|

Market at a Glance - 7/28/2022

|

|

By:

Christopher Mistal

|

July 28, 2022

|

|

|

|

7/28/2022: Dow 32529.63 | S&P 4072.43 | NASDAQ 12162.59 | Russell 2K 1873.03 | NYSE 15198.81 | Value Line Arith 8731.08

Seasonal: Bearish. August is the worst DJIA, S&P 500, Russell 1000, and Russell 2000 since 1988 and second worst month for NASDAQ. Midterm-year August’s have been mixed with significant losses occurring in 1974, 1990 and 1998. August 2022 is also in the “Weak Spot” of the four-year-cycle.

Fundamental: Recession. The traditional definition of a recession is two consecutive quarters of GDP decline. Q1 was negative and the first estimate of Q2 was also negative. Treasury yields are also partially inverted. Real personal consumption expenditures also decreased in May (June to be released on July 29). Corporate earnings have also been tepid with numerous companies missing expectations. Housing is cooling, supply chain pressures persist, and consumer confidence remains depressed. Employment data has remained firm but could be the final shoe to drop if other data continues to come in weak.

Technical: Nearing Resistance? DJIA, S&P 500 and NASDAQ have all enjoyed fair rallies off of their respective June lows. At those lows, they were all oversold and due for a bounce. All three have reclaimed their 50-day moving average but remain well below their 200-day moving averages. Also standing in their way are the early June highs around: DJIA 33250, S&P 500 4180 and NASDAQ 12320. A decisive move above these levels could put respective 200-day moving averages in play. Failure could lead to an eventual retest of the June lows.

Monetary: 2.25 – 2.50%. Energy and other commodity prices have eased lately, but headline CPI and PPI have yet to confirm with lower readings that could suggest a change in trend. Nonetheless, the Fed did raise rates by 0.75% this month and boldly signaled that they will likely slow the pace of hikes as soon as their next meeting in September. As a result of a less hawkish Fed, the market has largely shrugged off this month’s rate increase thus far. QT (quantitative tightening), currently around $47.5 billion per month is scheduled to double to $95 billion on September 1.

Psychological: Improving. According to

Investor’s Intelligence Advisors Sentiment survey Bullish advisors stand at 38.9%. Correction advisors are at 27.8% while Bearish advisors numbered 33.3% as of their July 27 release. Bears peaked at 44.1% in mid-June and have been trending lower as the market has climbed higher. Current levels of bulls, bears and correction advisors are essentially neutral. Where the market goes next is likely to dictate the overall direction in sentiment.

|

August Outlook: Hot Julys Often Bring Late-Summer/Autumn Buys

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

July 28, 2022

|

|

|

|

Inflation, war, recession fears, aggressive Fed rate hikes, lingering supply chain issues, layoffs, earnings misses, and lingering pandemic issues drove the market into official bear market territory last month. Driven by hopes of a soft landing, a resilient labor market, pockets of positive economic and corporate results, and some rather seriously oversold conditions in big name tech and growth stocks the market has rallied smartly off the June lows.

As of today’s close, DJIA is up 8.8% from the June lows, S&P is up 11.1% and NASDAQ is up 14.2%. The 2022 summer rally has worked the bulls into a frenzy like a matador with his red muleta, pushing the Dow toward a top-ten July, up 5.7% at todays close with only one trading day left in the month, qualifying this as a “Hot July Market.”

Gains of this magnitude for July, however, have frequently been followed by late-summer or autumn selloffs and better buying opportunities than now. In the past, full-month July gains in excess of 3.5% for DJIA have been followed historically by declines of 7.2% on average in the Dow with a low at some point in the last 5 months of the year.

2022 Tracing Justin Mamis’ Sentiment Cycle

Here is a little sneak peek into the 2023 Stock Trader’s Almanac as we send it off to press that is also remarkably apropos now. The 2022 edition features “Marty Zweig’s Investing Rules” on page 80. For the 2023 edition on this page, we are featuring “Bob Farrell’s Market Rules to Remember & Justin Mamis’ Sentiment Cycle.”

90-year-old Bob Farrell has retired to Florida, but he still imparts his forecasts and outlook to investors and traders from time to time. We will touch on his “Rules to Remember” at another time.

Justin Mamis passed away in 2019, but his books and wisdom are still relied upon regularly to this day. Mamis was a highly regarded market analyst and technician who authored three must-have books on the stock market: When to Sell (1977), How to Buy (1982), and The Nature of Risk (1991) and two must read newsletters.

Just before we presented at the CMT Association’s 2022 Annual Symposium veteran technical analyst Helene Meisler shared Mamis’ Sentiment Cycle (pictured below) along with her analysis of where in the cycle the market was at the time at the end of April 2022—in that brief pause between disbelief and panic (green circle).

Comparing the current chart of the S&P 500 below we’ve highlighted in yellow that area of disbelief Ms. Meisler pointed out in April. Our assessment is that the June low correlates quite well with the “Panic” point on Mamis’ chart and we are now hitting the first level of “Anxiety.” This dovetails with our bearish seasonal/cycle outlook as we are entering the worst two months of the year and are smack dab in the

“Weak Spot” of the 4-Year Cycle from Q2 to Q3 of the midterm election year.

Our view on the economy is less than sanguine as we just logged the second quarter in a row of negative GDP with rampant inflation only just beginning to take its toll on Main Street. Cheerleading aside, we have not definitively averted recession. It may yet prove to be mild, but the effects of the Fed’s aggressive rate increase have yet to really hit home, and another hike is likely in September.

While the summer rally off the June lows has been impressive, the market is now running into technical resistance around the early June highs. Sentiment has rebounded with the market but is by no means bullish. Market internals have been choppy with New Lows still outpacing New Highs and without any material rise in the Advance/Decline Line.

We believe the bear market is nearing the end, but this July bounce is a classic bear market rally before the final push lower. Remember, July is the best month of Q3. But “Hot July Markets” like this year are often followed by lower prices and better buying opportunities later in the year.

August and September are the worst months of the year, and we are facing some rather stiff headwinds with respect to the war in Ukraine, inflation, rate hikes, growth and the midterm elections. But the

“Sweet Spot” of the 4-Year Cycle from Q4 midterm year through Q2 pre-election year is only two months away. Cash is still king. Stick to the playbooks and look for a retest of the lows in the August-October period, which we expect to deliver the next fat pitch for the “Sweet Spot” and the return of the bull.

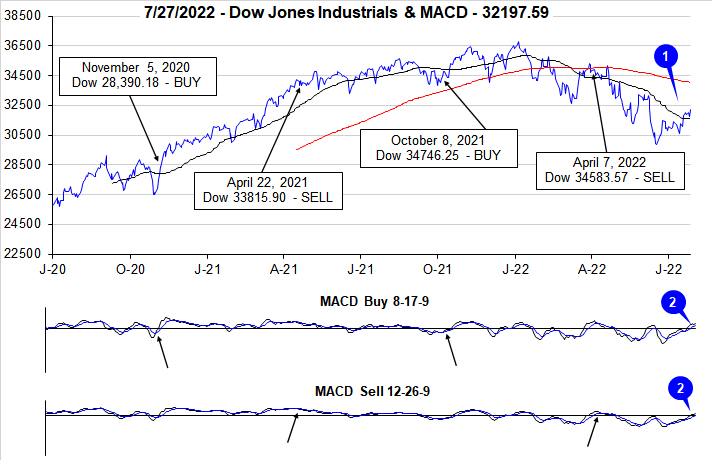

Pulse of the Market

After an abysmal first half of the year, DJIA has managed to extend its rally off the June lows into July (1). As of the close today, July 28, DJIA was up 5.7% in July which is strong enough to claim the 10th best July performance by percent going back to 1950. Based upon points gained, it would be DJIA’s best July ever. July’s gains have pushed DJIA back above its 50-day moving average, but still 4.4% below its 200-day moving average. The rebound has also persisted long enough to push both the faster and slower moving MACD indicators back above the zero line (2). As MACD climbs higher above the zero-line, overbought indications tend to strengthen.

Should this week’s gains hold, DJIA (3), S&P 500 (4) and NASDAQ (5) will log their first back-to-back weekly gains since late March. It would also be the first time since last October when all three indexes were positive in at least four of six weeks. With the historically worst two months of the year, August and September, just ahead, the current streak of gains could quickly come to an end.

NYSE Weekly Advancers and Weekly Decliners (6) have been consistent with the market’s overall choppy moves higher off of the June lows. During down weeks the number of Weekly Decliners expanded and during positive weeks Weekly Advancers held the advantage. A significant spike in the ratio of Weekly Advancers to Weekly Decliners is still absent from the table. Without a spike similar to past major bottoms, the odds of a retest of the June lows remain elevated.

Despite the recent rebound, New Weekly New Highs (7) have remained disappointingly low at just 54 during the week ending July 22. Even during the first two weeks of June when the market was in near free-fall there were a greater number of new highs. Somewhat encouraging, New Weekly Lows have retreated to their second lowest reading of the year. There were fewer at the start of June. A trend of increasing new Highs and shrinking new Lows would be a positive sign.

Even before Q2 U.S. GDP was released the spread between the 90-day Treasury and the 30-year Treasury had been narrowing (8). The 90-day rate was climbing in anticipation of the Fed raising rates again while the 30-year was declining on growing recession fears. Since the start of the year the 90-day rate has gone from essentially zero to approximately 2.5% while the 30-year rate has climbed about one full point. The percentage of the yield curve that is inverted continues to expand which has historically been another recession indication.

|

August Almanac: Positive Midterm Record Marred by Sizable Losses

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

July 21, 2022

|

|

|

|

Money flows from harvesting made August a great stock market month in the first half of the Twentieth Century. It was the best DJIA month from 1901 to 1951. In 1900, 37.5% of the population was farming. Now that less than 2% farm, August is amongst the worst months of the year. It is the worst DJIA, S&P 500, Russell 1000, and Russell 2000 month over the last 34 years, 1988-2021 with average declines ranging from –0.3% by Russell 2000 to –0.8% by DJIA. NASDAQ August ranks second worst over the same period with an average gain of 0.3%.

Contributing to this poor performance since 1988; the second shortest bear market in history (45 days) caused by turmoil in Russia, the Asian currency crisis and the Long-Term Capital Management hedge fund debacle ending August 31, 1998, with the DJIA shedding 6.4% that day. DJIA dropped 1344.22 points for the month, off 15.1%—which is the second worst monthly percentage DJIA loss since 1950. Saddam Hussein triggered a 10.0% slide in August 1990. The best DJIA gains occurred in 1982 (11.5%) and 1984 (9.8%) as bear markets ended. Sizeable losses in 2010, 2011, 2013 and 2015 of over 4% on DJIA have widened Augusts’ average decline.

![[Midterm August Table]](/UploadedImage/AIN_0822_20220721_August_2022_midterm_Vital_Stats_mini_table.jpg)

In midterm years since 1950, Augusts’ rankings improve slightly: #8 DJIA and S&P 500, #10 NASDAQ (since 1974), #5 Russell 1000 and #10 Russell 2000 (since 1982). Average losses range from –0.2% for S&P 500 to –1.3% for Russell 2000. Russell 1000 has advanced 0.2% on average in midterm Augusts. All five indexes have winning track records, but losses have frequently been substantially larger than gains. DJIA and NASDAQ suffered double-digit losses in 1974, 1990 and 1998.

Historically, the first eight or nine trading days of the month have exhibited weakness while mid-month is better. Note the bullish cluster from August 15 through 17. This strength is visible above on trading days 11, 12 and 13. The end of August tends to be softer when traders evacuate Wall Street for a summer finale. The last five days were bearish from 1996 to 2013 but have been positive in seven of the last eight years. However, S&P 500 has been up only nine times on the penultimate day in the past 26 years.

On Monday of monthly options expiration DJIA has been up 17 of the last 27 years with four up more than 1%. Monthly expiration Friday has been mixed recently. DJIA has been up the last four years straight after declining in seven of the previous eight. Expiration week is down 19 times in 32 years since 1990, with some sizable losses; –2.6% in 1990, –2.3% in 1992, –4.2% in 1997, –4.0% in 2011, –2.2% in 2013 and –5.8% in 2015. The week after expiration is stronger up 20 of the last 32.

|

August 2022 Strategy Calendar

|

|

By:

Christopher Mistal

|

July 21, 2022

|

|

|

|

|

Stock Portfolio Updates: Volatility Swells Cash Holdings

|

|

By:

Christopher Mistal

|

July 14, 2022

|

|

|

|

This time may feel different, much different than recent economic retreats and corresponding bear markets. But each bear market and recession has had its own set of circumstances and triggers. Covid economic shutdowns in 2020, subprime lending in 2008 to 2009, dot-com euphoria ending and 9/11 in 2000-2001 and on and on. However when the bear ended, and economic growth resumed there was always one common outcome: a new bull market for stocks. It seems quite reasonable to expect a similar outcome this time around.

Because the causes of bear markets and recessions have varied and neither usually begins nor ends on a set schedule a precise date for the current bear’s end remains elusive. We can, as we have been opining in recent months, speculate that the bear is likely to come to an end sometime later this year, most likely in late Q3 or early Q4 based upon historical data.

In the following table of S&P 500 Bull, Bear, 10% Corrections and Recessions since 1948 we have added the current bear market. This table differs from the data found on page 134 of the 2022 Stock Trader’s Almanac. In this table we have used the commonly cited in various media 20% decline as the definition of a bear market. As of July 16 close, S&P 500 was down 20.7% in 191 calendar days from its closing high on January 3. Compared to the average bear market loss of 33.2%, the current bear has actually been rather typical and mild thus far. Considering the compression in cycles that has been observed recently it would also seem reasonable to anticipate the bear finishes in less than the average 376 calendar days recorded by the previous 12 bears.

![[S&P 500 Bull, Bear, 10% Corrections and Recessions since 1948]](/UploadedImage/AIN_0822_20220714_SP500_Bull-bear-correx-recessions_table.jpg)

We still believe that the current bear market will come to an end later this year, most likely around midterm election time. We believe yesterday’s hotter than expected 9.1% CPI reading actually improves the odds of a final bottom later this year as it is likely to force the Fed to accelerate its rate hike cycle even further. The sooner the Fed gets to a point where inflation is slowing, the sooner they can pause or perhaps even stop hiking rates. Historically, the market has enjoyed its best performance when the

Fed was inactive or making minor adjustments to rates. Until that time arrives, cash may be the least risky asset to hold in your portfolio.

Stock Portfolio Updates

Over the last five weeks since last update through yesterday’s close, S&P 500 declined 7.6% while Russell 2000 fell 8.7%. Over the same time period the entire stock portfolio slipped 0.2% lower, excluding dividends and any fees. A sizable cash position, that currently stands at approximately 84% of the total portfolio, aided in avoiding the vast majority of the market’s decline. As a reminder, we are not targeting a specific percentage of cash. The current balance is the result of heeding stop losses when reached and by being patient for a more favorable risk/reward setup in the market.

Broad market weakness in early June had the greatest impact in the Large-cap portfolio. Even traditionally defensive positions were not spared. In total seven stocks were stopped out of the portfolio. Constellation Energy (CEP) was the first to get stopped out on June 14 with a 44.9% gain. CEP was spun off from Exelon Corp (EXC) earlier this year and was not a new trade idea. EXC was also stopped out in June. Due to its spin off of CEP, EXC was closed for a loss of 11.9% however, the overall trade was positive due to CEP’s gain.

Also stopped out in June were Ameren Corp (AEE), DTE Energy (DTE), Duke Energy (DUK) and DT Midstream (DTM). Sadly many of these stops were classic whipsaws that occurred right around the lows in June. As recession concerns have grown and Treasury bond yields eased, many have rebounded. Once again it would appear that the market’s volatility can sweep into any sector.

Brookfield Infrastructure (BIP) was stopped out just after it split 3:2. Softening energy prices and broad market weakness in June appear to be the key reasons for BIP’s decline. Rather than rush back into these positions, we will elect to remain in cash and await a better opportunity.

Despite numerous upgrades in recent weeks, Warner Brothers Discovery (WBD) continues to decline. Like CEP, WBD was a spin off and our patience has worn thin. Sell WBD. For tracking purposes it will be closed out of the portfolio using its average price on July 15.

On a positive note, MGP Ingredients (MGPI), in the Small-cap portfolio bucked the market’s trend and climbed 8.1% higher over the last five weeks. At today’s close, MGPI was less than $3 from its 52-week reached on July 5. MGPI is on Hold.

All positions are on Hold. Please see the table below for updated stop losses and current advice for positions not covered above.

|

ETF Trades: Shorting Setups in Transports & Industrials

|

|

By:

Christopher Mistal

|

July 07, 2022

|

|

|

|

On the heels of one of the roughest first-half starts in decades; the market has found some footing during the seasonally bullish start to the second half of the year here in the beginning of July. NASDAQ’s midyear rally appears to be fully underway lending strength to S&P 500 and DJIA. Even during historically meager midterm years, the first half of July has generated respectable gains.

However, as you can see in the updated S&P 500 seasonal pattern chart, through its July 6 close below, gains have historically faded later in the month or sometime in August. Despite a few days of strength recently, we still expect this bear market to put in a typical midterm-election-year bottom sometime later this year. The bottom is most likely to be in the August-October timeframe just ahead of the midterm elections and possibly around the time when the Fed begins to slow or even pause its rate hike cycle.

July Sector Seasonalities

Three new sector seasonalities begin in the month of July. First up is a bearish seasonality in Transports which typically begins in the middle of July and lasts until the middle of October. This seasonality is based upon the Dow Jones Transportation index (DJT). Over the last 10- and 15-year time periods DJT has declined 2.1% and 2.6% on average during this weak timeframe. Industrials also exhibit similar weakness as the transports sector over nearly the same period.

iShares Transportation (IYT) is a top choice to establish a short position in to take advantage of seasonal weakness in the transport sector. IYT has over $800 million in assets, has traded an average of over 250,000 shares per day over the past 30 days and has a reasonable 0.41% expense ratio. IYT’s top five holdings include: United Parcel Service, Union Pacific, CSX, FedEx and Old Dominion Freight.

![[iShares Transportation (IYT) Daily Bar Chart]](/UploadedImage/AIN_0822_20220707_IYT.jpg)

Similar to the broader market, IYT has been trending lower since the start of the year with only the briefest hints of strength along the way. Currently IYT is below its 50- and 200-day moving averages and its 50-day moving average has fallen below its 200-day (a death cross). Currently, stochastic, relative strength and MACD indicators have turned mildly positive, but it could be a false indication similar to what transpired in late May through early June. IYT could be shorted near resistance around $226.25 or a breakdown below $199. If shorted, set an initial stop loss at $236.00, this level is around IYT’s early June closing high.

SPDR Industrials (XLI) will be our choice to establish a short position in to trade seasonal weakness in the industrial sector. XLI has over $12 billion in assets and frequently has over 10 million shares changing hands daily. Its expense ratio of 0.10% is very reasonable. Top five holdings include: Raytheon Tech, United Parcel Services, Union Pacific, Honeywell and Lockheed Martin.

XLI’s chart and technical indicators do not differ much from the chart of IYT. XLI even experienced the same late May to early June rally before falling abruptly. XLI could be shorted near resistance just above $92.10 or on a breakdown below $84.00. If shorted, set an initial stop loss at $97.75, this level is just above the closing high in early June’s failed breakout.

July’s final seasonality is for gold & silver mining stocks. This seasonality is based upon strength in the Philadelphia Gold & Silver index that typically begins in late July and lasts until late December. The recent break in gold and silver along with continued strength in the U.S. dollar suggests further weakness is likely before the ultimate bottom is reached. Gold’s failure to make a meaningful run higher while inflation is at multi-decade highs is also concerning. For now, we are going to pass on this trade as the current situation does not appear favorable.

Sector Rotation ETF Portfolio Updates

In the time since last update all positions in the portfolio except SPDR S&P Biotech (XBI) were stopped out. Even historically defensive positions that have traditionally weathered the “Worst Six Months” were not spared by the broad declines in June. SDPR Healthcare (XLV) was the first to get stopped out on June 10. SPDR Consumer Staples (XLP) followed on June 13 and SPDR Utilities (XLU) on June 16. Excluding dividends and trading costs, only XLV produced a modest gain.

Previously mentioned U.S. dollar strength appears to be a key contributor to gold’s recent weakness with SPDR Gold (GLD) being stopped out at the start of this week. GLD had been a longer-term holding so even after its recent retreat it still produced a 19.9% gain since addition.

June’s broad market weakness was an excellent reminder that at times, cash can be the safest place to shelter. As has been the case throughout the market’s long history, there will likely be a much better opportunity to put cash back to work. Until that time arrives, interest rates are on the rise while inflation (year-over-year change) appears to be topping. Cash may not provide much of a real return, but it surely does appear less risky than other choices at this time.

Tactical Seasonal Switching ETF Portfolio Updates

On June 13, NASDAQ’s Seasonal MACD Sell signal was triggered. Per the email Alert sent that day Invesco QQQ (QQQ) and iShares Russell 2000 (IWM) were closed out of the portfolio using their respective average prices during the June 14 trading session. NASDAQ just recorded its first down “Best Eight Months” with MACD timing since 2008 and its first double-digit decline since 2001. These are disappointing results for the strategy, but we do not believe it is broken or no longer working. We anticipate there will be a better opportunity later this year with history suggesting a solid, positive return during the next “Best Months” period which also aligns perfectly with the “Sweet Spot” of the four-year cycle.

Defensive bond positions, TLT, AGG and BND, have recovered modestly as recession fears have supported demand, but remain in the red excluding dividends and trading costs. All three positions are considered partial positions as originally suggested in April. Should more recession signals flash, bond funds could easily continue to rally. Any price upside could be limited as the Fed is still committed to raising rates. Once again, cash does appear to be the least risky position to remain in during the remainder of the “Worst Months” this year.