|

March 2019 Trading & Investment Strategy

|

|

By:

|

February 28, 2019

|

|

|

|

|

Market at a Glance - 2/28/2019

|

|

By:

Christopher Mistal

|

February 28, 2019

|

|

|

|

2/28/2019: Dow 25916.00 | S&P 2784.49 | NASDAQ 7532.53 | Russell 2K 11575.55 | NYSE 12644.81 | Value Line Arith 6226.17

Psychological: Skeptical. According to

Investor’s Intelligence Advisors Sentiment survey bulls are at 52.4%. Correction advisors are at 27.2% and Bearish advisors are 20.4%. Typically at these levels, we would interpret sentiment to be somewhat excessively bullish however, given the markets nine-week winning streak it is surprising there are not even more bulls. This suggest that there may still be a healthy amount of doubt (and capital on the sidelines) that could fuel the market even higher.

Fundamental: Mostly firm. U.S. growth is still expected to slow due to the fading effects of tax cuts, but it is not forecast to fall off a cliff. Corporate earnings will also slow as year-over-year comparisons are tougher. However, employment is still firm with 304,000 net new jobs added in January while inflation is remaining largely in check. Housing and autos are still challenged due to higher interest rates than in the recent past. Recent stabilization in rates could provide some aid to confidence and the overall economy.

Technical: Recovering. DJIA, S&P 500, NASDAQ and Russell 2000 continued to climb throughout February. DJIA, S&P 500 and NASDAQ have all reclaimed their respective 200-day moving averages, Russell 2000 is currently struggling with this key level. Respective 50-day moving averages have turned up. Further gains will be needed to drive the 50-day moving average back above the 200-day moving average. NYSE and S&P 500 cumulative daily advance/decline lines have bullishly climbed back above previous highs.

Monetary: 2.25-2.50%. Even though we have heard from some Fed officials since their last meeting in January, they all appear to be sticking to a more dovish tone regarding future potential rate increases. The next Fed meeting on March 19-20, will provide additional clarity. Until then, the new status quo will likely not change.

Seasonal: Bullish. In March the market tends to perform better in the first half than the second half. In pre-election years March has historically performed better than average with DJIA and NASDAQ ranking climbing to fourth best (S&P 500 is unchanged). Russell 2000 March performance improves to third best.

|

March Outlook: Rally Intact Pausing at Resistance & Seasonal Weak Spots

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

February 28, 2019

|

|

|

|

Since Christmas the market has ripped higher on supportive market internals, still solid overall fundamentals and improving technicals. In line with our Seasonal Market Probability Calendar (graphically represented on page 20 of the

Stock Trader’s Almanac 2019 in the “February Almanac” and

here on the blog) the market succumbed to usual February weakness after the first few days of the month and again around the Presidents’ Day holiday and again today on the usually bearish last trading day of the month.

The two yellow boxes in the chart highlight the seasonal weak spots mentioned above from the 4th-7th trading days of February, around Presidents’ Day and on the last trading day of the month. After diving through the August 2017 low support level and then springing back up through it on Christmas, the market paused at the February 2018 low resistance level and again at the October-November 2018 lows that were blown out in December. Now that we have cleared the 200- and 50-Day Moving Averages we have the aforementioned November high at 2815 to clear before we can attack new all-time highs.

![[S&P Chart]](/UploadedImage/AIN_0319_20190228_S&P_Resistance.jpg)

We don’t expect to take out the old high so fast. More likely we will dance around this 2815-level for a few months. Early March strength should push us above this level, but then end-of-March weakness is likely to retest this level again. Provided we avoid any unexpected geopolitical snafus the all-time highs could be tested in Q2 and perhaps exceeded, followed by backing and filling in Q3. Then we expect the market to make another run at new highs in the 4th quarter where many Pre-Election Year highs have been logged over the years.

Overall our outlook remains positive. Seasonal indicators are strong with our January Indicator Trifecta positive 3-for-3 and the Best Six Months back in the black up about 3% across the board after a wild ride at the end of 2018. The market has impressively digested the dynamic news flow so far this year and a look at the “Pulse” below highlights a much improved market internal environment. NYSE Advance-Decline made new highs recently illustrating the broad participation in the rally.

There will be bumps and volatility this year, most likely around the end of March and during the Worst Four Months July-October. But in the end we expect solid gains for 2019.

Pulse of the Market

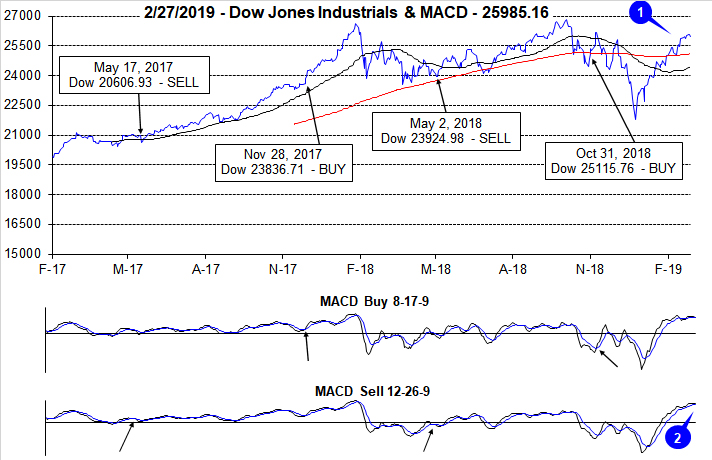

DJIA’s advance off the December bottom continued in February with better than average pre-election year gains (1). DJIA has reclaimed its 200-day moving average (solid red line in top chart) and its 50-day moving average is also heading higher. If DJIA’s 50-day moving average continues to climb, it will eventually cross back above the 200-day moving average to form a bullish golden cross. The pace of gains did slow when compared to January’s move which is reflected in both the faster and slower moving MACD indicators (2). Due to this slowing in momentum the faster moving MACD indicator turned negative yesterday. The slower moving MACD “Sell” indicator however, is still positive.

Another DJIA Dow Friday/Down Monday (DF/DM) did occur in early February (3), but much like the early January occurrence there has yet to be any meaningful follow through on this historically bearish sign. DJIA and NASDAQ (5) have extended their weekly winning streaks to nine straight. S&P 500 has been up in eight of the past nine weeks (4). The last time DJIA recorded a streak of nine or more straight weekly gains was in 1995 and there have only been

twelve other streaks of nine or more straight weeks since 1901. When these streaks end, it is usually followed by a brief period of consolidation, but after a month or so the rally has usually resumed.

Market breath measured by NYSE Weekly Advancers and NYSE Weekly Decliners has been bullish since late December with Advancers outnumbering Decliners by wide margins in eight of the last nine weeks (6). As a result, the NYSE cumulative advance/decline line is now higher than it was last September when the market was making new all-time highs. This is a bullish sign that suggests further market gains are probably.

Bullishly, New Weekly Highs have slowly been expanding while New Weekly Lows have remained subdued (7). As the rally continues and the market climbs closer to its previous highs, New Weekly Highs should continue to increase in number.

Consistent with recent commentary from FOMC members, short- and long-term interest rates (8) have stabilized. The 90-day Treasury rate has ticked slightly higher to 2.41 but is not expected to make any major move higher while the 30-year Treasury has remained right around 3.00% for the last ten weeks.

Click for larger graphic…

|

March Almanac & Vital Stats: Even Better in Pre-Election Years

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

February 21, 2019

|

|

|

|

Turbulent March markets tend to drive prices up early in the month and batter stocks at month end. Julius Caesar failed to heed the famous warning to “beware the Ides of March” but investors have been served well when they have. Stock prices have a propensity to decline, sometimes rather precipitously, during the latter days of the month. In March 2001, DJIA plunged 1469 points (-11.8%) from March 9 to the 22.

March packs a rather busy docket. It is the end of the first quarter, which brings with it Triple Witching and an abundance of portfolio maneuvers from The Street. March Triple-Witching Weeks have been quite bullish in recent years. But the week after is the exact opposite, DJIA down 21 of the last 31 years—and frequently down sharply for an average drop of 0.50%. In 2018, DJIA lost 1413 points (–5.67%) Notable gains during the week after for DJIA of 4.9% in 2000, 3.1% in 2007, 6.8% in 2009, and 3.1% in 2011 are the rare exceptions to this historically poor performing timeframe.

Normally a decent performing market month, March performs even better in pre-election years (see Vital Statistics table below). In pre-election years March ranks: 4th best for DJIA, S&P 500, NASDAQ and Russell 1000 (January, April and December are better). Pre-election year March rank #3 for Russell 2000. Pre-election year March has been up 13 out of the last 14 for DJIA. In fact, since inception in 1979, the Russell 2000 has a perfect, 10-for-10 winning record.

Saint Patrick’s Day is March’s sole recurring cultural event. Gains the day before Saint Patrick’s Day have proved to be greater than the day itself and the day after. Perhaps it’s the anticipation of the patron saint’s holiday that boosts the market and the distraction from the parade down Fifth Avenue that causes equity markets to languish. Or maybe it’s the fact that Saint Pat’s usually falls in historically bullish Triple-Witching Week.

Whatever the case, since 1950, the S&P 500 posts an average gain of 0.19% on Saint Patrick’s Day (or the next trading day when it falls on a weekend), a gain of 0.13% the day after and the day before averages a 0.24% advance. S&P 500 median values are 0.17% on the day before, 0.07% on Saint Patrick’s Day and –0.19% on the day after. In the eleven years when St. Patrick’s Day falls on a Saturday, like this year, since 1950, the day before (Friday) produced an average gain of 0.21%, while Monday advanced an average 0.13%.

| March (1950-2018) |

| |

DJI |

SP500 |

NASDAQ |

Russell

1K |

Russell 2K |

| Rank |

|

5 |

|

4 |

|

6 |

|

4 |

|

4 |

| #

Up |

|

44 |

|

44 |

|

30 |

|

26 |

|

29 |

| #

Down |

|

25 |

|

25 |

|

18 |

|

14 |

|

11 |

| Average

% |

|

1.1 |

|

1.2 |

|

0.8 |

|

1.1 |

|

1.4 |

| 4-Year Presidential Election Cycle Performance

by % |

| Post-Election |

|

0.3 |

|

0.6 |

|

-0.2 |

|

0.7 |

|

1.1 |

| Mid-Term |

|

1.0 |

|

1.1 |

|

1.3 |

|

1.6 |

|

2.7 |

| Pre-Election |

|

2.0 |

|

1.9 |

|

3.1 |

|

2.0 |

|

3.1 |

| Election |

|

1.0 |

|

1.2 |

|

-0.9 |

|

0.1 |

|

-1.1 |

| Best & Worst March by % |

| Best |

2000 |

7.8 |

2000 |

9.7 |

2009 |

10.9 |

2000 |

8.9 |

1979 |

9.7 |

| Worst |

1980 |

-9.0 |

1980 |

-10.2 |

1980 |

-17.1 |

1980 |

-11.5 |

1980 |

-18.5 |

| March Weeks by % |

| Best |

3/13/09 |

9.0 |

3/13/09 |

10.7 |

3/13/09 |

10.6 |

3/13/09 |

10.7 |

3/13/09 |

12.0 |

| Worst |

3/16/01 |

-7.7 |

3/6/09 |

-7.0 |

3/16/01 |

-7.9 |

3/6/09 |

-7.1 |

3/6/09 |

-9.8 |

| March Days by % |

| Best |

3/23/09 |

6.8 |

3/23/09 |

7.1 |

3/10/09 |

7.1 |

3/23/09 |

7.0 |

3/23/09 |

8.4 |

| Worst |

3/2/09 |

-4.2 |

3/2/09 |

-4.7 |

3/12/01 |

-6.3 |

3/2/09 |

-4.8 |

3/27/80 |

-6.6 |

| First Trading Day of Expiration Week: 1990-2018 |

| #Up-#Down |

|

20-9 |

|

20-9 |

|

16-13 |

|

18-11 |

|

17-12 |

| Streak |

|

D2 |

|

D1 |

|

U6 |

|

D1 |

|

U2 |

| Avg

% |

|

0.2 |

|

0.1 |

|

-0.2 |

|

0.05 |

|

-0.2 |

| Options Expiration Day: 1990-2018 |

| #Up-#Down |

|

15-14 |

|

18-11 |

|

13-16 |

|

16-13 |

|

12-16 |

| Streak |

|

U1 |

|

U1 |

|

U4 |

|

U1 |

|

U4 |

| Avg

% |

|

0.2 |

|

0.1 |

|

-0.1 |

|

0.08 |

|

-0.05 |

| Options Expiration Week: 1990-2018 |

| #Up-#Down |

|

21-8 |

|

21-8 |

|

18-11 |

|

20-9 |

|

16-13 |

| Streak |

|

D1 |

|

D1 |

|

D1 |

|

D1 |

|

D1 |

| Avg

% |

|

1.0 |

|

0.8 |

|

0.01 |

|

0.8 |

|

0.3 |

| Week After Options Expiration: 1990-2018 |

| #Up-#Down |

|

10-19 |

|

7-22 |

|

13-16 |

|

7-22 |

|

13-16 |

| Streak |

|

D4 |

|

D7 |

|

D6 |

|

D7 |

|

D7 |

| Avg

% |

|

-0.5 |

|

-0.4 |

|

-0.1 |

|

-0.4 |

|

-0.1 |

| March 2019 Bullish Days: Data 1998-2018 |

| |

1,

15, 19, 20 |

1,

5, 13, 15, 19 |

1,

5, 13, 18-20 |

1,

5, 13, 19 |

13, 19, 25, 29 |

| |

|

|

25 |

|

|

| March 2019 Bearish Days: Data 1998-2018 |

| |

21,

22, 26 |

14,

21, 26 |

4,

26 |

14,

21, 26 |

26 |

| |

|

|

|

|

|

|

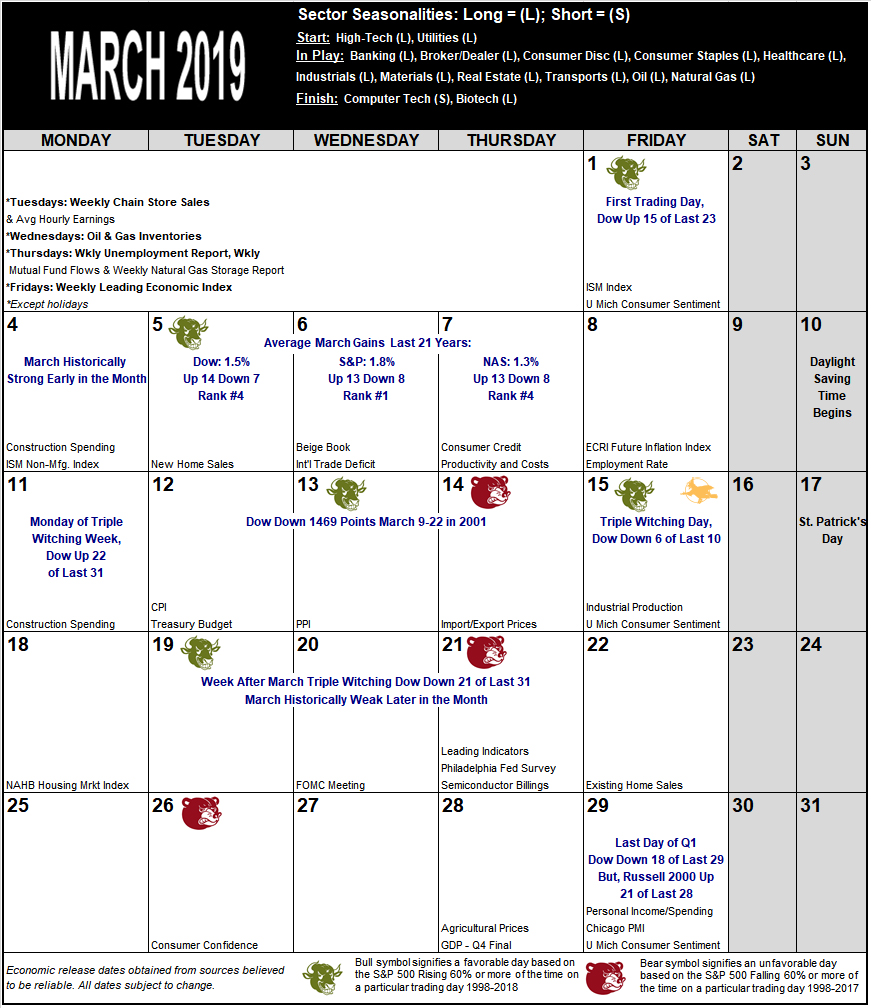

March 2019 Strategy Calendar

|

|

By:

Christopher Mistal

|

February 21, 2019

|

|

|

|

[Editor's Note: Due to partial Federal Government Shutdown, several key economic releases do not appear on the March calendar because no release date is currently available.]

Click here to download printer friendly pdf file of March Strategy Calendar...

|

Stock Portfolio Update: Strong Market Gains Are A Strong Indication

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

February 14, 2019

|

|

|

|

One of the basic stock market indicators is the market itself. A market like we are experiencing right now with powerful gains following a deep fast correction is a positive indication in and of itself. Several colleagues have been expounding lately on the record following such gains. LPL Financial Senior Market Strategist Ryan Detrick put out some research showing the last five times since WWII that the S&P 500 was up 10% year-to-date (YTD) in February and the gains for the rest of the year were strong, except for pesky 1987.

Sam Stovall, Chief Investment Strategist at CFRA Research pointed out in his latest note that if the S&P 500 posted a gain for February, “it would trigger an encouraging signal for the entire year.” Sam observed that of the 28 years since WWII when the S&P 500 gained ground in both January and February, “In 100% of these observations, the S&P 500 was up for the full year and recorded an average total return of nearly 24%. What's more, the S&P 500 was higher in the remaining 10 months of the year 93% of the time, returning an average 13.5%.”

We wanted to dig a little deeper. So I expanded the YTD study beyond 10% gains to examine a larger data set and ran the data on consecutive up January and February using the cash S&P 500 index instead of the “total return” index and overlaid both with the positive January Indicator Trifectas, when the Santa Claus Rally, the First Five Days and the full-month January Barometer are all positive. In the tables below positive January Trifecta years are highlighted in grey.

At yesterday’s close February 13 the S&P 500 was up 9.8% YTD. The top 30 YTD gains at the February high are ranked by gain in Table 1. S&P 500 tacked on gains in 25 of those 30 years for an averages gain of 11.3%. Overlay the Trifecta and two losses disappear.

In Table 2 of the 27 years that the S&P 500 gained ground in both January and February since WWII there is only one full year loss on the S&P cash index in 2011 and it’s puny, and there are only 2 losses in the following March-December period in 1987 and 2011 – both were in Trifecta years.

So, no matter how you slice it, gains earlier in the year are generally a solid indication for gains the rest of the year.

Stock Portfolio & Free Lunch Update

Over the last four weeks since last update, S&P 500 climbed 5.2% through yesterday’s close while Russell 2000 added 6.1% over the same time frame. Overall, the entire Stock Portfolio rose 2.5% excluding any dividends or trading fees. Large-Caps performed best, up 6.1% as defensive positions continued to perform and recent additions improved. Small-Caps were second best advancing 1.9%. Gains here came from remaining Free Lunch positions. Mid-Caps enjoyed a 1.6% advance.

Our Free Lunch strategy this year has been a resounding success. The entire basket, including closed positions, through yesterday’s close was up an average 27.8% compared to gains of 13.0% for NYSE Comp and 17.2% for NASDAQ. NYSE-listed positions have enjoyed the largest gains, up 29.5% on average. NASDAQ positions have also done well, up 27.1%.

Many of the original positions have been stopped out, but that is the nature of the strategy. Free Lunch is a short-term trade with a different set of guidelines that takes advantage of yearend selling for tax reasons, the January Effect of small-cap outperformance, the Santa Claus Rally and the First Five Days. Free Lunch stocks were not purchased for typical reasons and typically their holding period is brief. As of the close on February 13, just five of the twenty-three Free Lunch stocks remained in the portfolio; OMI, GTHX, NNBR, PRTK and UCTT. Continue to hold these positions with an 8% trailing stop loss, updated using daily closing price.

Remaining positions from last June’s defensive basket (Presented Date of 6/14/2018) also continue to contribute to the portfolios overall performance with price appreciation (measured in results) and dividends (not included in performance tracking). These eleven remaining defensive positions are all positive with an average gain of 17.2%. McCormick & Company (MKC), once the performance leader of this group, was stopped out on January 24 the day after earnings narrowly missed expectations.

December’s Seasonal Sector Trades that were presented to take advantage of strength in copper have been added to the portfolio. Freeport-McMoRan (FCX) and Southern Copper (SCCO) were both added on December 13, 2018, as both opened the trading day below their respective buy limits. FCX and SCCO are on Hold.

All other positions in the portfolio are on Hold. Please see portfolio table below for Current Advice and Stop Losses.

|

Seasonal Sector Trades: Gold & Silver Rally Running into Resistance

|

|

By:

Christopher Mistal & Jeffrey A. Hirsch

|

February 07, 2019

|

|

|

|

Historically silver has a seasonal tendency to peak in February, most notably so in 1980 when the Hunt Brothers’ plot to corner the silver market was foiled. Our seasonal analysis shows that going short on or about February 20 and holding until about April 25 has worked 35 times in the last 46 years for a win probability of 76.1%. As you can see in the short silver table, the usual February silver break was trumped by the overarching precious metal bull market of 2002–2011 just four times in ten years.

![[February Short Silver (May) Trade History]](/UploadedImage/AIN_0319_20190207_SI_History.jpg)

After suffering losses for two years in a row in 2010 and 2011, this trade returned to success with its second best performance in 2012 as precious metals in general fell out of favor. This trade was then successful in 2013, 2014 and 2015. A shaky start for stock markets in early 2016 combined with multi-year lows for silver sparked fresh demand for the metal resulting in a loss that year, but this trade returned to success in 2017 and again in 2018. Last year, sizable gains could have been realized with a longer holding period as silver retreated in earnest after mid-June.

![[Silver (SI) Weekly Bars (Pit Plus Electronic) and 1-Yr Seasonal Pattern]](/UploadedImage/AIN_0319_20190207_SI_Seasonal.jpg)

In the above chart, silver’s weekly price bars appear in the top half of the chart and silver’s seasonal trend since 1972 appears in the bottom half. Typical seasonal weakness is highlighted in yellow. Historically, silver has declined from late-February/early-March until the end of June. This year, typical seasonal weakness has yet to materialize, but silver does appear to be running into some resistance just above $16 per ounce. Just above $16 per ounce was a key support level silver held for much of the spring last year before breaking down. Silver could continue to rally modestly higher, so we will want to see signs of weakness before executing any trade.

![[ProShares UltraShort Silver Daily Bar Chart]](/UploadedImage/AIN_0319_20190207_ZSL.jpg)

ProShares UltraShort Silver (ZSL) is an inverse (bearish) ETF that seeks to return two times the inverse of the daily performance of silver bullion priced in U.S. dollars for delivery in London and is one choice to trade this seasonality in the Almanac Investor Sector Rotation ETF Portfolio. Average daily trading volume can be light, but when silver does make a move lower, trading activity in ZSL generally does expand quickly. ZSL can be considered on dips below $33.05. If purchased, an initial stop loss of $30.08 is suggested.

Gold’s Sympathy Slide

Seasonally, there is also a weak price period for gold from mid-February until mid to late June. Entering a short position on or about February 20 and holding until March 15 has been a successful trade 27 times in the past 44 years for a success rate of 61.4% with a cumulative profit of $45,140 per futures contract. However, in recent years holding onto the short position established in February longer has been the more profitable trade.

The chart below is a weekly chart of the price of gold with the exchange-traded note (ETN) known as DB Gold Double Short (DZZ) overlaid to show the inverse price correlation between the two trading vehicles. The line on the bottom section is the 44-year average seasonal tendency showing the market’s directional price trend with seasonal weakness highlighted in yellow. DZZ trades 2x the inverse of the daily price change of a single gold futures contract.

As you can see in this next chart, DZZ has been trending lower as gold moves higher. Gold is also closing in on potential resistance near $1350 per ounce. This is right around the price were gold stalled last year in February and again in April. DZZ could be considered on dips below $5.35. If purchased a stop loss of $4.87 is suggested.

Both of today’s new trade ideas will be tracked in the Almanac Investor Sector Rotation ETF Portfolio.

|

ETF Portfolio Updates: Market Takes a Breather

|

|

By:

Christopher Mistal

|

February 07, 2019

|

|

|

|

Broad market strength persisted throughout the month of January into February. As of today’s close, DJIA and S&P 500 are up 7.9% year-to-date. NASDAQ is even stronger, up 9.8%. Gains since the market’s December 24th closing low now exceed 15%. Thus far the market’s performance suggests a classic “v” bottom has occurred. DJIA, S&P 500 and NASDAQ all have rebounded back above their respective 50-day moving averages and DJIA has even reclaimed its 200-day moving average.

![[DJIA Daily Bar Chart]](/UploadedImage/AIN_0319_20190207_DJIA.jpg)

![[S&P 500 Daily Bar Chart]](/UploadedImage/AIN_0319_20190207_SP500.jpg)

![[NASDAQ Daily Bar Chart]](/UploadedImage/AIN_0319_20190207_NASDAQ.jpg)

Although today’s trading was negative there were some positives. First, DJIA still closed above its 200-day moving average. Second, all the major indexes did recover modestly by the close. This does not guarantee that weakness will end abruptly, but it does suggest a repeat of December’s rout is not highly probable. More likely is a period of reflection and consolidation following the sizable move the market has made over the last six weeks. Technical indicators such as MACD, Stochastics and relative strength are stretched and in need of a reset. Once that occurs and provided economic data and news flow remains supportive, then the rally will likely resume.

Sector Rotation ETF Portfolio Updates

Last update in early January, we elected to cautiously re-enter many of the positions that were stopped out in December. Some of our suggested buy limits worked well while others ultimately proved to conservative. As a result, IYW, IBB, XLB and XLE were added to the portfolio. XLF, XLP, XLY, XLV, XLI, VNQ and IYT remain open positions. Given the magnitude of the recent rally and February’s historical tendency of being the weak link in the “Best Months,” we are not going to change buy limits for the open positions at this time. Should we get a period of consolidation, a better buying opportunity is possible.

At the top of the Sector Rotation ETF Portfolio, December’s trade ideas in copper now appear. United States Copper (CPER) and Global X Copper Miners (COPX) were both added when they traded below their buy limits back in mid-December. CPER and COPX are on Hold.

Last month’s new trade ideas in natural gas have also been added to the portfolio. FCG is flat while UNG is currently down 3%. The wild temperature swings experienced in the Midwest and Northeast have translated into wild price swings by natural gas. Natural gas inventories are well below the 5-year average for this time of the year which should be supportive of prices.

The fourth quarter correction in 2018 has improved the prospects for this year. Valuations have shrunk to more attractive levels. The decline in price also improves the odds of typical pre-election year gains. There is also plenty of time remaining in the current Best Six/Eight Months to recoup last quarter’s losses and possibly more.

Tactical Switching Strategy Update

Per last month’s advice, we added to existing positions in DIA, IWM, QQQ and SPY on January 11. All four positions opened below their respective buy limits. Because of the additional purchases the presented price has been adjusted. With the additional purchases, at a lower price, the overall gain in the TSS Portfolio is 3%. All positions in the TSS Portfolio are now on Hold.