|

Market at a Glance - 7/30/2020

|

|

By:

Christopher Mistal

|

July 30, 2020

|

|

|

|

7/29/2020: Dow 26539.57 | S&P 3258.44 | NASDAQ 10542.90 | Russell 2K 1500.63 | NYSE 12669.62 | Value Line Arith 6262.01

Fundamental: Improving. Yes, improving. Q2 GDP advance estimate showed a decrease of 32.9%, but this was considerably better than early June projections 40-50% decreases. This was the worst quarterly decline on record. For reference the worst quarter during the financial crisis of 2008-2009 was less than a third of that. Because of that massive decline and a clear desire not to fully shut down again, the worst is most likely in the rearview mirror. Weekly jobless claims are also well off their peak, although they have picked up slightly and remain above 1 million as many areas of the economy remain closed or are taking steps backwards. The low bar for corporate earnings also appears to be overly pessimistic.

Technical: Divergent. NASDAQ trading at new all-time highs. S&P 500 positive year-to-date and DJIA is trailing both. This divide is also in the overall economy and is likely to persist until the pandemic fades into history. All three indexes are bullishly above their respective 50- and 200-day moving averages. NASDAQ and S&P 500 are strongest with their 50-day moving averages above their 200-day moving averages. Previous highs are likely to prove formidable resistance for DJIA and S&P 500. NASDAQ’s concerns are earnings, guidance and valuation.

Monetary: 0 – 0.25%. At its meeting earlier this week the Fed attempted to be cautiously optimistic. They noted activity has picked up since the lows but remains below pre-pandemic levels. They also pointed out a fair amount of uncertainty exists and that the “path of the economy will depend significantly on the course of the virus.” Nothing truly shocking. To alleviate some of this uncertainty, the Fed further committed to do everything in its power to support the recovery.

Seasonal: Neutral. August has been the worst DJIA, S&P 500 and NASDAQ month of the year since 1988. However, August’s track record in election years since 1950 (DJIA & S&P 500) or 1971 (NASDAQ) is much better. Average election year August performance ranges from 0.7% by DJIA to 3.3% for Russell 2000 (since 1979). This election year could be different since the pandemic has changed the date and structure of the conventions which have historically taken place in July.

Psychological: Near frothy. According to

Investor’s Intelligence Advisors Sentiment survey Bullish advisors are at 57.3%. Correction advisors stand at 25.2% while Bearish advisors stand at 17.5%. Overall sentiment is hovering right around levels seen near recent highs going back to late 2018. Sentiment has often lingered at elevated bullish levels for varying lengths of time before any meaningful retreat occurs. As long as the major indexes hold up, sentiment is likely to remain bullish.

|

August Outlook: Pandemic, GDP & Election Jeopardize Rally

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

July 30, 2020

|

|

|

|

Last week the market was shrugging off pandemic setbacks, bleak economic and corporate outlooks, geopolitical tensions, civic unrest and a contentious U.S. presidential election battle with NASDAQ hitting a new all-time high and S&P 500 at a new recovery high. In fact we were looking at a classic

“Hot July” pattern with DJIA up 4.6% for the month as of the close on July 22.

Gains of this magnitude for July, however, have frequently been followed by late-summer or autumn selloffs and better buying opportunities than end-of-July. In the past, full-month July gains in excess of 3.5% for DJIA have been followed historically by declines of -7.2% on average (-4.7% median decline) in the Dow with a low at some point in the last 5 months of the year.

Quite a bit has changed in the past eight days with the Dow giving back 2.6% putting July up only 1.9% month-to-date. Jobless claims have up-ticked the past two weeks from 1.31 million to 1.43 million. To put it perspective the difference of 126,000 claims is just under half the entire pre-pandemic level of 282,000 weekly jobless claims released on March 19. Plus, today the Advanced Estimate (first reading of three) of Q2 GDP came in at -32.9%. This was the worst reading ever – even worse than the Great Depression. Perhaps we can find some solace in the fact that it was less bad than the early June estimates of -40-50%.

We are not bearish long term. The super accommodative Fed will continue to print money as needed and we are likely to see more fiscal stimulus from central governments that will tack on more trillions to the current running tab of about $13 trillion. With Congress scheduled to go into recess August 10 through Labor Day there is concern the next stimulus package that is currently in negotiation will not be completed prior. However, it is in both parties best self-interest to get it done before the break. If it does not get done the market will likely respond more negatively.

There has been a bit of chatter out there about how Q3 of election years is the best performing quarter of the entire 4-year presidential stock market cycle. But that study uses data going all the way back to 1900 when the world was a much different place with much of the economy driven by agriculture. Our studies show that all the election year Q3 outperformance transpired before WWII with an average DJIA gain of 11.1% from 1901-1948. However, from 1949-June 2020 election year Q3 averaged DJIA gains of only 0.7%, ranked 11th of 16.

Also any improvement to August and September performance during election years is attributable to the buzz and excitement around the conventions. Nowadays campaigning goes on pretty much nonstop. This year’s candidates are already set save Biden’s running mate. The rally off the pandemic low has put the market back at lofty levels again. With most of the good news baked in, the market will be hard-pressed to add significant gains over the next 2-3 months without some major virus breakthroughs and a return to more normal economic activity.

Checking the accompanying updated chart of election years tracking 2020 S&P 500 performance versus all election years and incumbent party wins and losses – as well as the polls – suggests that President Trump’s reelection is not a forgone conclusion. In fact S&P 500 is tracking the incumbent loss trend more closely. But that of course remains to be seen. Market performance over the next three months is critical to President Trump’s reelection bid and you can be sure he is well aware and will do everything in his power to boost the market as all incumbents generally do.

![[AIN_0820_20200730_Election_Year_Pattern.jpg Chart]](/UploadedImage/AIN_0820_20200730_Election_Year_Pattern.jpg)

Depending on the state of the pandemic, the economy and the market over the next three months and how President Trump handles the COVID situation as well as civic unrest and diplomatic machinations the election could go still go either way. If things go south and the president is not reelected the yearend rally will likely come from lower levels and be more robust. The market is more prone to a pullback or correction over the next two months than piling on the monster rally. So stick to the drill remain cautious, stay on the defense, hold winners, sell losers and be ready for the summer doldrums and then a yearend rally.

Pulse of the Market

Spiking coronavirus cases across numerous locations in the U.S. has caused some areas of the country to slow and even reverse reopening plans. This has put a damper on expectations of a quick economic recovery and the pace of gains by DJIA. Early June DJIA highs (1) have not been eclipsed even with NASDAQ reaching new all-time highs and S&P 500 trading in positive year-to-date territory. As a result of DJIA essentially flat-to-sideways trading over the past five weeks, both the faster (2) and slower moving MACD indicators applied to DJIA are currently negative. This confirms DJIA’s loss of momentum and raises the odds of further weakness in the near-term.

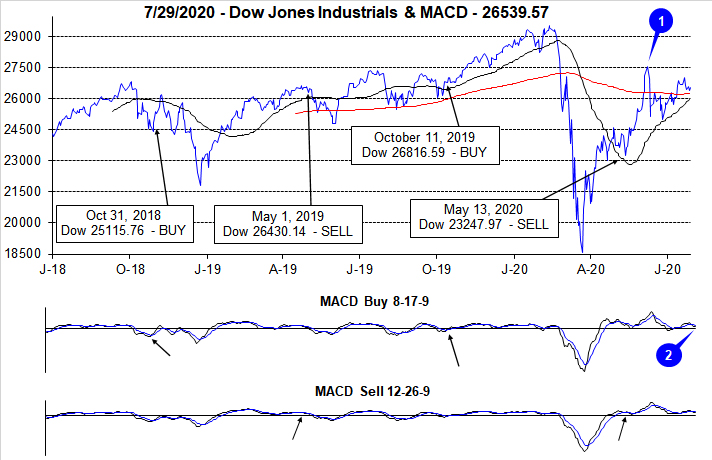

Since the end of March, the market’s trend has been resoundingly higher, but that trend has grown increasingly choppy with DJIA (3), S&P 500 (4) and NASDAQ (5) oscillating between weekly gains and losses. Weekly winning streaks have not exceeded three weeks in a row since early in the fourth quarter of 2019. However, DJIA’s streak of advancing Mondays (or first trading day of the week) is impressive at eleven in a row and thirteen of the last fourteen. It would seem traders and investors worse fears and concerns have not been materializing over weekends. The last time DJIA enjoyed a longer streak of positive first trading days of the week was at the end of 2009 that lasted through January 2010.

Market breadth measured by NYSE Weekly Advancers and NYSE Weekly Decliners (6) has gotten choppier over the last five weeks as tech stocks have charged higher leaving many other sectors behind. As the pandemic drags on, the market will likely increasingly favor the companies and sectors best equipped to navigate an uncertain outlook. As major indexes become increasingly tech-heavy, their advances may not accurately reflect the state of the economy and employment. Weekly market breadth is likely to remain mixed which is probably a better reflection of the current economic conditions.

Weekly New Highs (7) have been steadily trending higher, but the pace has been slow as broad market participation is still lacking. New all-time NASDAQ highs and the success of tech in general during the pandemic has produced the majority of new individual stock highs. The subdued number of New Weekly Lows is encouraging though as it suggests selling pressure in weaker areas of the market may have subsided.

Interest rates (8) are once again historically low and are likely to remain so for at least the foreseeable future. After peaking in early June, the 30-year Treasury rate is again trending lower toward its April low. Lower rates will aid consumers (to varying degrees) and the last cycle of ZIRP (zero interest rate policy) proved especially beneficial to the stock market. Odds are stocks will enjoy a similar outcome as well this time around.

|

August Almanac: Top Month in Election Years for Tech & Small Caps

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

July 23, 2020

|

|

|

|

Money flows from harvesting made August a great stock market month in the first half of the Twentieth Century. It was the best month from 1901 to 1951. In 1900, 37.5% of the population was farming. Now that less than 2% farm, August is amongst the worst months of the year. It is the worst DJIA, S&P 500, NASDAQ, Russell 1000 and Russell 2000 month over the last 32 years, 1988-2019 with average declines ranging from 0.1% by NASDAQ to 1.1% by DJIA.

However, in election years since 1950, Augusts’ rankings improve: #6 DJIA, #5 S&P 500, #1 NASDAQ (since 1971), #1 Russell 1000 and #1 Russell 2000 (since 1979). This year, the market’s performance in August will likely depend heavily on how July closes and whether or not the rate of covid-19 infection continues to accelerate which could force some areas to roll back reopenings.

![[Election Year August Mini Table]](/UploadedImage/AIN_0820_20200723_Election_Year_August_mini_table.jpg)

Contributing to this poor performance since 1987; the second shortest bear market in history (45 days) caused by turmoil in Russia, the Asian currency crisis and the Long-Term Capital Management hedge fund debacle ending August 31, 1998 with the DJIA shedding 6.4% that day. DJIA dropped a record 1344.22 points for the month, off 15.1%—which is the second worst monthly percentage DJIA loss since 1950. Saddam Hussein triggered a 10.0% slide in August 1990. The best DJIA gains occurred in 1982 (11.5%) and 1984 (9.8%) as bear markets ended. Sizeable losses in 2010, 2011, 2013 and 2015 of over 4% on DJIA have widened Augusts’ average decline.

The first nine trading days of the month have exhibited weakness while mid-month is better. Note the bullish cluster from August 17 through 19. The end of August tends to get whacked as traders evacuate Wall Street for the summer finale. The last five days have declined in 13 of the last 24 years with the S&P 500 up only seven times on the penultimate day in the past 24 years. In the last 24 years, the last five days of August have averaged losses of: Dow Jones Industrials, –0.7%; S&P 500, –0.2% and NASDAQ, –0.3%.

On Monday of expiration the Dow has been up 16 of the last 25 years with five up more than 1%, while on expiration Friday it has dropped in 7 of the last 10 years. Expiration week is down slightly more than half the time since 1990, but some of the losses have been steep (-2.6% in 1990, -2.3% in 1992, -4.2% in 1997, -4.0% in 2011, -2.2% in 2013 and -5.8% in 2015). The week after expiration is mildly stronger up 18 of the last 30.

| August Vital Stats (1950-2019) |

| |

DJI |

SP500 |

NASDAQ |

Russell

1K |

Russell 2K |

| Rank |

|

10 |

|

11 |

|

11 |

|

11 |

|

9 |

| #

Up |

|

39 |

|

38 |

|

27 |

|

25 |

|

23 |

| #

Down |

|

31 |

|

32 |

|

22 |

|

16 |

|

18 |

| Average

% |

|

-0.2 |

|

-0.1 |

|

0.2 |

|

0.2 |

|

0.2 |

| 4-Year Presidential Election Cycle Performance

by % |

| Post-Election |

|

-1.7 |

|

-1.4 |

|

-1.2 |

|

-1.4 |

|

-0.8 |

| Mid-Term |

|

-0.5 |

|

-0.2 |

|

-1.2 |

|

0.2 |

|

-1.3 |

| Pre-Election |

|

0.8 |

|

0.4 |

|

0.5 |

|

0.05 |

|

-0.5 |

| Election |

|

0.7 |

|

0.9 |

|

2.7 |

|

2.0 |

|

3.3 |

| Best & Worst August by % |

| Best |

1982 |

11.5 |

1982 |

11.6 |

2000 |

11.7 |

1982 |

11.3 |

1984 |

11.5 |

| Worst |

1998 |

-15.1 |

1998 |

-14.6 |

1998 |

-19.9 |

1998 |

-15.1 |

1998 |

-19.5 |

| August Weeks by % |

| Best |

8/20/82 |

10.3 |

8/20/82 |

8.8 |

8/3/84 |

7.4 |

8/20/82 |

8.5 |

8/3/84 |

7.0 |

| Worst |

8/23/74 |

-6.1 |

8/5/11 |

-7.2 |

8/28/98 |

-8.8 |

8/5/11 |

-7.7 |

8/5/11 |

-10.3 |

| August Days by % |

| Best |

8/17/82 |

4.9 |

8/17/82 |

4.8 |

8/9/11 |

5.3 |

8/9/11 |

5.0 |

8/9/11 |

6.9 |

| Worst |

8/31/98 |

-6.4 |

8/31/98 |

-6.8 |

8/31/98 |

-8.6 |

8/8/11 |

-6.9 |

8/8/11 |

-8.9 |

| First Trading Day of Expiration Week: 1990-2019 |

| #Up-#Down |

|

19-11 |

|

22-8 |

|

24-6 |

|

23-7 |

|

21-9 |

| Streak |

|

D2 |

|

D2 |

|

D2 |

|

D2 |

|

D2 |

| Avg

% |

|

0.25 |

|

0.31 |

|

0.43 |

|

0.28 |

|

0.38 |

| Options Expiration Day: 1990-2019 |

| #Up-#Down |

|

13-17 |

|

14-16 |

|

15-15 |

|

15-15 |

|

15-15 |

| Streak |

|

U2 |

|

U2 |

|

U2 |

|

U2 |

|

U2 |

| Avg

% |

|

-0.26 |

|

-0.17 |

|

-0.19 |

|

-0.16 |

|

0.09 |

| Options Expiration Week: 1990-2019 |

| #Up-#Down |

|

13-17 |

|

16-14 |

|

17-13 |

|

16-14 |

|

19-11 |

| Streak |

|

D1 |

|

D1 |

|

D3 |

|

D1 |

|

D1 |

| Avg

% |

|

-0.46 |

|

-0.16 |

|

0.16 |

|

-0.14 |

|

0.25 |

| Week After Options Expiration: 1990-2019 |

| #Up-#Down |

|

18-12 |

|

20-10 |

|

19-11 |

|

20-10 |

|

20-10 |

| Streak |

|

D1 |

|

D1 |

|

D1 |

|

D1 |

|

D1 |

| Avg

% |

|

0.33 |

|

0.37 |

|

0.60 |

|

0.36 |

|

0.10 |

| August 2020 Bullish Days: Data 1999-2019 |

| |

14,

19, 27 |

17-19,

27, 31 |

14,

17-19, 27 |

17-19,

27, 31 |

14, 18, 19, 25, 27 |

| |

|

|

|

|

|

| August 2020 Bearish Days: Data 1999-2019 |

| |

3,

12, 28 |

12,

20, 28 |

4,

12, 20 |

12 |

4, 5, 7, 12 |

| |

|

|

|

|

|

|

August 2020 Strategy Calendar

|

|

By:

Christopher Mistal

|

July 23, 2020

|

|

|

|

|

Mid-Month and Stock Portfolio Updates: Best of July Over & Defense Offers Second Opportunity

|

|

By:

Christopher Mistal

|

July 16, 2020

|

|

|

|

NASDAQ’s mid-year rally came to an end on Tuesday, July 14. During the rally’s 12-day stretch beginning on the third to last day of June through the ninth trading day in July, NASDAQ gained 4.7%. This is well above its average performance since 1985 but less than half of its best showing from 1999. At NASDAQ’s high close during the rally on July 10 it was up 6.0%. Historically around this time in July is when the market has begun to weaken as NASDAQ’s full-month average performance is just 0.9% since 1985.

![[NASDAQ Mid-Year Rally Table]](/UploadedImage/AIN_0820_20200715_NASDAQ_Midyear_rally_table.jpg)

In the following chart, July’s seasonal pattern over the last 21 years has been plotted with July 2020, plotted on the right axis for comparison through yesterday’s close. This July’s well above average performance so far called for a second, larger range in order to aid in the comparison. Over the last 21 years the market’s trend has been lower beginning right around mid-month through the close. DJIA, S&P 500, NASDAQ, Russell 1000 & 2000 have on average given back some or all of their first half of July gains.

![[July 21-Year Seasonal Pattern Chart]](/UploadedImage/AIN_0820_20200715_Seasonal_July.jpg)

Aside from historical, seasonal data; valuations, sentiment and a lack of guidance from companies this second quarter earnings season are a few possible catalysts that could lead to some near-term market weakness. According to estimates from our friend Sam Stovall of

CFRA, the S&P 500 is currently trading around 24.6 times its next 12-month earnings estimates, which is a premium of 49% to its 20-year average. Even if estimates are on the conservative side, there certainly appears to be a fair amount of optimism and hope built into current valuations leaving little room for mistake or error.

Bullish sentiment is also rather elevated now suggesting the majority that wants to own stocks likely already do. There may be massive piles of cash on the sidelines but that doesn’t mean its owners want to put it all into the market. The first notable data point at a worrisome (or at least at cautionary) level is

Investors Intelligence Advisors Sentiment survey showing a +40.0% spread between the number of bulls and bears. In their own words, “

Above +30% counts show more risk the higher they get, with defensive measures appropriate above 40%.” The second was last week’s CBOE Weekly Put/Call ratio at 0.44. At the start of June it reached 0.43 and in the following week S&P 500 dropped 4.8%.

Historically the worst two months of the year for the market, August and September, are just a few weeks away. Covid-19 is still spreading and many localities are slowing or reversing re-opening plans. Vaccine development is advancing, but that too could only lead to further uncertainty as the “stay-at-home” trade that has buoyed many tech stocks could also come to a rapid end. The worst is likely over but that does not rule out the possibility of a pullback, correction or at least a pause in the rally sometime between now and Election Day. The exceptional market performance in the second quarter is not likely to be repeated in the third quarter. NASDAQ’s Q2 gain of 30.6% this year was its second-best quarter ever. Its best quarter was Q4 of 1999, up 48.2%

Stock Portfolio Updates

Over the last five weeks through yesterday’s close, S&P 500 climbed a modest 1.1% and Russell 2000 edged 0.7% higher. During the same time period the portfolio slipped 2.2% excluding dividends and any trading fees. Overall performance lagged the broader indexes due to being rather concentrated in generally defensive positions (shaded in grey in the table below) – specifically a sizable number of utilities. After selling off throughout much of June, utilities have begun to show new life in July and the sector is enjoyed a nice move today.

Weakness was widespread across all three market-cap ranges in the portfolio. Large caps were worst, off 7.8% as numerous positions gave up previous gains. Duke Energy (DUK) is one example that was up 5.6% last update and has slipped to down 5.8% at yesterday’s close. Consolidated Edison (ED) was modestly lower last update and was stopped out on June 23 for a 14.9% loss. Energy stocks, BP plc (BP), Exxon Mobile (XOM) and Total S.A. (TOT) also lost ground this past month giving up approximately half of their respective gains or in the case of BP all over the last five weeks.

Bright spots in the large cap portfolio include Regeneron (REGN), ZTO Express (ZTO) and Abbott Labs (ABT). All three positions continued higher over the last five weeks. REGN is still the top performing position in the entire portfolio, up 105.1% since last October after selling half of the original position when it doubled on May 29. REGN and ABT are both in the fight against covid-19. ABT is contributing to the testing and detection of the virus while REGN has developed and is testing REGN-COV2, a novel anti-viral antibody cocktail. ZTO is an express delivery company in China where they just reported better than expected second quarter growth.

Our mid-cap stocks, two of which are utilities, also struggled over the last month. Due to a sizable cash balance the decline was limited to 2.2%. Algonquin Power (AQN) and One Gas Inc (OGS) are now below their respective original purchase prices. AQN and OGS can be considered for purchase near current levels up to their buy limits. JetBlue Airways (JBLU) also surrendered a sizable portion of last update’s gains but is still hanging onto a 35.1% advance since addition. JBLU is on Hold. This was a highly speculative trade idea based upon the notion that JBLU could and would survive a protracted and severe contraction in air travel.

Lastly are the small caps, three financial stocks and a homebuilder. KB Home (KBH) has retreated from its recent highs but has held up well as mortgage rates remain at or near record lows. KBH is on Hold. Real estate could face some weakness as federal support for unemployment benefits nears its currently scheduled end and as many mortgage and rent forbearance programs and protections wind down while millions are still unemployed. For nearly the same reasons, Atlantic Union Bankshares Corp (AUB), WSFS Financial Corp (WSFS) and South State Corp (SSB) are on Hold. Some mega banks have managed to best earnings expectations through the assistance of trading while others have not. It is likely regional banks will experience a similar mixed earnings season as each region has its own unique battle with covid-19.

Many of the defensive positions in the portfolio can again be considered on dips below their buy limits. Please see table below for specific buy limits, stop losses and current advice.

|

Top Performing Sectors of the “Worst Four Months”

|

|

By:

Christopher Mistal

|

July 09, 2020

|

|

|

|

This year has proven to be challenging for seasonality as the market was forced to endure a country-wide economic shutdown in response to the coronavirus pandemic. DJIA and S&P 500 “Best Six Months” were negative however, NASDAQ’s “Best Eight Months” were positive. After steep losses in February and March and the shortest bear market in history, major indexes rebounded sharply in April, May and June with technology stocks leading throughout. Tech strength has persisted into July and NASDAQ’s mid-year rally has been a success so far (up 5.3% as of today’s close) with three days remaining in the twelve-day span.

But, the growing weight of surging coronavirus cases across numerous U.S. states appears to be increasingly burdening tech leadership and its momentum. Even though NASDAQ has broken out to new all-time highs, DJIA and S&P 500 have been struggling since early June. Once NASDAQ’s mid-year rally comes to a close, it too could succumb to negative headlines and generally mixed economic data. At which point the broader market could weaken further as well.

In the following table, the performance of S&P 500 and NASDAQ during the “Worst Four Months” July to October is compared to fourteen select sector indices or sub-indices, gold and the 30-year Treasury bond. Nine of the fourteen indices chosen are S&P Sector indices. Gold and 30-year bond are continuously-linked, non-adjusted front-month futures contracts. With the exception of two indices, 1990-2019, a full 30 years of data was selected. This selection represents a reasonably balanced number of bull and bear years for each and a long enough timeframe to be statistically significant while representing current trends. In an effort to make an apples-to-apples comparison, dividends are not included in this study.

![[Various Sector Indices & 30-Year Treasury Bond versus S&P 500 during Worst Six Months May-October Since 1990 table]](/UploadedImage/AIN_0820_20200709_Worst_Four_Table.jpg)

Using the S&P 500 as the baseline by which all others were compared, six sector indices or sub-indices, 30-year Treasury bond futures, gold futures and NASDAQ outperformed during the “Worst Four Months” while eight others underperformed based upon “AVG %” return. At the top of the list are Biotech and Information Technology with average gains of 4.59% and 3.35% during the “Worst Months.” However, before jumping into Biotech positions, only 25 years of data was available and, in those years, Biotech was up just 56.0% of the time from July through October. Some years, like 2014, gains were massive while in down years losses were frequently nearly as large. The race to produce a coronavirus vaccine is likely to give the sector a boost this year, but in the end, there will likely be only one company that accomplishes this first. That company’s shareholders are likely to be rewarded while runners-up may not be as fortunate.

![[Biotech mini-table]](/UploadedImage/AIN_0820_20200709_Biotech_table.jpg)

In second-place, Information Technology with 30 years of data and a 70.0% success rate is probably a safer choice than Biotech. Its 3.35% AVG % performance comes by way of two fewer losses in five additional years of data. Four sizable double-digit losses since 1990 are indicative of the sectors potential volatility and the only meaningful blemish on an otherwise fairly solid track record.

Other “Worst Four” top performers consisted mostly of the usual suspects when defensive sectors are considered. Consumer Staples, 30-year Treasury bonds and Utilities all bested the S&P 500. Gold futures, Healthcare and Financials also bested the S&P 500, but % Up was not as favorable. Although not the best sector by AVG %, Utilities advancing 70.0% of the time with a worst single-year loss of 7.88% is the closest thing to a sure bet for success during the “Worst Four Months.”

![[Utilities mini-table]](/UploadedImage/AIN_0820_20200709_utilities_table.jpg)

At the other end of the performance spectrum we have the sectors to consider shorting or to avoid altogether. The Natural Gas sector, represented by NYSE ARCA Natural Gas index, was the worst over the past 30 years, shedding an average 2.27% during the “Worst Four.” Consumer Discretionary, Telecommunication Services, Materials and PHLX Gold/Silver also recorded average losses. Based solely upon the percentage of time up, Telecommunication Services is the most consistent loser of the “Worst Four” advancing just 46.7% of the time.

![[NYSE ARCA Natural Gas index mini-table]](/UploadedImage/AIN_0820_20200709_nat-gas_table.jpg)

Interesting to note is the fact that only three sectors/indices fail to advance in July and October, on average. July is the first month of the second half of the year and tech’s mid-year rally gives it a bullish tailwind. August and September tend to be downright ugly on average. It is this window of poor performance that has given October a lift in the past 30 years. Only Biotech, gold futures, 30-year bonds, utilities and gold & silver stocks manage to post gains in both August and September.

Based upon “% Up” during the “Worst Four Months,” Consumer Staples and Utilities look like the best place to be. Both sectors have beaten the S&P 500 while being relatively less volatile. If maximum return is your goal, and volatility can be tolerated, Biotech and Information Technology are the way to go. The disconnect in performance between gold futures and gold & silver stocks suggests that the physical metals may be the best place to be during times of economic uncertainty and/or broad equity weakness.

|

ETF Trades & Portfolio Updates: Transports, Industrials & Precious Metals

|

|

By:

Christopher Mistal

|

July 02, 2020

|

|

|

|

July and the second half of the year have started off consistent with historical trends and patterns. The first trading day was mostly positive with S&P 500 and NASDAQ recording gains while today, the last day before the long Independence Day Holiday weekend the market is also enjoying solid gains. A better than expected June jobs report and positive news regarding covid-19 vaccine are among the key factors supporting the market.

However, July has historically been a month of transition with gains early and weakness in the second half. Thus far the market and economic data appears to be shaking off the spike in daily covid-19 cases along with the delays and even backtracking in reopening plans in certain areas of the country. Perhaps the market is correct, and it really doesn’t matter or perhaps the spike just hasn’t reached a level where the market would take notice.

Nonetheless, the market has enjoyed a spectacular rebound and valuations and bullish sentiment are elevated. Combined with covid-19 and election uncertainties, it would appear that conditions are conducive to trigger a pause or even a pullback by the market sometime during the “Worst Months.”

July Sector Seasonalities

Three new sector seasonalities begin in the month of July. First up is a bearish seasonality in Transports which typically begins in the middle of July and lasts until the middle of October. This seasonality is based upon the Dow Jones Transportation index (DJT). Over the last 5-, 10- and 15-year time periods DJT has declined 2.7%, 1.0% and 3.5% on average during this weak timeframe. Industrials also exhibit similar weakness as the transports sector over nearly the exact same time period.

iShares Transportation (IYT) is a good choice to establish a short position in to take advantage of seasonal weakness in the transport sector. IYT has nearly $600 million in assets, has traded an average of over 250,000 shares per day over the past 20 trading days and has a reasonable 0.42% expense ratio. IYT’s top five holdings include: Norfolk Southern, Union Pacific, FedEx, Kansas City Southern and JB Hunt.

Unlike NASDAQ and tech stocks, IYT continues to struggle to reclaim pre-covid levels. More recently, IYT’s breakout above its 200-day moving average failed to hold and it retreated back to its lower 50-day moving average. Currently, Stochastic, relative strength and MACD indicators are all neutral, but improving as IYT has enjoyed a few days of gains. IYT could be shorted near resistance around $176.81 or a breakdown below $154.46. If shorted, set an initial stop loss at $180.00, this level is just above the intra-day high in early June’s failed breakout.

SPDR Industrials (XLI) will be our choice to establish a short position in to trade seasonal weakness in the industrial sector. XLI has over $9 billion in assets and frequently has over 10 million shares changing hands daily. Its expense ratio of 0.13% is very reasonable. Top five holdings include: Union Pacific, Honeywell, Boeing, Raytheon Tech and 3M.

XLI’s chart and technical indicators do not differ much from the chart of IYT. XLI has not recovered to pre-covid levels, also had a failed breakout in early June and currently is trading between its higher 200-day moving average and its lower 50-day moving average. XLI could be shorted near resistance around $74.94 or a breakdown below $66.35. If shorted, set an initial stop loss at $77.00, this level is just above the intra-day high in early June’s failed breakout.

July’s final seasonality is from gold & silver mining stocks. This seasonality is based upon strength in the Philadelphia Gold & Silver index that typically begins in late July and lasts until late December. Over the last five years this trade has not been that successful however, over the last fifteen years the trade has averaged 4.6%. A three-pronged approach to this trade will be taken. In addition to a long position in VanEck Vectors Gold Miners (GDX) positions in SPDR Gold (GLD) and iShares Silver (SLV) are also suggested.

![[VanEck Vectors Gold Miners (GDX) Daily Bar Chart]](/UploadedImage/AIN_0820_20200702_GDX.jpg)

GDX is currently trading near multi-year highs due to strength in physical gold. In response to covid-19, interest rates have been cut to zero again and massive government spending has/is taking place. Lower rates and ballooning deficits and debt have generally a negative for the U.S. dollar and have the potential to boost inflation. Both are generally viewed as a positive for gold and the stocks that mine it. GDX could be considered near current levels up to a buy limit of $37.05. If purchased an initial stop loss at $32.25 is suggested. Take profits if GDX trades above $42.46.

SPDR Gold (GLD) is a current holding in the Sector Rotation ETF Portfolio. Additional purchase and/or new purchases could be considered on dips below a buy limit of $166.50. If purchased, set a stop loss at $155.00.

SLV could be considered near current levels with a buy limit of $16.90. If purchased, set a stop loss at $14.45.

Sector Rotation ETF Portfolio Updates

With the exception of the four trade ideas presented above, the balance of the Sector Rotation Portfolio is on Hold. Defensive positions in XLP, XLU and IBB were established in early May and will likely be held until sometime on or after October 1, 2020; the earliest date that our Seasonal MACD Buy Signal can trigger.

Please see updated portfolio table below for the most recent advice, buy limits and stop losses.

Tactical Seasonal Switching Strategy Updates

In accordance with our

June 11 NASDAQ Seasonal MACD Sell signal corresponding positions in

iShares Russell 2000 (IWM) and

Invesco QQQ (QQQ) were closed out of the portfolio using their respective average prices on June 12. IWM was a bust, down 8.1%. QQQ was once again the bright spot of the portfolio, up 23.5% from October 14, 2019 through June 12 of this year. Although challenging to hold positions during the dramatic March covid-induced market selloff, it certainly worked well with QQQ.

Now that NASDAQ’s Best Eight Months have come to an end, the portfolio is entirely defensive holding only positions in bond ETFs AGG and BND. Cash is also a position that could be held for the rest of the “Worst Months.” AGG and BND can still be considered on dips below their respective buy limits.