|

2019 Forecast: Santa on Notice from Dueling Grinches – Low Nears – Bear Lurks

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 20, 2018

|

|

|

|

Fed Chairman Powell and President Trump have been competing for who can freak the market out most. Our contention for months has been that the Fed is the biggest risk to the market and economy and that surely seems to have come home to roost the past few months and this week.

Last month in our “Market at a Glance” we said that, “

After nearly a decade at zero, a brief pause to evaluate the impact of recent hikes does not seem unreasonable.” In addition to the continuing rate hikes is the impact of the Fed’s quantitative tightening program of reducing its balance sheet, which is equivalent to another ¼ or ½ point on the Fed Funds rate. We have not been the only ones saying this and perhaps Stanley Druckenmiller said it best in his

Wall Street Journal piece last weekend.

And in the face of this market selloff Chairman Powell refused to relent and pause to reflect. Perhaps he’s playing hardball with President Trump and wants to prove the Fed’s independence or perhaps he is just determined to raise rates as much as he can while the “labor market has continued to strengthen and” “economic activity has been rising at a strong rate,” in the Fed’s own words from the 12/19/18 FOMC Statement.

Either way his comments at Wednesday’s news conference that he expects to raise rates 2 more times in 2019, while the Fed’s growth forecasts for 2019 and beyond are for slower growth were not what the market wanted to here. Quarter point now and a pause to reflect would have been music to Wall Street’s ears.

President Trump’s own games of hardball with the Democrats over the “wall” and the funding bill to keep the federal government open and the Chinese over fair trade continue to spook the market. The market’s performance thus far in Q4 has been the exact opposite of historical averages. Higher interest rates, trade disputes and Brexit all appear to be weighing on the market. Tougher corporate earnings comparisons and slowing earnings growth are also hindering the market.

When the U.S.-China trade negotiations take a step in a positive direction and the Fed has toned down some of its more hawkish rhetoric the market will be free to rally. It would take one impressive rally to put Q4 back in the black, but there is still time for a more modest yearend rally that could return DJIA and S&P 500 to a positive full-year performance or at least bring Santa Claus to Wall Street.

Technically the market is broken. As we warned on our blog Monday we were

flirting with disaster and now that all three major U.S. market indices have violated the early 2018 lows more selling is probable as there is little support below them. Next levels of support are found way back at the August 2017 lows around Dow 21700, S&P 2425 and NASDAQ 6200.

Additionally, volatility has not spiked that high and the selling has been rather orderly with little of the panic that is present at market bottoms.

So as we wind down this year of the return to volatility and more historically normal market action (2017 was an anomaly) our outlook is tempered, at least for the next several weeks and early 2019. If our Santa Claus Rally can materialize that would be the first constructive sign, if not, we would expect more volatility.

Midterm Correction Sets Stage

The tax cut legislation held off the usual midterm year correction until much later in the year, pushing the potential low toward yearend and into 2019. But this bodes well for pre-election year 2019. If the market had kept chugging along to new highs, gains in 2019 would have been harder to come by.

Now that we have a sizeable correction and likely a bit more downside in store, 2019 is setting up better than it was at the beginning of October. If the market can find support soon or early in 2019, the Fed comes to its senses and the folks in D.C. can cut some deals more normal pre-election year gains can be expected.

The third year of the 4-year presidential election cycle is still the strongest and now with the market hitting new 52-week lows the stage is set. For perspective have a look at the average 1-year seasonal patterns for the Dow, S&P 500 and NASDAQ in the chart below.

Four Horseman of the Economy

Lead horseman DJIA along with the rest of the market has definitely come up lame since early October, but the longer term uptrend remains intact. However, as mentioned above we have a technical breakdown on the charts that brings the August 2017 lows into play. Next levels after that are the spring 2017 lows then yearend 2016 levels.

Consumer confidence is still strong, but further market declines could easily take the wind out of the consumer’s sails. Corporate investments are still in full force with billions of dollars of spending planned, but if the economy-driving consumer gets cold feet growth rates are likely to slow.

The Fed’s statutory mandate from Congress to “promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates,” appears to be in check. The Unemployment Rate continues to remain super low at 3.7%. Economic activity is strong and prices remain stable.

Our inflation horseman as measured by our 6-month exponential moving average calculation on the CPI and PPI is has been rising steadily into that healthy level with the CPI just over 2% at 2.43% up from 1.98% last year at this time. PPI is now at 4.31% up nearly a full percentage point from last year’s 3.49% level, but down a notch from last month’s 4.59% level.

2018 Forecast Recap

The three-case forecast we presented last year was:

- Worst Case – 5% chance. Full blown midterm bear market caused by North Korea actually setting off a nuke, no positive impact from tax reform, or some other doomsday scenario.

- Base Case – 47.5% chance. Above average midterm year gains in the range of 8-15%, a mild worst six correction or pullback.

- Best Case – 47.5% chance. Everything pans out, tax reform juices corporate earnings, bonuses & paychecks grow, economy grows. DJIA 29,000, S&P 3,300, NASDAQ 9,800

The small chance we gave the doomsday scenario did not pan out. While stocks have sold off a chunk here, this is not a full-blown bear market at this point. Our best case scenario also did not pan out. But our base case was not that far off. Instead of getting a correction during the bulk of the worst six months and the 8-15% gains by yearend, we got 8-15% gains by early October and an October-December correction.

Pulse of the Market

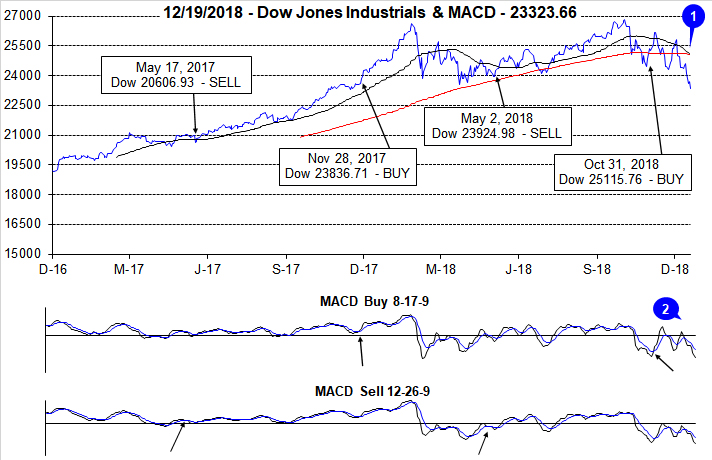

Thus far there has been nothing magical about Q4 2018. At today’s close, DJIA is down 13.6% for the quarter. This is DJIA’s worst Q4 since 2008 when it declined 19.1% and its eighth worst Q4 going back to 1901. DJIA has sunk below its 50- and 200-day moving averages and a death cross has formed on its chart (1). A death cross occurs when the 50-day moving averages crosses through the 200-day moving average. Since 1982, the majority of DJIA death crosses were not accompanied by any major subsequent decline. Faster and slower moving MACD indicators applied to DJIA are currently negative and below the “zero” line (2). This is indicative of a market that is or is approaching oversold conditions.

Mid-month December has historically been a choppy time for DJIA and that has been especially true this year with only a single day of strength on the first trading day and frequent daily declines following. On Monday, December 17, DJIA completed its thirteenth Down Friday/Down Monday (DF/DM) of 2018 (3). The longer-term track record for DF/DM occurrences is ominous, with declines frequently taking place sometime in the next 90 calendar days. However, they have also occurred at some significant inflection points near interim bottoms. With DJIA, S&P 500 (4) and NASDAQ (5) all declining in four of the past five weeks a rebound is a possibility.

Market breath measured by NYSE Weekly Advancers and NYSE Weekly Decliners was last positive during the final week of November and turned decidedly negative over the last two weeks (6). However, the ratio of decliners to advancers has yet to reach the extreme levels of 6-10 decliners per one advancer that transpired near recent lows in February 2018 or February 2016.

Weekly New Highs and New Lows reacted as one would expect during a steady retreat. New Lows (7) have ballooned to their highest level since February 2016 while New Highs remain subdued. A sustained trend of expanding highs and shrinking lows would be an encouraging sign that the selloff could have reached a climax.

90-day Treasury rate continued to climb (8) reaching 2.38% last week ahead of the anticipated Fed interest rate hike while the 30-year Treasury rate continues to decline on slowing global growth prospects. Market-based interest rates appear to be telling the Fed to take a breather on further hikes as the Treasury yield curve continues to flatten while 2-year yields are already exceeding 5-year yields (inversion).

Click for larger graphic…

2019 Forecast

There is an increasing probability that we are in a bear market right now in the U.S. And if the U.S. market continues to behave as it has for the last few months, we could be down 20% on the Dow and S&P 500 soon or in early 2019. The NASDAQ was down 20% intraday from its highs today and the Russell 2000 is already down 23.8% as of today’s close from its 2018 high

Taking into account the risks of heightened volatility, increasingly bearish sentiment, a more tepid fundamental outlook, a persistently hawkish Fed, an embattled Federal government as well as the bullish history of pre-election year markets and historical seasonal patterns we have once again laid out three scenarios for next year:

- Worst Case – Prolonged bear market caused by hawkish Fed, dysfunctional Federal Government, slow growth and weak corporate fundamentals brings us all the way back to November 2016 pre-Trump election levels or lower. Repeat of pre-election year 2015 with the bear lasting throughout 2019 into 2020.

- Base Case – Something gives. Mild bear market bottoms soon or in early 2019 as Fed tones down rhetoric and holds off raising rates, Trump and the Dems work out a few deals and we have modest pre-election year gains in the 5-10% range.

- Best Case – Everything resolves quickly. Fed becomes accommodative. Trade deals are worked out expeditiously. Trump tacks towards the center and works with congress and does not get “Muellered.” Typical pre-election year gains of 10-15% for Dow and S&P 500 and 20-30% for NASDAQ

We will be keeping you fully abreast of all readings from out three January Trifecta Indicators: Santa Claus Rally, First Five Days and the full-month January Barometer and will make adjustments on the close of January 2019.

Happy Holidays & Happy New Year, we wish you all a healthy and prosperous 2019!

|

Market at a Glance - 12/20/2018

|

|

By:

Christopher Mistal

|

December 20, 2018

|

|

|

|

12/19/2018: Dow 23323.66 | S&P 2506.96 | NASDAQ 6636.83 | Russell 2K 1349.23 | NYSE 11371.84 | Value Line Arith 5401.44

Psychological: Neutral. According to

Investor’s Intelligence Advisors Sentiment survey bulls are at 39.3%. Correction advisors are at 39.3% and Bearish advisors are 21.4%. At current levels, sentiment is essentially flat. Bearish advisors have ticked modestly higher but are still just a few percentage points above their level when the market was at all-time highs a few months ago.

Fundamental: Firm-ish. Near-term the outlook remains reasonably solid. Unemployment is low, the economy is still creating jobs each month, corporate earnings, although slowing, are forecast to continue growing and Atlanta Fed’s GDPNow model is forecasting 2.9% growth for Q4. Beyond the near-term the outlook becomes murky. The housing market and the auto industry are feeling the bite of higher interest rates already. Foreign markets are struggling, more tariffs could be coming, and the Fed has forecast a slowdown in growth in 2019 and 2020. One may want to consider that the Fed does not have the greatest track record forecasting growth and it has admitted such.

Technical: Broken down. DJIA, S&P 500, NASDAQ and Russell 2000 have all closed below support at their respective lows from earlier this year. Death crosses appear on the charts of all four. Russell 2000 is in the worst shape down over 20% since its high to officially be in a bear market. Dow Theory is also signaling the possibility of a new bear market, but utilities have not broken down yet. Stochastic, relative strength and MACD indicators applied to the major indexes are near or at oversold levels.

Monetary: 2.25-2.50%. The Fed did take a somewhat less hawkish tone at its recent meeting, but it apparently was not dovish enough. After raising interest rates for the fourth time this year, the Fed suggested fewer hikes will occur next year which was a mild win for the bulls. However, the Fed failed to mention any possibility of slowing the rate at which is reducing its balance sheet. In the end only the slightest of shifts away from its previously hawkish tightening monetary policy. Even a moderately hawkish Fed is still the greatest risk to the economy and the market. The continued flattening of the Treasury yield curve is the market signaling to the Fed it is time to pause and even consider easing up a bit.

Seasonal: Bullish. January is the third month of the Best Six/Eight, but it is the last of the Best-Three-Consecutive-month span. January is the top month for NASDAQ (since 1971) averaging 2.6%, but it has slipped to sixth for DJIA and S&P 500 since 1950. Pre-election-year Januarys have been exceptional (DJIA +3.7%, S&P 500 +3.9% NASDAQ +6.6%). The Santa Claus Rally ends on January 3rd and the First Five Days early-warning system ends on the 8th. Both indicators provide an early indication of what to expect in 2019. We will wait until the official results of the January Barometer on January 31 before tweaking our 2019 Annual Forecast. Email Alerts will be sent after the close on these dates.

|

January Almanac: Top Month for Stocks in Pre-Election Years

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 27, 2018

|

|

|

|

January has quite a legendary reputation on Wall Street as an influx of cash from yearend bonuses and annual allocations typically propels stocks higher. January ranks #1 for NASDAQ (since 1971), but sixth on the S&P 500 and DJIA since 1950. It is the end of the best three-month span and holds a full docket of indicators and seasonalities.

DJIA and S&P rankings did slip from 2000 to 2016 as both indices suffered losses in ten of those nineteen Januarys with three in a row, 2008, 2009 and 2010. January 2009 has the dubious honor of being the worst January on record for DJIA (-8.8%) and S&P 500 (-8.6%) since 1901 and 1931 respectively. Despite late-month weakness in 2018, S&P 500 still gained 5.6% and DJIA jumped 5.8%.

In pre-election years, Januarys have been downright stellar ranking #1 for S&P 500, NASDAQ, Russell 1000 and Russell 2000 and #2 for DJIA. Average gains range from 2.9% by Russell 1000 to a whopping 6.6% for NASDAQ.

On pages 108 and 110 of the Stock Trader’s Almanac 2019 we illustrate that the January Effect, where small caps begin to outperform large caps, actually starts in mid-December. Thus far, signs of this have been absent when comparing iShares Russell 2000 (IWM) to SPDR S&P 500 (SPY) as broad weakness prior to the last two days has depressed most shares. The majority of small-cap outperformance is normally done by mid-February, but strength can last until mid-May when indices typically reach a seasonal high.

The first indicator to register a reading in January is the Santa Claus Rally. The seven-trading day period began on the open on December 24 and ends with the close of trading on January 3. Normally, the S&P 500 posts an average gain of 1.3%. The failure of stocks to rally during this time tends to precede bear markets or times when stocks could be purchased at lower prices later in the year.

On January 8, our First Five Days “Early Warning” System will be in. In pre-presidential election years this indicator has a solid record. In the last 17 pre-presidential election years 12 full years followed the direction of the First Five Days. 1955, 1991, 2007, 2011 and 2015 did not. The full-month January Barometer has an even better pre-presidential-election-year record as 15 of the last 17 full years have followed January’s direction.

Our flagship indicator, the January Barometer created by Yale Hirsch in 1972, simply states that as the S&P goes in January so goes the year. It came into effect in 1934 after the Twentieth Amendment moved the date that new Congresses convene to the first week of January and Presidential inaugurations to January 20.

The long-term record has been stupendous, an 86.8% accuracy rate, with only nine major errors in 68 years. Major errors occurred in the secular bear market years of 1966, 1968, 1982, 2001, 2003, 2009, 2010 and 2014 and again in 2016 as a mini bear came to an end. The market’s position on January 31 will give us a good read on the year to come. When all three of these indicators are in agreement it has been prudent to heed their call.

| January (1950-2018) |

| |

DJI |

SP500 |

NASDAQ |

Russell 1K |

Russell 2K |

| Rank |

|

6 |

|

6 |

|

1 |

|

5 |

|

5 |

| #

Up |

|

44 |

|

42 |

|

31 |

|

25 |

|

22 |

| #

Down |

|

25 |

|

27 |

|

17 |

|

15 |

|

18 |

| Average

% |

|

0.9 |

|

1.0 |

|

2.7 |

|

1.0 |

|

1.4 |

| 4-Year Presidential Election Cycle Performance

by % |

| Post-Election |

|

0.6 |

|

0.8 |

|

2.3 |

|

1.6 |

|

1.8 |

| Mid-Term |

|

-0.5 |

|

-0.7 |

|

0.01 |

|

-0.6 |

|

-0.6 |

| Pre-Election |

|

3.7 |

|

3.9 |

|

6.6 |

|

2.9 |

|

3.2 |

| Election |

|

-0.01 |

|

0.2 |

|

1.7 |

|

0.1 |

|

1.2 |

| Best & Worst January by % |

| Best |

1976 |

14.4 |

1987 |

13.2 |

1975 |

16.6 |

1987 |

12.7 |

1985 |

13.1 |

| Worst |

2009 |

-8.8 |

2009 |

-8.6 |

2008 |

-9.9 |

2009 |

-8.3 |

2009 |

-11.2 |

| January Weeks by % |

| Best |

1/9/76 |

6.1 |

1/2/09 |

6.8 |

1/12/01 |

9.1 |

1/2/2009 |

6.8 |

1/9/87 |

7.0 |

| Worst |

1/8/16 |

-6.2 |

1/8/16 |

-6.0 |

1/28/00 |

-8.2 |

1/8/16 |

-6.0 |

1/8/16 |

-7.9 |

| January Days by % |

| Best |

1/17/91 |

4.6 |

1/3/01 |

5.0 |

1/3/01 |

14.2 |

1/3/01 |

5.3 |

1/21/09 |

5.3 |

| Worst |

1/8/88 |

-6.9 |

1/8/88 |

-6.8 |

1/2/01 |

-7.2 |

1/8/88 |

-6.1 |

1/20/09 |

-7.0 |

| First Trading Day of Expiration Week: 1990-2018 |

| #Up-#Down |

|

17-12 |

|

13-16 |

|

12-17 |

|

11-18 |

|

11-18 |

| Streak |

|

D2 |

|

D2 |

|

D6 |

|

D6 |

|

D6 |

| Avg

% |

|

-0.02 |

|

-0.06 |

|

-0.05 |

|

-0.1 |

|

-0.2 |

| Options Expiration Day: 1990-2018 |

| #Up-#Down |

|

18-11 |

|

17-12 |

|

16-13 |

|

17-12 |

|

17-12 |

| Streak |

|

U8 |

|

U4 |

|

U4 |

|

U4 |

|

U4 |

| Avg

% |

|

0.02 |

|

0.03 |

|

-0.04 |

|

0.03 |

|

0.1 |

| Options Expiration Week: 1990-2018 |

| #Up-#Down |

|

15-14 |

|

11-18 |

|

16-13 |

|

11-18 |

|

15-14 |

| Streak |

|

U1 |

|

U1 |

|

U1 |

|

U1 |

|

U1 |

| Avg

% |

|

-0.2 |

|

-0.2 |

|

0.02 |

|

-0.2 |

|

-0.1 |

| Week After Options Expiration: 1990-2018 |

| #Up-#Down |

|

15-14 |

|

18-11 |

|

16-13 |

|

18-11 |

|

21-8 |

| Streak |

|

U4 |

|

U4 |

|

U4 |

|

U4 |

|

U4 |

| Avg

% |

|

-0.2 |

|

-0.1 |

|

0.1 |

|

-0.04 |

|

0.2 |

| January 2019 Bullish Days: Data 1998-2018 |

| |

2,

3, 25, 28 |

10,

16, 25 |

2,

8-10, 16, 28 |

9,

10, 25 |

9, 10, 16, 28, 31 |

| |

|

|

|

|

|

| January 2019 Bearish Days: Data 1998-2018 |

| |

8,

17, 18, 22 |

None |

15,

18, 22 |

None |

18, 30 |

| |

|

|

|

|

|

|

January 2019 Strategy Calendar

|

|

By:

Christopher Mistal

|

December 27, 2018

|

|

|

|

|

2018 Free Lunch Stocks Served: 23 New Lows Make the Cut

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 22, 2018

|

|

|

|

Publication Note: On Thursday, December 27th we will deliver to you our last regularly scheduled Alert of 2018 covering the January 2019 Almanac and Strategy Calendar. Our next email will be on January 3, 2019. However, if market conditions warrant an interim update, one will be sent. Happy Holidays and Happy New Year!

Our “Free Lunch” strategy is purely a short-term strategy reserved for the nimblest traders. Traders and investors tend to get rid of their losers near yearend for tax loss purposes, often driving these stocks down to bargain levels. Our research has shown that NYSE stocks trading at a new 52-week low on or about December 15 will usually outperform the market by February 15 in the following year. We have found that the most opportune time to compile our list is on the Friday of December triple witching.

This strategy takes advantage of several year-end patterns and indicators. First, the stocks selected are usually technically, deeply oversold and poised for a bounce, dead cat or otherwise. Second, all of the stocks are of the small- and mid-cap variety that will benefit from the January Effect which is the tendency for small-caps to outperform large-caps from mid-December through February. Lastly, the strategy spans the usually bullish Santa Claus Rally and the First Five Days of January.

To be included in this list, the stock must have traded at a new 52-week low on Friday, December 21, 2018. To remain on this year’s list, the stock had to still be trading at $1.00 or higher as several online trading platforms place additional restrictions on a trade when shares are below $1.00. Furthermore, the stock must have traded at least 100,000 shares on average over the past 20 days and have a market cap of at least $100 million, but not greater than $10 billion. Then, any stock that was not down 70% or more from its 52-week high to the 52-week low reached on Friday was also eliminated. Additionally, since the number of stocks making new 52-week lows on December 21, 2018 was so large we screened for stocks that had trading volume on Friday that was 3x the average daily over the past 20 days on NYSE, AMEX and NASDAQ. Finally, preferred stocks, funds, splits, special high dividends and new issues were eliminated. No stocks from the American Stock Exchange made the cut.

Our suggested guidelines for trading these Free Lunch stocks is to initiate a position at a price no greater or less than 2% of Friday’s closing price and to implement an 8% trailing stop on a closing basis from your execution prices. If the stock closes below 8% of the execution price or a subsequent high watermark, then the stock would be closed out of the portfolio. If any of these stocks trades in a window between -2% to +2% of Friday’s closing price it will be tracked in the Almanac Investor Stock Portfolios using the trade’s execution price with an 8% trailing stop on closing basis.

If you buy these stocks, please note the following:

1. Consider selling them as soon as you have a significant gain and utilize stop losses.

2. The stocks all behave differently and there is no automatic trigger point to sell at.

3. Standard trading rules from the Almanac Investor Stock & ETF Portfolios do not apply for these stocks.

4. We think you should be out of all of these stocks between the middle of January and the middle of February.

5. Also, be careful not to chase these stocks if they have already run away.

DISCLOSURE NOTE: Officers of the Hirsch Organization do not currently own any of the shares mentioned. However, we may participate in the Free Lunch Strategy.

|

Seasonal Sector Trades: Copper Setting Up For a Rally

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

December 13, 2018

|

|

|

|

Copper has a tendency to make a major seasonal bottom in December and then a tendency to post major seasonal peaks in April or May. This pattern could be due to the buildup of inventories by miners and manufacturers as the construction season begins in late-winter to early-spring. Auto makers are also preparing for the new car model year that often begins in mid- to late-summer. Traders can look to go long a May futures contract on or about December 17 and hold until about February 24. In this trade’s 46-year history, it has worked 30 times for a success rate of 65.2%. After four straight years of declines from 2012 to 2015, this trade has been successful the last two years.

Cumulative profit, based upon a single futures contract excluding commissions and fees, is a respectable $74,913. More than one-fourth of that profit came in 2007, as the cyclical boom in the commodity market magnified that year’s seasonal price move. However, this trade has produced other big gains per single contract, such as a $14,475 gain in 2011, and even back in 1973, it registered another substantial $9,475 gain. These numbers show this trade can produce big wins and big losses if not properly managed. A basic trailing stop loss could have mitigated many of the losses.

![[Long Copper (May) Trade History Table]](/UploadedImage/AIN_0119_20181213_HG_History_Table.jpg)

In the following chart, the front-month copper futures weekly price moves and seasonal pattern are plotted. Typical seasonal strength in copper is highlighted in yellow. Last year’s seasonal period was actually tepid. The move off of copper’s December low to its late-December high was greater than the gain over the entire holding period. Copper also spiked in mid-June before succumbing to typical seasonal weakness. Copper has been essentially range bound since late-September. A reduction in Chinese tariffs on imported autos (along with the potential easing of other tariffs) could be a catalyst for copper to begin its seasonal rally soon. Any improvement in the U.S. housing market will also likely support higher prices for copper.

![[Copper (HG) Bars and Seasonal Pattern Chart (Weekly Data December 2017 – December 13, 2018)]](/UploadedImage/AIN_0119_20181213_HG_Seasonal.jpg)

One option to take advantage of copper’s seasonal move is iPath Bloomberg Copper TR Sub-Index ETN (JJCTF). As a reminder, ETNs differ from ETFs. An ETN is debt whose current value is based upon an index return. In the case of JJCTF, it is linked to the Bloomberg Copper Total Return Index, which represents the potential return of an unleveraged investment in copper futures. JJCTF trading volume is quite thin, trading just a few thousand shares per day on average. Volume does pick up when copper begins to move, but we will pass on JJCTR.

A second option that provides exposure to the copper futures market without having to have a futures trading account, is United States Copper (CPER). This ETF tracks the daily performance of the SummerHaven Dynamic Copper Index Total Return. CPER’s daily volume is also on the light side, but at least it frequently trades in excess of 10,000 shares per day. Stochastic, relative strength and MACD technical indicators applied to CPER are all negative now. A position in CPER can be considered on dips below $17.00. If purchased an initial stop loss of $16.25 is suggested. This trade will be tracked in the Almanac Investor Sector Rotation ETF Portfolio.

![[United States Copper (CPER) Daily Bar Chart]](/UploadedImage/AIN_0119_20181213_CPER.jpg)

Another way to gain exposure to copper and its seasonally strong period is through the companies that mine and produce copper. Global X Copper Miners ETF (COPX) holds shares of some of the largest copper miners and producers from across the globe. Its top five holdings as of December12, 2018 are: Kaz Mineral, Vedanta, KGHM Polska, Zijin Mining Group and OZ Minerals. COPX could be considered on dips below $19.00. If purchased, an initial stop loss of $20.47 is suggested. This trade will also be tracked in the Sector Rotation section of the ETF Portfolio.

![[Global X Copper Miners ETF (COPX) Daily Bar Chart]](/UploadedImage/AIN_0119_20181213_COPX.jpg)

Yet another option to trade seasonal strength in copper is through the use of highly correlated stocks. Two common names that fit nicely are Freeport-McMoRan (FCX) and Southern Copper (SCCO). Both are highly correlated with the price of copper and both are well below their respective highs traded earlier this year. Both pay a dividend and have attractive valuations relative to the broader market. SCCO could be considered on dips below $32.00. If purchased an initial stop loss at $27.84. FCX can be considered on dips below $10.95. If purchased a stop loss of $9.53 is suggested. These two stock trades will be tracked in the Almanac Investor Stock Portfolio.

|

Stock Portfolio Update: New Longs Struggle While Defense Continues to Shine

|

|

By:

Christopher Mistal

|

December 13, 2018

|

|

|

|

Over the last four weeks since last update, S&P 500 declined 1.9% through yesterday’s close. Russell 2000 was 3.1% lower over the same time period. Overall, the entire Stock Portfolio slipped 0.2% excluding any dividends or trading fees. Mid-caps were hit the hardest, down 2.7%. Small-caps were second worst off 1.4%. Our Large-cap portfolio, with the largest concentration of defensive stocks, gained 6.7%. Compared to the S&P 500, the overall portfolio outperformed due to gains made by defensive positions added in June.

Recent market volatility has proven to be a challenge for our November Stock Basket. Of the original 20 stocks, eight have been stopped out. Lumentum Holdings (LITE) was the first to go in early November. Since then, Tillys (TLYS), Granite Construction (GVA), Kemet Corp (KEM), Range Resources (RRC), Unit Corp (UNT), HollyFrontier (HFC) and TJX Cos Inc (TJX) also closed below their respective stop losses and have been closed out of the portfolio. RRC and HFC were likely pressured lower by the decline in crude oil price. TLYS actually reported better than expected earnings, but revenues were apparently less than analyst estimates which was all the reason needed for shares to drop 29% in just four trading sessions.

Of the remaining positions from November’s basket, large-cap positions have been holding up the best. CDW Corp (CDW) had a modest 1% gain at yesterday’s close but surrendered it today. BRO, EPD, EXPE, EXPD and PAA are down single-digit since being added to the portfolio. Mid- and small-cap positions that still remain are slightly weaker with most off double-digits. Should the market find its footing in mid-December, like it has in many past Decembers, then these losses could quickly be recovered.

June’s basket of Defensive Stocks continues to perform well. Gains in the Large-cap section of the portfolio came nearly entirely from defensive positions and were sufficient to offset the mild declines recorded by other positions. Of the original 21 stocks selected thirteen are still held and all are positive with an average gain of 19.9%.Including the stopped and closed positions, the basket’s average performance is 10.2% compared to a loss of 4.7% by S&P 500 over the same time period excluding any dividends or fees.

The best performing defensive position is still McCormick & Company (MKC), up 46.2% as of yesterday’s close. Second best is Church & Dwight (CHD) up 36.4% at yesterday’s close. Mondelez (MDLZ) and Southern Co (SO) are the only two defensive stocks that are not yet up double-digits.

Per last update’s advice, Altria Group (MO), Sysco (SYY) and Conagra (CAG) were all closed out of the portfolio using their respective average prices on November 16. All three are lower now than then so those sales could be considered timely.

All positions in the portfolio are on Hold. Should market volatility subside around mid-December we will consider unwinding remaining defensive positions and entering new long positions. Please see portfolio table below for Current Advice and Stop Losses.

|

ETF Trades: Oil Returns to Favor in December

|

|

By:

Christopher Mistal

|

December 06, 2018

|

|

|

|

Tomorrow morning the Bureau of Labor Statistics will release its Employment Situation report for November. Depending upon your preferred source, the consensus estimate is for a gain of approximately 200,000 net new nonfarm jobs. This would be even stronger than the 179,000 that ADP reported earlier today. Historically, the market has responded favorably to the jobs report released in December. S&P 500, NASDAQ, Russell 1000 and Russell 2000 have all advanced fourteen times in the last seventeen years. DJIA’s record has one more loss. Average gains range from a low of 0.46% by DJIA to 0.81% by Russell 2000.

![[Market Performance on December Jobs Day Table]](/UploadedImage/AIN_0119_20181206_Dec_PR_Day.jpg)

Tomorrow’s jobs report will be the last one the Fed will see before they meet later this month. Currently, there is right around a 75% chance the Fed will hike rates again at it December meeting according to CME Group’s FedWatch Tool. A weaker jobs report could lessen the probability of another hike, but it does appear the Fed will likely hike regardless in December and instead shift focus onto 2019. Unemployment is low, and inflation appears to be under control, but economic growth is not exactly running away. The flattening (slightly inverted) Treasury yield curve also seems to be signaling that it may be time for the Fed to pause, but probably not until next year.

New December Seasonality

Oil companies typically come into favor in mid-December and remain so until late April or early May in the following year (yellow box in chart below). This trade has averaged 10.8%, 5.6%, and 7.8% gains over the last 15-, 10-, and 5-year periods. This seasonality is not based upon the commodity itself; rather it is based upon NYSE ARCA Oil & Gas index (XOI). This price-weighted index is composed of major companies that explore for and produce oil and gas.

Crude oil and XOI have been tumbling since early October on increasing U.S. supplies and the Saudi’s producing at record levels causing a broad oversupply. Trade and global growth concerns are also weighing on demand. The condition of excess supply is widely known and will likely be corrected before crude oil falls much below $50 per barrel.

SPDR Energy (XLE) is the top pick to trade this seasonality. A new position in XLE could be established on pullbacks with a buy limit of $63.50. Employ a stop loss of $57.15. Take profits at the auto sell of $77.39. Exxon Mobil is the top holding in XLE at 24.77%. The remaining top five holdings of XLE are Chevron, ConocoPhillips, EOG Resources and Occidental Petroleum.

Sector Rotation Portfolio Updates

Recent market weakness has dampened the performance of most positions held in the Sector Rotation Portfolio. Average performance has been cut in half since last update with technology-related funds performing poorest. SPDR Technology (XLK) was stopped out on the close on November 20. XLK has rebounded modestly and is currently trading right around the level it was stopped out at. XLK’s top two holdings are Microsoft and Apple. Microsoft has been holding up well while Apple’s selloff appears to be overdone. A new position in XLK can be considered on dips up to a buy limit of $66.05.

SPDR Healthcare (XLV), SPDR Consumer Staples (XLP) and Vanguard REIT (VNQ) are the top performing positions in the portfolio. Their defensive nature has contributed to their resilience. XLV, XLP and VNQ can all still be considered on dips or at current levels. These positions could provide some cushion against any broad market volatility in the near-term.

All other positions in the portfolio not previously mentioned can also be considered near current levels or on dips. Please see table below for updated buy limits, stop losses and current advice for each position.

Tactical Seasonal Switching Strategy Portfolio Update

Although current market volatility seems unprecedented, it is not. Midterm years historically have seen volatility in October, November and sometimes into early December. The Fed is starting to take a more dovish tone. The Federal government may shutdown, but again, this has occurred before and the market powered through. Trade issues with China could end quicker than they started. We will stick to the time-tested strategy while paying close attention to incoming economic data and technical indicators.

Current weakness can be used to establish new positions or add to existing positions in DIA, IWM, QQQ, SPY.