|

Market at a Glance - 3/31/2022

|

|

By:

Christopher Mistal

|

March 31, 2022

|

|

|

|

3/31/2022: Dow 34678.35 | S&P 4530.41 | NASDAQ 114220.52 | Russell 2K 2070.12 | NYSE 16670.91 | Value Line Arith 9583.40

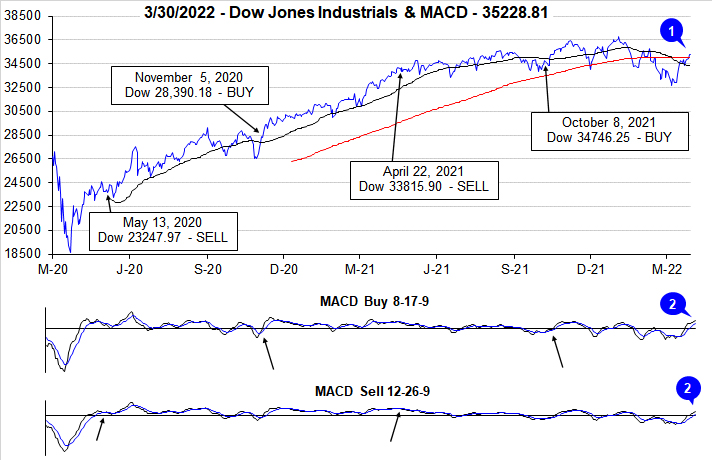

Seasonal: Bullish. April is the #1 DJIA and S&P 500 month of the year since 1950. Third best month for NASDAQ (since 1971) and Russell 2000 (since1979). Average gain in all years ranges from 1.7% by S&P 500 to 2.0% by DJIA. DJIA has been up 16 straight Aprils, 2006 – 2021. Midterm year performance has been softer with average performance sliding to –0.1% by NASDAQ to 0.7% from DJIA and Russell 2000. April is also the last month of the “Best Six Months” for DJIA and S&P 500. Our Seasonal MACD Sell Signal can occur anytime on or after April 1.

Fundamental: Murky. Russia’s Ukraine invasion persists. Commodity and energy prices remain lofty. Inflation is running at multi-decade highs with little evidence pressures will abate anytime soon. U.S. growth is slowing, and the Fed is tightening monetary policy. However, employment data and corporate earnings forecasts remain respectable. Federal infrastructure spending is also likely to give the economy a boost. If conflict in Ukraine comes to a resolution sooner rather than later, the outlook would likely greatly improve quickly.

Technical: Rebounding. After spending the majority of the first quarter in retreat, DJIA, S&P 500 and NASDAQ appear to have found support in March. All three index charts have a death cross formation (50-day has fallen below 200-day moving average) on them, but the intra-day lows of February 24 held. The brisk rally has brought DJIA and S&P 500 back above their respective 50- and 200-day moving averages, but NASDAQ has not reclaimed its 200-day moving average yet. Given the magnitude and duration of the rally a pause here at the end of Q1 is not out of the question. If NASDAQ can reclaim and hold its 200-day moving average, then the rally could have further room to run.

Monetary: 0.25 – 0.50%. Some might say “it’s about time.” That is what the Fed finally said too at its March meeting when it announced the first rate increase of what is likely to be a series of increases. The higher and the longer inflation runs above the Fed’s target the more credibility they likely lose. Russia in Ukraine and ongoing supply chain disruptions are likely to challenge the Fed’s ability to rein in inflation. Recent comments from Fed members have also indicated a willingness to move at a quicker 0.5% hike interval if needed. In the end, it is likely the Fed only gets to 2 to 2.5% before pausing, likely sometime next year. Considering historical interest rate levels, this would still be rather accommodative monetary policy.

Psychological: Neutral. According to

Investor’s Intelligence Advisors Sentiment survey Bullish advisors have climbed to 37.7%. Correction advisors stood at 28.2% while Bearish advisors numbered 34.1% as of their March 29 release. Historically, extreme bearish sentiment has frequently been an excellent buying opportunity. This doesn’t appear to be the situation any longer as bullish sentiment has modestly improved, and the market has swiftly rallied off the March lows.

|

April Outlook: War, Inflation & Fed Loom Over End Best Six Month

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

March 31, 2022

|

|

|

|

As we enter the last month of the Best Six Months, the market logged its first down quarter in two years since the beginning of the pandemic. Going back to 1930 when our S&P 500 data begins Q1 was positive 55 years and negative 37 times over the 92-year span. Overall, years that advanced in Q1 were up 46 of the 55 years or 83.6% of the time with an average gain of 13.2% for S&P 500. Years when Q1 was down, were positive only 16 of the 37 years or 43.2% of the time for an average loss of -0.1%.

What jumped out at us were the midterm years that had losing first quarters. In the table we compiled here, the events during these years have an eerie resonance to what’s happening today in 2022. War, conflict, inflation, recession, and rate hikes were common themes in these midterm years. Only three of these 10 midterm years had sizable gains: 1938 (War in Europe), 1942 (WWII) and 1982 (Secular Bull). Losses carried over into Q2 in all but 3 years: 1938, 1942 and 2018. Third quarters rebounded in all but three years: 1966 (Vietnam), 1974 (Oil Embargo/Watergate) and 2002 (Iraq). The only real Q4 blemish was 2018 when the Fed hiked rates too briskly.

![[Down Midterm Q1 Table]](/UploadedImage/AIN_0422_20220331_Down_Q1_Midtern_S&P.jpg)

In general, after a down midterm Q1, losses tended to carry over into Q2 and the market began to find its footing in Q3 and rally into Q4. Protracted crises in 1962, 1966, 1970, 1974, and 2002 delivered the most negative results though all had significant bear market bottoms. At the Q1 crossroads in 2022 we are faced with similar conditions. Persistent hyper inflation (Jeff’s large iced black coffee is up 29% in the last month from $3.02 to $3.89), a rising rate environment that’s stoking inverted yield curve/recession fears, the brutal war in Ukraine and the new

Cold War 2.0 with Russia are threatening a bear market on the backdrop of the

heightened volatility we have been warning of since our

Annual Forecast in December.

War Low Support Holding

Technically we are encouraged by the fact that the intraday low on February 24, the day Russia invaded Ukraine, has held and survived at least one solid test on March 14. We have been using the NASDAQ 100 Index (NDX), which is tracked by the Invesco QQQ Trust (QQQ), as our benchmark of late as it has been leading the market in both directions for several years. As we have illustrated in the chart here the lows on February 24 and March 14 with the late-February/early-March rally in between has created a potential W-123 swing bottom. The 14300 level around point 2 becomes support, which is also right at the 50-day moving average. NDX has bumped into resistance around 15000 and the 200-day moving average.

![[NDX Chart]](/UploadedImage/AIN_0422_20220331_NDX.jpg)

It was also encouraging that the market had rallied back up to and through the 200-day moving average. Reclaiming the 200 DMA again would be most constructive. Market internals are also improving with advancers recently outpacing decliners and new highs beating new lows. Continued improvement technically and internally is needed for the rally to have staying power. Barring any major escalation in Ukraine, we suspect the market to log additional gains in April as the Best Six Months come to a close and then move sideways during much of Q2 and Q3. Likely testing the lows before rallying in Q4 and into 2023.

Recession Not Forgone Conclusion.

Financial pundits, market analysts and economists have been debating when and if the economy will go into recession and what that means for the stock market. We’ve all heard the stats that bear markets lead recessions by 8 months or so. But the dire warnings that the slightly inverted yield curve or the negative yield spread that has recently occurred will definitely lead to recession may be an exaggeration and a fear tactic to get attention. Yes, a solidly inverted yield curve or negative spread is an indication of recession. But this slight inversion can also remedy itself before becoming recessionary. In addition, these inversions of the past everyone is citing came from much higher interest rate levels and none have occurred from anywhere near the historically low rates we have now. It’s a big difference going from 4.75 to 5.50 as we did in 1999 than going from Zero to 1.0.

Many have pointed out that the lead time from these negative spreads or inversions to recessions has been years in many instances. There is also something odd with the negative yield spreads this time around. Unlike any previous period, while the spread between the 10-year and the 2-year is going down toward zero the 10-year/Fed Funds spread is rising.

Perhaps a recession is not such a foregone conclusion or at least it may only happen years down the road. We will suffer another recession, someday. But it is hard to fathom a recession in the near future with the unemployment rate and claims so low and states flush with cash, infrastructure spending and the massive proposed federal budget currently on the table.

Worst Six Months Prep

It’s time to be on the lookout for our Best Six Months MACD Seasonal Sell Signal for DJIA and S&P 500. So, here’s a reminder to longtime subscribers and a synopsis for new subscribers. We do not simply “Sell in May and go away.” We employ a more nuanced and subtle approach to how we implement our Best & Worst Months Switching Strategies. We are not issuing the signal at this time.

As we prepare for our upcoming Best Six Months Seasonal MACD Sell Signal that can occur any time on or after April 1 there are several factors and aspects of the strategy, we’d like to be sure you’re up to speed on. DJIA’s and S&P 500’s “Worst Six Months” are May through October. NASDAQ’s “Worst Four Months” are June through October. We begin tracking DJIA and S&P 500 for our “Best Six Months” MACD Seasonal Sell Signal on or after April 1. We begin tracking NASDAQ for its “Best Eight Months” MACD Sell Signal on or after June 1.

We will issue our Seasonal MACD Sell Signal when corresponding MACD Sell indicators applied to DJIA and S&P 500

both crossover and issue a new sell signal on or after April 1. We will not be issuing our NASDAQ Best Eight Months MACD Sell Signal until on or after June 1. Historical dates for the “Sell Signal” can be seen in the tables under the “

Our Strategy” tab on the website.

When we issue our DJIA and S&P 500 Seasonal Sell Signal you will receive an email Alert after the close that day. At that time, we will either sell associated positions outright or implement tight trailing stop losses. Additional bearish and defensive positions as well as other protective strategies may also be considered. All current stock and ETF holdings will be reevaluated at that time. Weak or underperforming positions can be closed out, stop losses can be raised, new buying can be limited, and we will evaluate the timing of adding positions in sectors that perform well in the Worst Six Months and presenting you with a new basket of defensive stocks.

The news flow on the war, the Fed, oil prices and inflation will drive the daily volatility. So, we will be sticking to our playbook guided by our seasonal, fundamental, technical, monetary and market psychology disciplines.

Pulse of the Market

After struggling throughout much of the year DJIA appears to have found support in March just above 32500. At its closing low on March 8, DJIA was down –10.2% year-to-date and down –3.71% for March. From that low through yesterday’s close DJIA was up 3.94% for March and its year-to-date loss has been trimmed to –3.05%. DJIA has reclaimed both its 50- and 200-day moving averages (1). The robust rally is also confirmed by positive readings from both the faster and slower moving MACD indicators (2) applied to DJIA. However, despite the recent brisk rally, DJIA still needs to reverse the death cross that was formed earlier in March when its 50-day moving average fell below its 200-day moving average.

DJIA’s recent rally and back-to-back winning weeks (3) snapped its five consecutive week losing streak. S&P 500 (4) and NASDAQ (5) have also advanced for two straight weeks. More gains by all three are needed to fully undo the damage already done this year. DJIA has fallen in 8 of the 12 weeks so far this year with five Down Friday/Down Monday occurrences throughout. S&P 500 and NASDAQ have just one less weekly loss. A third week of gains would certainly test the stamina of the bears.

NYSE Weekly Advancers and Weekly Decliners (6) have been consistent with the market’s overall move. Decliners have outnumbered Advancers during losing weeks while the opposite occurred in advancing weeks. Two exceptions were the last full week in February and last week when weekly gains were logged even as Weekly Decliners outnumbered Weekly Advancers. Last week’s meager number of Weekly Advancers is concerning as it would appear that participation in the rally has already started to wane.

On a somewhat bullish note, Weekly New Highs (7) have begun to tick higher while Weekly New Lows have declined rather quickly. For the rally to continue New Highs will need to continue to climb and New Lows should also continue to fall. Considering all the uncertainty the market faces, it could be a choppy trend in either direction.

After briefly dipping in late-February and early-March, the 90-day and 30-year Treasury rates have resumed their climbs higher (8). Both are still significantly lower than headline CPI which would seem to suggest that the bond market still does not expect the elevated levels of inflation that have been prevalent for nearly a year to persist indefinitely. Depending on how aggressive the Fed moves on rates, the 90-day rate could climb quicker than the 30-year rate pushing the yield curve ever closer to a full inversion. The Fed certainly has a significant challenge in front of them and their pace of tightening is likely still the biggest threat to the market along with any escalation in Russia’s invasion of Ukraine.

|

April Almanac & Vital Stats: DJIA Up 16 in a Row

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

March 24, 2022

|

|

|

|

April marks the end of the “Best Six Months” for DJIA and the S&P 500. The window for our seasonal MACD sell signal opens on April 1st. From our Seasonal MACD Buy Signal on October 8, 2021, through today’s close, DJIA is down 0.11% while S&P 500 is up 2.93%. This is below historical average performance due largely to surging inflation, a tightening Fed and Russia’s invasion of Ukraine. But before the “Worst Months” arrive, April’s solid historical track record could keep the current rally intact.

![[Seasonal April Market Chart]](/UploadedImage/AIN_0422_20220324_April_Seasonal.jpg)

As you can see in the above chart of the recent 21-year market performance in April, the month has been nearly perfect with gains steadily building from the first trading day to the last with only the occasional and minor blip along the way. April 1999 was the first month ever to gain 1000 DJIA points. However, from 2000 to 2005, “Tax” month was hit, declining in four of six years. Since 2006, April has been up sixteen years in a row with an average gain of 2.9% to reclaim its position as the best DJIA month since 1950. April is the best month for S&P 500 and third best for NASDAQ (since 1971).

The first trading day of April and the second quarter, has enjoyed notable strength over the past 27 years, advancing 19 times with an average gain of 0.28% in all 27 years for DJIA. However, five of the eight declines have occurred in the last nine years. The largest decline was in 2020 when DJIA declined 4.44% (973.65 points). Other declines were in 2001, 2002 and 2005. S&P 500’s record on April’s first trading day matches DJIA, 19 advances in 27 years. NASDAQ recent performance is slightly weaker than DJIA and S&P 500, but the day is still bullish for technology stocks in general with more advances than declines during the same period.

The first half of April used to outperform the second half, but since 1994 that has no longer been the case. The effect of April 15 Tax Deadline (April 18 for 2022) appears to be diminished with numerous bullish days present on either side of the day. Traders and investors are clearly focused on first quarter earnings and guidance during April. With conflict in eastern Europe and the Fed raising rates, companies may lean conservative with guidance during this upcoming earnings season.

Typical midterm-election year woes have tempered April’s performance since 1950. April is DJIA’s and S&P 500’s seventh best month in midterm-election years, up 12 of the last 18. Russell 2000 ranks highest at fifth best in midterm-year Aprils. Sizable losses exceeding 4% on DJIA and S&P 500 occurred in 1962, 1970 and 2002.

Monthly options expiration week frequently impacts the market positively in April and DJIA has the best track record since 1991, with an average gain of 1.40% for the week with just five declines in 31 years. The first trading day of expiration week has a slightly better record (average gain) than expiration day and the week as a whole is generally marked by respectable gains across the board. The week after has a softer long-term record, but still has a bullish leaning record.

Good Friday (as well as Passover and Easter) lands in the middle of April this year. Historically the longer-term track record of Good Friday (page 100 of STA 2022) is bullish with notable average gains by DJIA, S&P 500, NASDAQ, and Russell 2000 on the trading day before. NASDAQ has advanced 20 of the last 21 days before Good Friday. Monday, the day after Easter has exactly the opposite record since 1980 and is in the running for the worst day after of any holiday. Since 2004 the day after has been improving with S&P 500 up 12 of the last 18.

|

April 2022 Strategy Calendar

|

|

By:

Christopher Mistal

|

March 24, 2022

|

|

|

|

|

Tactical Seasonal Switching Strategy Update: Midterm Year “Worst Months” Historically Weakest

|

|

By:

Christopher Mistal

|

March 17, 2022

|

|

|

|

We are not issuing the signal at this time.

From our Seasonal MACD Buy Signal on

October 8, 2021 through today’s close, DJIA is down 0.76%, S&P 500 is up 0.46% while NASDAQ is down 6.62%. At this stage of the “Best Months,” this performance is disappointing and far from what was anticipated at the start of the current cycle. However, there is still ample time for the market to move higher before the “Best Months” officially come to an end at the end of April for DJIA and S&P 500 and NASDAQ in June. Our Seasonal MACD Sell trigger could extend the “Best Months” in the event the market does continue to rally, or it could do just the opposite and move us to a more cautious posture should the rally fail.

The long-term track record of our Seasonal Switching Strategy, which is based on the “Best Six Months” in conjunction with our MACD Technical Buy and Sell Signals, has a solid track record of outperformance with potentially less risk compared to a buy and hold approach. Since 1950, DJIA’s average annual gain has been 8.7%. Over the same time period, DJIA has lost an average 0.4% during the “Worst Six Months,” May through October, and gained an average 8.9% during the “Best Six Months,” November through April.

Detractors are quick to point out that there have been positive “bad” months and negative “good” months. This is absolutely true as there is no trading or investment strategy that works 100% of the time (even the best will report a trading loss every once and a while). In midterm election years, the second weakest year of the four-year cycle (page 132, STA22), there is a history of selloffs during the “Worst Months.”. The “Worst Months” in 1974 hosted the largest decline. More recently, during 1998 and 2002, the “Worst Months” were also negative. Each of the last 17 Midterm Year “Worst Months” can be seen in the following table. DJIA and S&P 500 Worst Six Months are May through the end of October. NASDAQ’s “Worst Four Months” are July through end of October.

Considering the negative historical average gains in Midterm years, during the “Worst Months” a cautious approach is worth consideration once again during this upcoming early spring/summer. The Covid-19 economic shutdown and ensuing bear market in Q1 of 2020 resulted in a loss for DJIA and S&P 500 during that year’s “Best Months” and an outsized market gain during the “Worst Months” as aggressive fiscal and monetary policy supported a quick recovery. And this year, the Fed has begun a rate increase cycle in the “Best Months” while Russia’s invasion of Ukraine is only further compounding the market’s challenges.

Market strength during recent “Worst Months” periods and weakness during the “Best Months” does not appear to be the result of any permanent change in historical seasonal patterns. It has been triggered by exogenous events and the fiscal, monetary and political responses to those events. Unlike the quick market reversal of March 2020, the Fed, elevated inflation, and Russia’s invasion of Ukraine could easily extend through the entirety of this year’s “Worst Months.”

Applying Our Seasonal Switching Strategy

Because of the elevated level of risk that has been historically observed during the “Worst Six Months” of the year and its historically tepid returns, reducing long exposure and developing a defensive strategy is the approach we take in the Almanac Investor Stock and ETF Portfolios. We do not merely “sell in May and go away.” Instead we take some profits, trim or outright sell underperforming stock and ETF positions, tighten stop losses and limit adding new long exposure to positions from sectors that have a demonstrated a record of outperforming during the “Worst Months” period.

For those with a lower risk tolerance or a desire to take a break from trading, the “Worst Months” are a great opportunity to unwind longs and move into the relative safety of cash, Treasury bonds, gold and/or some combination of these safe havens. Preservation of capital may be more important than growth and with historical averages and frequency of gains reduced; the “Worst Six Months” are a good time to simply step aside if you prefer. August, September and/or October have provided some excellent buying opportunities in recent years and could do the same again this year.

Potential Worst Months Moves

We are not issuing the signal at this time. We are only preparing you for when it does arrive.

Currently, the Almanac Investor Stock Portfolio and ETF Portfolio are positioned with a long-only bias for the “Best Months” with no long exposure to bonds, no short positions in individual stocks or sectors, or positions in bear market funds. But, beginning April 1, 2022 we will begin looking for our seasonal MACD sell signal. When it triggers, we will transition to a less aggressive stance in the portfolios.

When both the DJIA and S&P 500 MACD Sell indicators trigger a new sell signal on or after April 1, we will issue an Almanac Investor Alert. We will either outright sell specific existing positions or implement tight trailing stop losses. We will also consider establishing new positions in traditionally defensive areas of the market which may include bond ETFs, gold and gold stocks, outright bearish (short) positions and other sector ETFs with a demonstrated track record during the “Worst Six Months.” All stock and ETF holdings will be evaluated at that time. ETFs providing exposure to sector seasonalities ending in April and May along with underperforming stocks in the Almanac Investor Stock Portfolio may be sold at that time as well.

For traders and investors employing the “Best 6 + 4-Year Cycle” as detailed on page 64 of the Stock Trader’s Almanac 2022, this year’s upcoming Seasonal MACD Sell signal should be heeded.

|

Stock Portfolio Updates: Holding for the Fed

|

|

By:

Christopher Mistal

|

March 10, 2022

|

|

|

|

Even after yesterday’s solid gain, the S&P 500 was still officially in a correction. But, just how good of an indicator is the S&P 500? Is it really on track to forecast a U.S. or global recession in the near future? A look back at S&P 500 past track record suggests around a 1 in 3 chance of a U.S. recession at this point. The historical odds of the current correction turning into a bear market are also about 1 in 3.

First a quick review of definitions. A bear market is widely defined as a 20% or greater decline in the S&P 500. A correction is typically defined as a decline greater than 10% yet less than 20%. Based upon these definitions every bear market begins as a correction, but not every correction becomes a bear market. As of today, at its closing low on March 8 of 4170.70, S&P 500 was off 13.0%. To be in an official bear S&P 500 would need to close below 3837.25.

Since June 15, 1948, there have been 12 S&P 500 bear markets and 27 corrections. Excluding the current correction from the tally there have been 38 declines in excess of 10%. However, the National Bureau of Economic Research has only identified 12 recessions over the same time period. This works out to less than 1 recession for every 3 S&P 500 declines in excess of 10%. It is also interesting to note that even though there have been 12 S&P 500 bear markets and 12 U.S. recessions since 1948, four of the recessions did not line up with S&P 500 bear markets.

Clearly there are ample reasons to be pessimistic about the market and the economy. Even before Russia invaded Ukraine energy prices had been steadily climbing higher and inflation was running at multi-decade highs spurring the Fed to start to step on the monetary policy brake pedal. The Fed has been quickly bringing QE to an end and prepping the market for a series of rate increases. Russia’s invasion of Ukraine and the elevated uncertainty it adds to the overall outlook is only going to make the Fed’s task all that much more difficult.

There are also reasons to remain optimistic about the economy and the market. The U.S. labor market remains firm with more job openings available than there are people looking for work. Energy prices are finally pausing and have actually begun to retreat. Corporate earnings have held up well and estimates for 2022 S&P 500 stock buybacks are around $1 trillion. It is also worth pointing out that S&P 500 is about 13% off its all-time high after rallying nearly 115% off its March 2020 low.

As we noted way back in December in our

2022 Annual Forecast, volatility was expected this year. At that time Russia was not waging war with Ukraine and energy had not surged to multi-year highs. Our main concern then was the Fed, and it appears the market maybe drifting back toward that concern once again. When Treasury bond yields were climbing earlier this year, hi-grow technology stocks were getting hit. With the 10-year Treasury yield hitting 2% today, many of those familiar names are getting hit again today. One notable exception is Amazon as the market is initially reacting rather positively to Amazon’s announced stock split and buyback plan.

Next week we will hear from the Fed. They are widely expected to raise rates and revise their outlook lower. We also expect they will acknowledge the heightened level of uncertainty caused by Russia/Ukraine. Should they provide a clearer path to monetary policy normalization it could remove some uncertainty from the market, but trading is likely to remain choppy. We will continue to stick to our strategy while heeding stop losses and remaining vigilant for the next buying opportunity. Historically, in midterm years it has arrived in Q3 or early Q4.

Free Lunch Update

Per last month’s update, the last position from December’s Free Lunch basket of stocks was closed out. Core Laboratories (CLB) was exited using its average price on February 11 for a gain of 24.6% excluding any trading costs or dividends. More recently CLB has briskly rallied on speculation that higher energy prices could lead to increased demand for oil and gas equipment and services. Based upon the recent brisk retreat in crude, CLB’s recent rally could be short-lived. The Free Lunch section of the overall Almanac Investor Portfolio will be removed in the next update. The cash balance will return to where it came from, the overall portfolio.

Stock Portfolio Updates

Over the last four weeks since last update through yesterday’s close, S&P 500 dropped 6.7% while Russell 2000 slid 3.2% lower. Over the same time period the entire portfolio slipped 0.5% lower, excluding dividends and any fees. Small-Cap positions, on average, were the worst performing off 2% as two positions were stopped out. Large-Caps were second worst, off 1.0%. Mid-Caps advanced 1.4% on average. In total, across all segments only two positions were stopped in the second half of February and early March.

Both positions that were stopped out were in the Small-cap portfolio. Broad market weakness combined with interest rate pressures appear to be the main reasons why both positions retreated. KB Home (KBH) was the first to be stopped out on February 22 followed by Customers Bancorp (CUBI) earlier this week. Both positions have bounced back modestly and did post gains today. In the near- and intermediate term, housing and banks could see continued pressure due to interest rates. Higher rates usually translate into higher mortgage rates which tend to weigh on housing demand while it appears likely that the yield curve will flatten instead of significantly steepen as the Fed raises its short-term rate.

Moving up to the Mid-cap portfolio, Pacira BioSciences (PCRX) was the driver behind this section of the total portfolio advancing over the last four weeks. Solid quarterly results that beat expectations on both the top and bottom lines appear to be the catalyst for PCRX’s solid recent gains. PCRX is on Hold.

Sharply rising fuel prices have prompted a tighter stop loss of $42.00 for Werner Enterprises (WERN). Shares have held up quite well, but it remains to be seen if WERN will be able to pass through costs to its customers as quickly as they are rising.

AT&T (T) is the sole open position that was in the red on the close on March 9. Despite some clarity on its dividend and its media properties, T’s struggles have continued. As a reminder, T intends to spin off Warner Media and merge it with Discovery Inc. while its dividend will be cut to $1.11 per share. When the spin off completes T shareholders will receive 0.24 shares of Warner Bros. Discovery for each share of T held. Hold shares of T as the spin off does appear it may be beneficial to both T and the new media company.

All other positions are on Hold. Please see the table below for updated stop losses and current advice for positions not covered above.

|

ETF Trades & Portfolio Updates: Taking Energy Sector Profits

|

|

By:

Christopher Mistal

|

March 03, 2022

|

|

|

|

It has been a little more than a week since Russia invaded Ukraine. The invasion removed one uncertainty (why is Russia amassing forces along the border) and introduced countless more for the market to sort through. Market volatility has remained elevated, but thus far it has not spiked to the levels last seen at the beginning of the pandemic. Ukraine has successfully resisted Russia forces thus far and the international community has come together in a limited capacity to hit Russia and its supporters with sanctions. What ultimately unfolds in Ukraine is still an unknown, but it is increasingly clear that Russia’s current leadership is going to forever be shunned by the majority of nations regardless of the war’s outcome. The human toll and economic impacts are likely to be long-lasting as well.

Last week we presented a table of past

Geopolitical & Energy Crises in an effort to provide some context for current events. Some observations that can be made from that table is the market always finds a way to work itself higher, but the exact timely largely depends on the duration of the crises and any long-lasting effects. Timing of the crisis also appears to play a role in the market’s response as crisis during a relatively healthy domestic economy such as the Cuban Missile Crisis had only a minimal impact on the intermediate- and longer-term trajectory of the market while the Arab Oil Embargo only worsened an already tough economic situation. The current Ukraine crisis arrived when the U.S. economy and market was relatively healthy so it is reasonable to expect, provided the situation doesn’t considerably escalate, that current volatility will eventually recede and the market will get back to doing what it has historically done, climb higher.

Since this year is a midterm year, it would not be completely without historical precedent for the market to remain volatile throughout the balance of the first quarter into Q2-Q3 before finally finding firmer footing. The midterm bottom could also arrive early this year. Continue to heed stops, remain focused on your strategy, and be prepared to put any cash back to work.

New Sector Seasonality

There is one new sector seasonality that begins in April: Computer Tech. We are going to look to take advantage of current weakness this month to establish a new position associated with this sector. In the following weekly bar chart of the Computer Technology (XCI), seasonal strength (lower pane, shaded in yellow) typically begins following an early or mid-April bottom and usually lasts through around mid-July although the bulk of the move can occur early. Market volatility over the past two years has influenced the seasonal pattern, but in the upper pane there was a clear move higher by XCI off of its March lows last year.

![[Computer Technology Index (XCI) Weekly Bars and Seasonal Trend Chart]](/UploadedImage/AIN_0422_20220303_XCI_Seasonal.jpg)

With over $45 billion in assets and ample average daily trading volume, SPDR Technology (XLK) is a top choice to consider holding during Computer Tech’s seasonally favorable period. It has a gross expense ratio of just 0.10%. Top five holdings include: Apple, Microsoft, NVDIA, VISA and Mastercard. Please note, Apple and Microsoft combined account for 46.39% of XLK’s holdings as of March 2 close.

XLK could be considered on dips with a buy limit of $152.85. This is right around its projected monthly pivot point (blue-dashed line in daily bar chart below). After declining for two months, technical indicators applied to XLK are beginning to improve. MACD has turned positive while Relative Strength and Stochastic indicators are also improving. Based upon its 15-year average return of 8.1% (excluding dividends and trading fees) during its favorable period mid-April to the middle of July, set an auto-sell price at $181.75. If purchased an initial stop loss of $137.57 is suggested. For tracking purposes, XLK will be added to the Sector Rotation ETF portfolio if it trades below its buy limit.

Sector Rotation ETF Portfolio Update

February certainly lived up to its historical reputation this year as a weak link in the Best Months as widespread market weakness persisted throughout the month. Market-wide weakness did translate into declines for many positions in the Sector Rotation portfolio. Once again, two notable exceptions were SPDR Gold (GLD) and SPDR Energy (XLE) as both enjoyed solid gains over the last month. GLD was up 32.2% since addition at yesterday’s close. Continue to Hold GLD.

With crude oil breaking above $110 per barrel, XLE traded to and above its associated auto-sell price on March 2. Per standard trading guidelines, XLE was sold at 73.19 and closed out of the portfolio. In response to several member inquiries, instead of outright selling XLE, one could consider implementing a tight trailing stop loss on the position or consider selling a portion of the position at the auto-sell price and holding the remaining with a tight trailing stop loss. Should nations decide to truly ramp up sanctions on Russia and stop buying its crude, prices could easily jump much higher, but on the flip side of this is the fact that a large premium has already been built into to crude’s price and any talk of a ceasefire and negations could just as easily trigger a sizable retreat in crude.

Global X Copper Miners (COPX) and First Trust Natural Gas (FCG) have also had a good month up 17% and 14.4% respectively at yesterday’s close. Natural gas has been rallying in sympathy with crude, although to a lesser extent. Copper has jumped this week possibly in response to falling mortgage rates and persistently strong demand for housing. COPX and FCG are on Hold. Unfortunately, United States Copper (CPER) was stopped out in the first half of February.

SPDR Financial (XLF) was stopped out on March 1 at 37.28. Typically the prospects of higher interest rates and a steepening yield curve have been positive for the banks, but it is increasingly looking like the yield curve is flattening as near-term rates creep higher in anticipation of the Fed while long-term rates are not rising nearly as much. A flattening yield curve has not been a positive for the banking sector. A second risk is sanctions on Russia. Anyone remember BRIC? That “R” was for Russia, and it is likely a safe assumption that there are more Russian assets at Western banks than one may think. The potentially most damaging assets that banks could be holding are bonds issued by Russia corporations or Russia itself.

SPDR Industrials (XLI) was stopped out on February 23. It would appear it just got wrapped up in broad selling at the peak of the Fed rate hike cycle discussion as XLI has since bounced back. During XLI’s recent decline its 50-day moving average has fallen below its 200-day moving average. This crossover is frequently called a “death cross.” With XLI quickly approaching its 50-day moving average we will take a wait-and-see approach. It would not be surprising to see XLI fail to reclaim its 50-day moving average on its first attempt.

SPDR S&P Biotech (XBI) is still the worst performing position in the portfolio, and it was down more today. As a reminder, XBI is intended to be a long-term core holding in the portfolio. The magnitude of its selloff is starting to gather some attention now that its price has returned to pre-covid levels. XBI is on Hold.

Last month’s new trade ideas, iShares DJ US Tech (IYW) and SPDR Utilities (XLU) have been added to the portfolio. As of the market’s close on March 2, IYW was up a modest 2.2% while XLU was down 0.4%. After today’s session, both are positive even though IYW retreated. IYW and XLU are Hold.

With the exception of the new trade ideas, all other positions in the portfolio are currently on Hold.

Tactical Seasonal Switching Strategy Portfolio Update

As of yesterday’s close, the Tactical Seasonal Switching Strategy portfolio had an average loss of 3.5% since our Seasonal Buy Signal. iShares Russell 2000 (IWM), is the worst performing position in the basket, down 8.0%. However, this is actually an improvement since last month. If IWM can find support and rally, it would be a welcome and encouraging sign. SPDR S&P 500 (SPY) was the last remaining positive position, up 0.1%. All positions in the portfolio are on Hold.

Positions in the Tactical Switching Strategy portfolio are intended to be held until we issue corresponding Seasonal MACD Sell Signals after April 1 for DJIA and S&P 500 and after June 1 for NASDAQ and Russell 2000. Due to this no stop loss is suggested on these positions and ample time remains for the market and these positions to improve.