seasonal buy signal on October 4. SPY and IWM also have solid gains of 8.7% and 8.1% respectively. QQQ is still the laggard, but much improved. All four positions are on Hold. As a reminder, officially the “Best Months” strategy does not employ stop losses on these positions. If this risk exceeds one own personal level, a stop loss could be utilized.