|

Market at a Glance – May 29, 2025

|

|

By:

Christopher Mistal

|

May 29, 2025

|

|

|

|

Please take a moment and register for our members’ only webinar, June 2025 Outlook & Update on Wednesday June 4, 2025, at 4:00 PM EDT here:

Please join us for an Almanac Investor Member’s Only discussion of recent market action with time for Q & A at the end. Jeff and Chris will cover their outlook for June 2025, review the Tactical Seasonal Switching Strategy ETF, Sector Rotation ETF, and Stock Portfolio holdings and trades. We will also share our assessments of the economy, tariffs, Fed, inflation, geopolitical events as well as relevant updates to seasonals now in play.

If you are unable to attend the live event, please still register. Within a day of completion, we will send out an email with links to access the recording and the slides to everyone that registers.

After registering, you will receive a confirmation email containing information about joining the webinar and a reminder message.

Market at a Glance

5/29/2025: Dow 42215.73 | S&P 5912.17 | NASDAQ 19175.87 | Russell 2K 2074.78 | NYSE 19743.85 | Value Line Arith 10872.06

Seasonal: Neutral. June is the last month of NASDAQ’s “Best Eight Months.” NASDAQ’s Seasonal MACD Sell signal can occur anytime on or after June 2, 2025. NASDAQ and Russell 2000 have performed best in June with average gains of 1.0% and 0.8% respectively. June ranks #11 for DJIA (–0.2%) and # 9 for S&P 500 (+0.2%) since 1950. In post-election years, June is also #11 DJIA and #9 S&P 500, but average performance weakens to –1.0% and –0.5% respectively while Russell 2000 improves to 1.2% and NASDAQ eases to 0.8%.

Fundamental: Mixed. Q1 GDP was revised 0.1% higher but remained negative at –0.2% and the Atlanta Fed’s GDPNow model’s forecast for Q2 GDP has retreated to 2.2% as of its May 27 update. Headline CPI continues to slowly retreat yet remains above the Fed’s stated 2% target. Labor market metrics are holding up with the unemployment rate holding steady at 4.2% and monthly jobs gains of 177,000 in April. Paused tariffs put in place under IEEPA (International Emergency Economic Powers Act) are being challenged in court but other legal paths appear to exist for the administration to continue using tariffs.

Technical: Consolidating? DJIA, S&P 500, NASDAQ, and Russell 2000 have all reclaimed their respective 50-day moving averages. S&P 500 and NASDAQ have climbed even higher and have pushed above their 200-day moving averages, but all four indexes have traded modestly lower or sideways since around mid-May. Near-term support levels around the May 9th closes are DJIA 41250, S&P 500 5660, NASDAQ 17930 could come into play.

Monetary: 4.25 – 4.50%. Following their May meeting, the Fed confirmed that they are still in no rush to resume cutting rates as inflation remains elevated and the labor market is reasonably firm. As of today, May 29, the odds for a June rate cut are effectively zero according to the CME Group’s FedWatch Tool. Arguably, the Fed was late to act when inflation began surging in 2021 and they will likely be late again.

Sentiment: Neutral. According to

Investor’s Intelligence Advisors Sentiment survey Bullish advisors stand at 41.5%. Correction advisors are at 32.1% and Bearish advisors were at 26.4% as of their May 28 release. The improvement in the number of bulls is encouraging while the number of remaining bear and correction advisors leaves room for the market to continue to rally as overall sentiment is not excessively bullish.

|

June Outlook: After June Consolidation Big May Bodes Well for Year

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

May 29, 2025

|

|

|

|

As we put the finishing touches on the manuscript for the 2026 Stock Trader’s Almanac, our 59th annual edition, this week and formulate our advanced outlook for 2026, we have been assessing how our 2025 forecast has fared. We underestimated the voracity with which the Trump 2.0 administration would prosecute its trade policy and tariff negotiations. But we did nail the heightened volatility and first quarter weakness that ran over into early April.

Back in December we gave our Base Case

Annual Forecast scenario a 65% probability for gains of 8-12% for 2025. Inflation risks tempered our bullish outlook, but we expected Trump 2.0 policy initiatives to stir the animal spirits and boost business, the economy and markets in line with the more recent bullish history of post-election years. The year sure started out that way climbing to new highs, but the President’s “art-of-the-deal” shock and awe style was a bit too shocking causing a spike in volatility and a steep correction.

Market volatility has been bullishly crushed since the April 8 low and in the process the rally has triggered a host of other bullish technical readings we detailed in the

Mid-Month Update two weeks ago. As you can see from the S&P 500 chart below several resistance levels have been cleared over the past four weeks: 5500 and 5670, the 50-day moving average (pink line), and the 200-day moving average (blue line).

Still 50/50

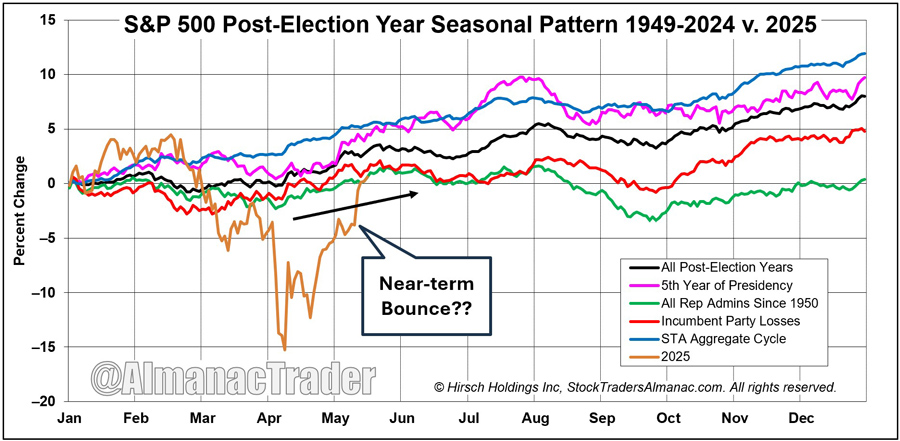

Despite the face-ripping rally S&P 500 is still flat on the year, up a mere 0.53% at today’s close. It is also tracking the two least bullish scenarios in the Post-Election Year Seasonal Pattern Chart below. The green line illustrates how closely 2025 is tracking this dubious pattern of old school Republican Administration Since 1950. The red line shows how in the year after Incumbent Party Losses markets tend to mark time as they adjust to the new sheriff in town and the new agenda.

On page 28 of the 2025 Almanac, we discuss the tendency of Republican Presidents to get down to brass tacks right out of the blocks whereas the Dems tend to hem and haw and not get around to big policy changes until the midterm year. President Trump has implemented more policy initiatives faster than any president we can remember. If this pace of shock-and-awe-and-pause-and-negotiate continues, the market is likely to chop around and go sideways until we get some real deals and the economy and/or market leaders knock some results out of the park.

It is this year’s rollercoaster and flat year-to-date performance that has shifted our outlook to 50/50 Base Case/Worst Case. If we can solidify some trade deals and log some good economic and corporate hard data points and continue to build on the constructive market action, then the odds of significant new highs increases. If the Trump Administration’s agenda flounders and data disappoints our flat to negative scenario for the year becomes more likely.

Big May Gains Are Good

With one trading day left, May is delivering some very merry gains once again. The table below shows all the years since 1950 when May logged a gain of 3% or more on the S&P 500. This is the second year in a row this has occurred and last year finished quite strong. All post-election years like 2025 are highlighted in orange. The next seven months of these years have done quite well, up 13, down 5 with an average gain of 8.7%, which would be right on target for our Base Case Annual Forecast scenario. June is the weak link in this dataset, up only 11 of the 18 years with a paltry average gain of 0.5% which aligns well with June’s historical lackluster performance. Q4 stands out here with some solid numbers and only two losses at the outset of the GFC in 2007 and during the 1957 bear market and recession.

NASDAQ Best 8 Months MACD Sell Criteria

Our NASDAQ Best 8 Months MACD Sell has NOT triggered. The market’s sideways trading the past two weeks has put NASDAQ’s Best 8 Months MACD Sell indicator close to the triggering criteria. If the NASDAQ Composite does not gain more than 95.72 points tomorrow, our NASDAQ MACD Sell indicator will get reset.

We calculate MACD using daily closing prices with a short exponential moving average (EMA) of 12 days, a long EMA of 26 days and a 9-day period EMA for the signal line, frequently written as 12-26-9. A sell signal is triggered when the signal crosses below the MACD line on or after the first trading day of June. We require a NEW Sell Signal after the first trading day of June. If the 9-day signal line comes into the month below the MACD line, then it must rise above and cross below it again after the first trading day of June.

The market has become somewhat desensitized to President Trump’s tariffs and trade war and continues to shrug off other corporate, economic and geopolitical setbacks rather summarily. We find it hard to get bearish here yet hard to get super bullish. With the Worst Six Months upon us, the ominous post-election pattern behavior we are witnessing and flat YTD performance, plus the technical resistance at Election gap we see no reason to overextend ourselves. Besides, the Fed is not doing anything until there is a fire to put out or it gets more clarity on fiscal policy, trade, the tax bill and immigration.

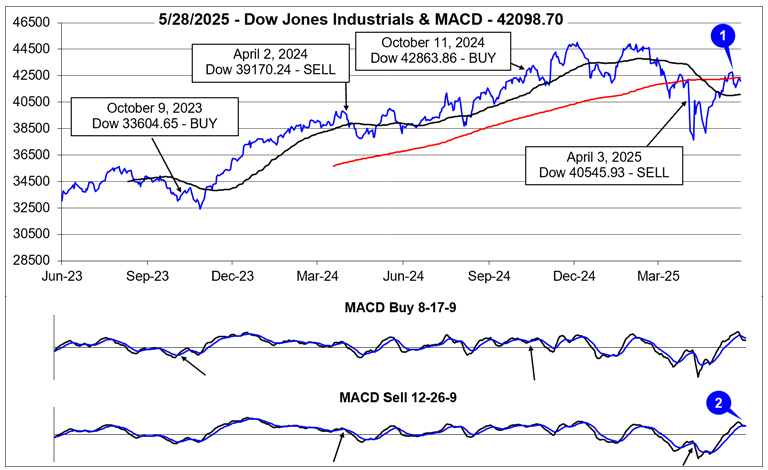

Pulse of the Market

April’s rebound rally continued in May and DJIA reclaimed its 50-day moving average and briefly its 200-day moving average (1) around mid-month. As of the close on May 28, DJIA was up 3.5% in May which is well above its average post-election year May average performance of 1.3% since 1950. However, DJIA is still down year-to-date 1.0%. Since mid-month, DJIA has modestly retreated and the shift in momentum has turned both the faster and slower moving MACD indicators negative (2). Historically, June has been a tepid month in post-election years and DJIA appears to be heading in that direction.

Despite the impressive gains since the April lows, weekly performance confirms the volatile and choppy nature of the recovery rally. Over the last seven full weeks, DJIA has advanced four times and declined three times (3). Three of the weekly gains were in excess of 1000 DJIA points while two of the weekly losses were also in excess of 1000 points. S&P 500 (4) and NASDAQ (5) have the same number of weekly gains and losses but with even larger gains and weekly swings. Sizable weekly and daily swings are likely to persist as uncertainty over the economic impact of tariffs remains elevated.

Weekly market breadth over the last five weeks has largely been in line with the magnitude of weekly moves. Weekly Advancers have outnumbered Weekly Decliners (6) in four of the past five weeks, most notably during the week ending May 9, when the major indexes all recorded mild weekly declines. However, the streak of four straight weeks of Advancers outnumbering Decliners abruptly ended last week. This sharp reversal also suggests more volatility is likely heading into June and possibly beyond.

Looking at the number of New 52-week Highs over the last five weeks (7), there was an encouraging pattern. New Highs were slowly expanding until declining last week. New 52-week Lows have declined substantially after spiking to nearly 1500 in the first half of April but have been unable to maintain a clear path much lower. New Highs and Lows are likely to continue to bounce around in the near-term as the market remains headline driven.

Apparently fueled by Federal debt concerns, the 30-year Treasury bond (8) yield climbed above 5% during the week ending May 23. On a weekly basis, the last time the 30-year Treasury bond exceeded 5% was in October 2023, for two consecutive weeks. Prior to then, the last time it was above 5% was way back in the spring and summer of 2006. A sustained move above 5% would likely weigh on stocks.

|

June Almanac & Vital Stats: NASDAQ & Russell 2000 Best

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

May 22, 2025

|

|

|

|

Over the last 54 years June has favored NASDAQ ranking sixth best with a 1.0% average gain, up 31 of 54 years (since 1971). This contributes to NASDAQ’s “Best Eight Months” which ends in June. However, June ranks near the bottom on the Dow Jones Industrials just above September since 1950 with an average loss of 0.2%. S&P 500 performs similarly poorly, ranking ninth, but with a 0.2% average gain. Small caps have tended to fare better in June. Russell 2000 has averaged 0.8% in the month since 1979 advancing 63.0% of the time. During the bear market in 2022, Russell 1000 and 2000 suffered their worst June losses ever, dropping 8.5% and 8.4% respectively. S&P 500 and NASDAQ also declined by over 8% that year.

![[Recent 21-Year June Seasonal Chart]](/UploadedImage/AIN_0625_20250522_June_2025_Seasonal_Chart.jpg)

Over the last twenty-one years, the month of June has been a rather lackluster month for the market. DJIA and Russell 1000 have recorded modest average losses in the month. S&P 500 has been essentially flat, averaging +0.002%. NASDAQ and Russell 2000 have fared better, logging average gains of 0.6% and 0.7% respectively. Historically the month has opened respectably, advancing on the first and second trading days. From there the market has tended to drift sideways and lower near or into negative territory just ahead of mid-month. From there the market has rallied to create a mid-month bump that generally has quickly evaporated and returned to losses. The brisk, post, mid-month drop is typically followed by a month-end rally led by technology and small caps.

In post-election years since 1950, June has followed a similar pattern to the recent 21-year period, but there has not been a mid-month rally. Early June strength has been notably stronger for NASDAQ and Russell 2000 while DJIA and S&P 500 have typically struggled throughout past post-election year Junes.

June is the second worst DJIA month in post-election years, averaging a 1.0% loss with a record of fourteen full month declines in eighteen years. For S&P 500, June is #9 with an average loss of 0.5% (7-11 record). Post-election year June ranks #8 for NASDAQ and #7 for Russell 2000 with average gains of 0.8% and 1.2% respectively.

The second Quad Witching Week of the year brings on some volatile trading with losses frequently exceeding gains. On Monday of Quad-Witching Week, DJIA has been down 15 of the last 28 years. Quad-Witching Friday is similar, DJIA has been up 18 of the last 35 years, but down 8 of the last 10. Full-week performance is choppy as well, littered with greater than 1% moves in both directions. The week after June’s Triple-Witching Day is horrendous. This week has experienced DJIA losses in 29 of the last 35 years with an average weekly decline of 0.8% since 1990. NASDAQ and Russell 2000 had fared better during the week after, but that trend appears to be fading.

![[June Vital Stats Table]](/UploadedImage/AIN_0625_20250522_June_2025_Vital_Stats_table.jpg)

June’s first trading day is the Dow’s best day of the month, up 28 of the last 37 years. Gains are sparse throughout the remainder of the month until the last three days when NASDAQ and Russell 2000 stocks begin to exhibit strength. The last day of the second quarter was a bit of a paradox as the Dow was down 17 of 24 from 1991 through 2014 while NASDAQ and Russell 2000 had nearly the opposite record. Since 2015, all indexes have had a bullish bias on the last trading day while DJIA and S&P 500 have been up 8 of the last 10.

|

June 2025 Strategy Calendar

|

|

By:

Christopher Mistal

|

May 22, 2025

|

|

|

|

|

Mid-Month Market & Stock Portfolio Updates: Thrust Verified Ride the Rally

|

|

By:

Jeffrey A. Hirsch & Christopher Mistal

|

May 15, 2025

|

|

|

|

The technical breadth thrusts we discussed in the

May Outlook and on the

monthly member’s only webinar are indeed being verified. As you can see from the S&P 500 technical chart below the market has reclaimed several resistance levels. At the end of April S&P climbed above 5500 at the bottom of the old W-1-2-3 failed swing bottom, moving back above the April-August 2024 uptrend line in the process. In early May S&P reclaimed the descending 50-day moving average (pink line) which now has turned slightly upward. Then after dancing with 5670 last week, which was last July’s peak, we gapped above the 200-day moving average (red circle), the top of the W-1-2-3 pattern and into the Election Day gap (orange circle). The November 6 close (red arrow) around 5929 and the old highs are now in our sights.

![[S&P Technical Chart]](/UploadedImage/AIN_0625_20250515_SP500_Technical_900.jpg)

The CBOE Volatility index (VIX) falling below 20 is also constructive. The V-shaped recovery from the April lows has put S&P fractionally in the black for 2025 year-to-date and back on track with the Incumbent Party Losses (red line) and All Republican Admins Since 1950 (green line) patterns in the S&P 500 Post-Election Year Seasonal Pattern chart below. This market action continues to support our view that the relief rally off the tariff tumble has legs, and we expect it to continue through June and perhaps into July, but not without a healthy dose of chop.

When typical seasonal weakness and post-election Q3 weakness collide with the end of the tariff pauses the market may be prone to another correction in the August-October timeframe. We are bullish short term but remain cautious with this market. The relief rally is encouraging, but the performance so far this year is reminiscent of old-school Republican administration post-election year weakness (

2025 Stock Trader’s Almanac, page 28), so our

outlook has improved slightly to 50/50 base case/worst case. If we can reclaim the February highs our base case of 8-12% gains for the year become more likely, if not then the odds of our worst case for a flat to slightly negative year remain high.

The magnitude of the rally this week is “off the charts,” but it is still on trend with the superlative post-election year May pattern. After a brief pause here in mid-May as the market consolidates the massive turnaround gains from the April lows, we expect the relief rally to continue through early summer before the next correction ensues. We would not be surprised if the rally stalled in mid-July as we have seen in recent years after NASDAQ’s perennial mid-year rally that we call

Christmas in July.

All things considered our April 17 Issue recommendations to get back into Invesco QQQ (QQQ) and iShares Russell 2000 (IWM) for the remainder of NASDAQ’s Best 8 Months November-June are working out quite well with QQQ up 19.7% at today’s close and IWM up 13.9%.

Our most dire concerns we conveyed in the May Outlook with respect to down Aprils after down Q1s and down Best Six Months appear to have been alleviated. DJIA’s swift and strong rebound off the April 8 low of 12.7% to the May 12 recovery high so far moves this market action more toward the 2009 and 2020 down Best Six Months camp though both of those were official bear market bottoms in our book and the 2025 selloff is just a bull market correction in our view.

Finally, if you look closely at the “When Bullish April is Down After Q1 Weakness” table in the

May Outlook and plug in April 2025’s final S&P performance of -0.8% instead of the -2.3% it was at on April 24 four trading days prior it looks more in line with years in the table with milder April losses and more solid yearly performance. Expect some economic, earnings and market adjustments related to tariffs and trade and geopolitics ahead, but the huge turnaround from the lows, dovetails with the end of the Best 8 Months and keeps us bullish near term but cautious about Q3.

Stock Portfolio Updates

Over the past five weeks, through the close on May 14, the Almanac Investor Stock Portfolio advanced 2.4% compared to an 8.0% advance by S&P 500 and an 8.9% gain by Russell 2000. Overall performance was limited by the sizable cash balance in the portfolio. Focusing on just the stock positions held, they collectively advanced an average of 9.8%. The lone small-cap, advanced 8.0%, Mid-Caps jumped 15.3% and Large-Caps rose 6%.

HealWell AI (HWAIF) has rebounded back above $1.00 after reporting record revenue growth in its Q1 of 208% earlier this week. Its acquisition of Orion Health was completed on April 1, and it is expected to contribute around $100 million in annual revenue starting in Q2 which should bring HWAIF close to being profitable. In addition, the acquisition of Orion Health expanded HWAIF’s reach globally by adding 70 large customers across 11 countries. HWAIF can still be considered on dips below its buy limit of $1.

Super Micro Computer (SMCI) is on hold. There is no suggested stop loss as it continues to trade in a wide and volatile range. It is also just a one-fourth position as profits have been taken twice since it was added to the portfolio in November 2022. Profits were taken when SMCI first doubled and a second time when it was trading around $900 (before its recent 10 for 1 split). After a modest retreat today, SMCI is still up over 37% this week. The catalyst for the jump was a rather bullish analyst call. If the analyst is reasonably correct in their calculations, SMCI has around a 9% market share in the AI race.

Grand Canyon Ed (LOPE) is on hold. LOPE reported Q1 results a little over a week ago on May 6 that were overall better than expected. Revenue growth was in line with estimates while earnings were better than forecast. On the news, LOPE traded at new all-time highs last week. Shares have modestly consolidated this week.

InterDigital (IDCC) is on hold. IDCC earnings were somewhat of a mixed bag but nonetheless appear to have been well received. It missed revenue estimates but surprised on earnings. The earnings surprise was sufficient to lift it back above its 50-day moving average, but short of its previous highs. Earnings estimates are rising but still remain negative.

OSI Systems (OSIS) is on hold. Fueled by solid revenue and earnings growth, OSIS broke out to new all-time highs earlier this week. Other positive takeaways from its May 1 earnings report include improving margins and a bump in full-year guidance. However, shares appear to have also stalled out this week, failing to follow through with more new highs.

Skyward Specialty Insurance (SKWD) is on hold. Shares of SKWD have also broken out to new all-time highs this week. Most recent earnings were solid with double-digit revenue and earnings growth and estimates are on the rise. However, the recent rise and breakout has caught the attention of analysts that have boosted their price targets. Expectations may be too high at this point.

AT&T (T) is on hold. This is the oldest holding in the portfolio. It was originally added for its dividend which is still respectable at just over 4%. T is also outperforming the S&P 500 year-to-date by a substantial margin. Should tariff, inflation, geopolitics, and/or economic data cause another bout of market weakness, T will likely weather any future storm like it has managed in 2025 so far.

EMCOR Group (EME) is on hold. Earnings were acceptable and likely aided in its recent share price rise, but EME has not yet returned to its recent highs. EME was swept up in AI-driven mania and it may not see new highs until the AI sector does.

ICICI Bank (IBN) can be considered on dips below its buy limit of $30.00. If you are looking for exposure to India’s financial sector, IBN is a position to consider. It is currently trading near all-time highs, and its reported earnings were better than expected, but its 12.4% gain since last October is not all that impressive when compared to OSIS.

Disclosure note: Officers of Hirsch Holdings Inc held positions in HWAIF, IWM, and QQQ in personal accounts.

|

Bitcoin & Best/Worst Sectors of “Worst Months”

|

|

By:

Christopher Mistal

|

May 08, 2025

|

|

|

|

Following a rocky April, the market has continued to rebound nicely in the first six trading days of May. As of today’s close, NASDAQ is up 2.76% and Russell 2000 is up 3.17%. DJIA and S&P 500 are moderately lagging, up 1.72% and 1.70% respectively. Whether or not this rally continues will likely depend on how quickly new tariff deals can be made. Today’s announcement of a deal with the United Kingdom is encouraging but at the same time not all that exciting. After all, we reportedly have a goods trade surplus with the United Kingdom. Progress with China and/or Europe is what is really needed for uncertainty to meaningfully dissipate.

![[S&P 500 Election Year Seasonal Chart]](/UploadedImage/AIN_0625_20250508_SP500_Seasonal.jpg)

We have updated the above chart of S&P 500 post-election-year seasonal patterns through today’s close. The bounce and rally that we had anticipated just after mid-April has continued but the pace of gains has begun to slow. Bullishly, volatility measured by CBOE’s VIX index has retreated and DJIA, S&P 500 and NASDAQ have all reclaimed their respective 50-day moving averages. The next hurdle will likely be their respective 200-day moving averages currently around DJIA 42230, S&P 500 5750, and NASDAQ 18300. Should the market track the more bullish post-election-year May seasonal patterns, the major indexes could be pushing through their respective 200-day moving averages sometime after mid-month.

Best & Worst for “Worst Six Months” May to October

In the following table, the performance of the S&P 500 and NASDAQ during the “Worst Six Months” May to October is compared to fourteen select sector indices or sub-indices, gold, Bitcoin, and the 30-year Treasury bond. Nine of the fourteen indices chosen are S&P Sector indices. Gold and 30-year bond are continuously-linked, non-adjusted front-month futures contracts. Except for two indices (Natural Gas & Biotech) and Bitcoin, 1990-2024, a full 35 years of data was selected. This selection represents a reasonably balanced number of bull and bear years for each and a long enough timeframe to be statistically significant while still representing current trends. To make an apples-to-apples comparison, dividends are not included in this study.

![[Various Sector Indices & 30-Year Treasury Bond versus S&P 500 during Worst Six Months May-October Since 1990 table]](/UploadedImage/AIN_0625_20250508_worst-six_best-worst_table.jpg)

Using the S&P 500 as the baseline by which all others were compared, five indices and Bitcoin outperformed during the “Worst Six Months” while ten others, gold and the 30-year Treasury bond underperformed based upon “AVG %” return. Bitcoin’s nearly 53% average return during the May-October period is an eye-popping figure but it is based upon just 14 years of data and its price was under $5 in May 2011 compared to over $100,000 today. If we start with data in 2018, the first full year after Bitcoin futures began trading, its average May to October gain is 12.98% with five positive periods and two negative. Interestingly, three out of four negative periods were also midterm election years (2014, 2018 & 2022, shaded).

![[Bitcoin mini table]](/UploadedImage/AIN_0625_20250508_worst-six_bitcoin.jpg)

Next on the list are Biotech and Information Technology with average gains of 7.15% and 5.51% during the “Worst Months.” Before jumping into Biotech positions, consider that only 30 years of data was available and, in those years, Biotech was up just 56.7% of the time from May through October. Some years, like 2014, gains were massive while in down years losses were frequently nearly as large.

In third place, Information Technology with 35 years of data and a 71.4% success rate is possibly a less risky choice than Biotech. Its 5.51% AVG % performance comes by way of three fewer losses in five additional years of data. However, five of the nine losses were double digit. The worst loss was 30.88% in 2008. Other double-digit losses were in 1990 and 2000-2002. After declining in 2012, Information Technology has been positive in 11 of the last 12 “Worst Six Months” periods. Holding existing tech-related positions with a trailing stop loss is one option to consider.

![[Information Technology mini-table]](/UploadedImage/AIN_0625_20250508_worst-six_infotech.jpg)

Other “Worst Six” top performers consisted mostly of the usual suspects when defensive sectors are considered. Healthcare and Consumer Staples have bested the S&P 500. Not surprisingly NASDAQ has also performed well, advancing 74.3% of the time with an average gain of 4.96%. NASDAQ’s Best Eight Months include May and June, so it does have an advantage. Although not the best sector by AVG %, Consumer Staples advancing 77.1% of the time is the closest thing to a sure bet for a gain during the “Worst Months.” However, should interest rates rise, Consumer Staples is susceptible to declines. Utilities also merit attention with a second best % Up at 74.3%, matching NASDAQ.

![[Healthcare mini-table] [Consumer Staples mini-table]](/UploadedImage/AIN_0625_20250508_worst-six_staples-healthcare.jpg)

At the other end of the performance spectrum, we have the sectors to consider shorting or to avoid altogether. The S&P 500 Materials sector was the worst over the past 35 years, shedding an average 1.35% during the “Worst Six.” PHLX Gold/Silver was third worst by average percent. However, based solely upon the percentage of time up, the stocks only, PHLX Gold/Silver index is the most consistent loser of the “Worst Six” advancing just 40.0% of the time. Aside from solid gains in 2012, 2019, 2020, and 2024, PHLX Gold/Silver has declined in nine of the last twelve “Worst Six Months.” NYSE ARCA Natural Gas is the last sector to record a loss, off 0.58%.

![[PHLX Gold/Silver mini-table]](/UploadedImage/AIN_0625_20250508_worst-six_xau.jpg)

Also interesting to note is every sector, gold, 30-year bonds, and Bitcoin are all positive in May, on average. It’s not until June when things begin to fall apart for many sectors of the market and the market itself. July tends to see a broad bounce, but it tends to be short-lived as August and September tend to be downright ugly on average. It is this window of poor performance that has tended to give October a lift in the past 35 years. Only Biotech, 30-year bonds and gold (futures and gold & silver stocks) manage to post gains in both August and September.

Based upon “% Up” Consumer Staples is the top sector of the “Worst Six Months” while Gold/Silver mining stocks are the worst. Historically speaking, May looks like a great time to consider rebalancing a portfolio as you will likely be closing out long positions into strength. Short trade ideas are also worth considering given June’s nearly across-the-board poor performance.

Sector Rotation ETF Portfolio New Trade

Despite the relatively limited number of years of data for Bitcoin, we are going to look to add a new position in

iShares Bitcoin (IBIT) on dips to the

Sector Rotation ETF Portfolio.

IBIT can be considered on dips below $55.25.

SPDR Consumer Staples (XLP) and

SPDR Utilities (XLU) can also still be considered on dips.

|

ETF Portfolios Update: New “Shorts” for May

|

|

By:

Christopher Mistal

|

May 01, 2025

|

|

|

|

For those who were unable to attend the member’s only webinar on Wednesday, the slides and video recording with an auto-generated transcript are available

here (or copy and paste in a new browser window:

https://www.stocktradersalmanac.com/LandingPages/webinar-archive.aspx). The near-term bounce we were looking for in mid-April did materialize, but the initial impact of tariff uncertainty is likely beginning to show up in economic data. Q1 GDP was negative, ADP private payrolls missed expectations, and today weekly jobless claims were also above expectations. Seasonally, historically bullish April was negative for DJIA and S&P 500, the Best Six Months were down, and 2025 continues to track the weaker Republican post-election year pattern noted on page 28 of the

2025 Almanac.

The “Worst Six Months” for DJIA and S&P 500 have arrived and the odds for our 2025 Forecast Worst Case Scenario have increased to 60% now. The clock on the 90-day tariff pause is ticking and there still have been no significant deal announcements. The market is likely to continue to endure continued volatility and chop until later in the year. Caution and vigilance still seem to be the best course of action.

May’s Sector Seasonalities

Six sectors’ favorable periods come to an end in May. Portfolio positions associated with Banking/Financials, Healthcare, Industrials, Materials (long trade from last October), Real Estate, and Transports were all closed out of the Sector Rotation Portfolio when the

Seasonal MACD Sell signal for DJIA and S&P 500 triggered in early April. If you are still holding any positions associated with these sector seasonalities, consider taking profits and/or raising any stop loss in use this month.

From page 94 of the 2025 Almanac, three sectors begin weak/bearish seasonal periods in May: Banking, Gold & Silver (stocks, not the physical metals), and Materials. We are going to look to establish corresponding short ETF positions this month. There are inverse and inverse leveraged ETFs that could be traded, but they tend to have high fees, thin average daily volume, and tracking errors over longer periods of time. Instead, we will look to simply short a typical sector-based ETF. For tracking purposes, these short trades will appear in the portfolio table below with an (S) after their names to designate a short trade. As a reminder, these short trades may not be suitable for everyone. Please do additional due diligence and consider your own personal goals and risk tolerance prior to trading.

Beginning with the first new May sector listed on page 94 of the Almanac, our top ETF to take advantage of banking sector weakness beginning in May is SPDR S&P Regional Banking (KRE). It has rebounded off its early April lows but appears to be nearing/running into resistance now right around its rapidly falling 50-day moving average. KRE could be shorted around resistance at $55.70 or on a breakdown below $53.01. If shorted, set an initial stop loss at $57.28. Cover the short position at an auto sell price of $47.96.

![[SPDR S&P Regional Banking (KRE) Daily Bar Chart]](/UploadedImage/AIN_0625_20250501_KRE.jpg)

Next up is VanEck Junior Gold Miners (GDXJ). This is likely the most controversial of today’s short trade ideas. Gold has been soaring, new all-time highs, etc. The long gold trade is likely very crowded and new all-time highs were hit last week. Gold has declined over $250 per ounce since trading over $3500 and inflation is in retreat which is likely to push mining stocks lower as well. GDXJ can be shorted near $60.05 or on a breakdown below $56.25. If shorted set an initial stop loss at $65.50. Look to cover the short GDXJ position at an auto sell price of $50.26.

![[VanEck Junior Gold Miners (GDXJ) Daily Bar Chart]](/UploadedImage/AIN_0625_20250501_GDXJ.jpg)

The final short idea is SPDR Materials (XLB). The materials sector has declined an average of 5.8% over the last 25 years from around mid-May to mid-October. If economic activity does continue to slow, demand for products supplied by the materials sector is also likely to decline, taking XLB lower along the way. XLB can be shorted around $84.10 or on a breakdown below $81.76. The initial stop loss is $87.00. Cover the short position at $72.88 or lower.

Sector Rotation ETF Portfolio Updates

“Worst Months” defensive positions in SPDR Consumer Staples (XLP) and SPDR Utilities (XLU) can still be considered below their respective buy limits. Despite the solid rally off the early April lows, a great deal of uncertainty about tariffs still overhangs the market and economic data is beginning to show signs of weakening. XLP and XLU have historically performed during periods of uncertainty and from May to November.

Two of the three new trades in foreign currencies presented on April 17 have been added to the portfolio. CurrencyShares Swiss Franc (FXF) and CurrencyShares Japanese Yen (FXY) were added on April 23, when they both traded below their respective buy limits for the first time. FXF and FXY can still be considered on dips. CurrencyShares Euro (FXE) has not been added to the portfolio and can also be considered on dips below its buy limit. Since presenting these currency ETFs, the U.S. dollar has strengthened modestly but remains well off its recent highs. If economic data continues to weaken and confidence in the market remains shaky, the U.S. dollar could easily resume its slide lower.

Invesco DB Agriculture (DBA) could also benefit from a falling U.S. dollar. DBA can still be considered on dips below its buy limit.

Tactical Seasonal Switching Strategy ETF Portfolio Updates

Per our April 17 email Issue, Invesco QQQ (QQQ) and iShares Russell 2000 (IWM) have been added back into the portfolio. Both were added during typical day after Easter weakness on April 21. As of April 30, QQQ and IWM were up an average of 8.2%.

NASDAQ’s Seasonal MACD Sell signal has not triggered. QQQ and IWM are on Hold. From now until sometime on or after June 2, 2025, the earliest date that NASDAQ’s Seasonal MACD can trigger, we will be maintaining a cautious stance in the portfolio. SHV and SGOV are currently our preferred bond ETFs. SHV and SGOV both pay their dividend monthly, and their current yields are still over 4%. Other funds of similar style are also fine alternatives if your choices are limited and SHV and/or SGOV are not available. Money market funds are also great alternatives.

TLT, AGG, and BND have exposure to long-dated Treasury bonds that have historically exhibited more price volatility than short-dated funds such as SHV and SGOV. Should weakening economic data spur the Fed into cutting rates sooner, rather than later, TLT, AGG, and BND could enjoy respectable price appreciation, but if the Fed is forced to delay reducing rates, and/or if inflation and growth accelerate, these ETFs could easily suffer losses as interest rates rise.

Positions in TLT, AGG, and BND are on Hold. If the outlook for interest rates warrants it, we may add to these existing positions when NASDAQ’s Seasonal MACD Sell triggers.

Disclosure note: Officers of Hirsch Holdings Inc held positions in FXF, FXY, IWM, QQQ, SGOV, and XLP in personal accounts.